Bridge Capital for Earnest Money Deposits: The Complete CRE Guide

As every experienced investor knows, many commercial real estate (CRE) deals are lost on timing rather than price.

An investor who can secure long-term financing to pay for a property may still lose out if they cannot provide the earnest money deposit (EMD) at the right time.

For some CRE investors, the inability to provide an earnest money deposit can be due to being presently cash-strapped. Perhaps they already have cash locked up in other projects.

Other investors may have the cash but prefer to use it to pursue other investment opportunities instead of tying it down with an escrow.

In both cases, bridge capital for earnest money can come to the rescue. With it, you can raise the cash you need for EMD and avoid losing out on good deals.

In what follows, we will consider how you can use bridge capital for earnest money as you build your CRE portfolio. We’ll cover:

- What is bridge capital for earnest money?

- How does bridge capital for earnest money work?

- What are the different types of bridge capital for earnest money deposits?

- Who are the top providers of specialized earnest money financing?

- How do I choose an earnest money financing provider?

Do you want to know how Duckfund can help you win in competitive markets? Contact us to learn more about our earnest money financing product.

1. What is bridge capital for earnest money?

Bridge capital for earnest money is a short-term financing solution that provides investors with the cash they need to make earnest money deposits before their own liquidity is ready.

In other words, bridge capital for earnest money is a form of gap funding. With it, CRE investors can register their interest in a property even if they are currently cash-strapped or unwilling to commit the cash they have.

But why is this gap funding important?

With the popularity of earnest money in commercial real estate, providing an EMD has become an important first step in securing properties.

Sellers demand it as an indication of the potential buyer's seriousness. Without it, the potential buyer cannot inspect the property or even negotiate its price.

With it, the potential buyer can:

- Kickstart the due diligence period, where they can satisfy themselves that the property is up to par

- Lock in the contract such that the seller does not show the property to other buyers

- Buy time to raise equity or secure other forms of long-term financing for the purchase price

For these reasons, serious buyers must do all they can to secure EMD financing for properties they love.

This is where bridge capital for earnest money comes in. With it, you can get your foot in the door and signify a serious interest in the property even if you are currently cash-strapped.

2. How does bridge capital for earnest money work?

Bridge capital for earnest money works in tandem with the structure of the earnest money deposit and often involves the following steps:

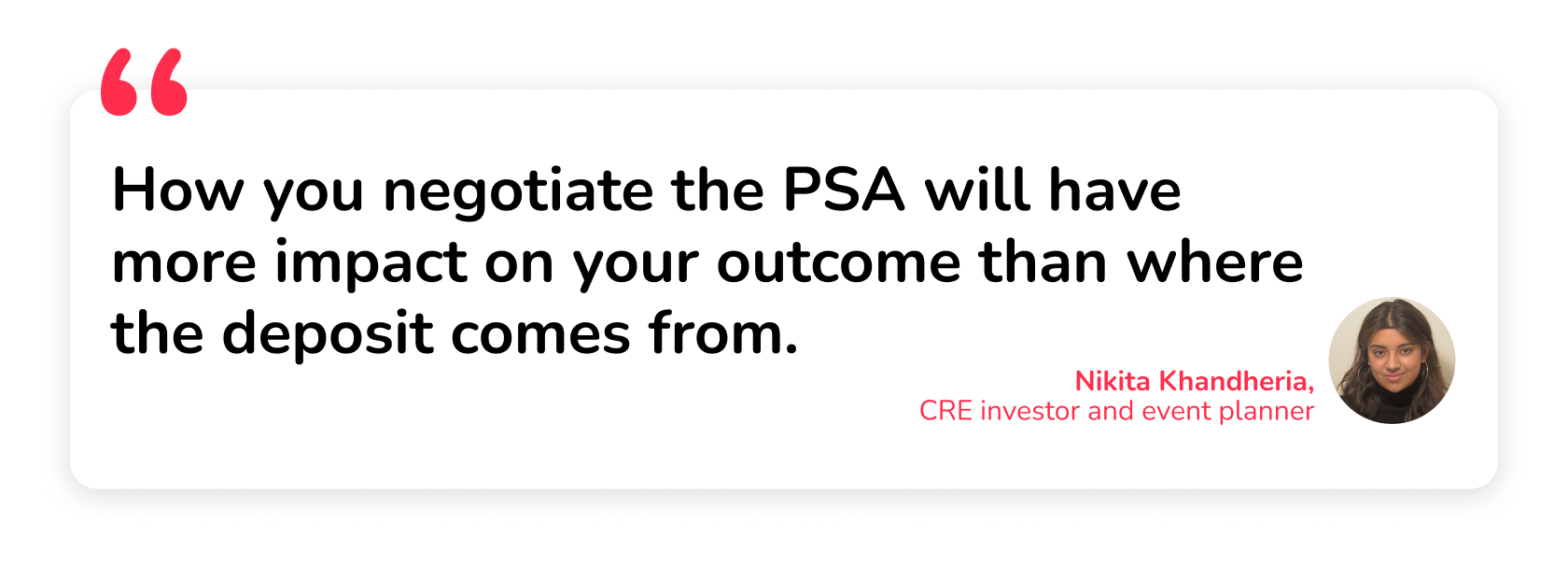

- The investor signs a Purchase and Sale Agreement (PSA) with the seller: The PSA will include all the important terms of the deal, including the purchase price, EMD amount, due dilligence period, contingencies, target closing date, warranties, representations, covenants, closing costs, among others.

This is usually the most important part since the structure of the deal can be more important than even the funding source.

“The more important point is that earnest money should be structured, not just funded,” according to Nikita Khandheria, a CRE investor and event planner. “Strong investors focus on extending diligence periods, staging deposits, and maintaining optionality for as long as possible. How you negotiate the PSA will have more impact on your outcome than where the deposit comes from.”

- The bridge capital provider wires the EMD to an escrow agent: Once you have signed the PSA, you will submit it as part of your application for EMD financing. If your application is successful, the bridge capital provider will wire the EMD to an escrow. The escrow will keep the funds and handle them according to the terms of the PSA.

- The investor completes due diligence: The payment of EMD unlocks the due dilligence period. Within this period, you can conduct a thorough due diligence on the property. This includes verifying the title, inspecting the property’s physical components, and performing a market analysis, among others.

- The investor decides whether to go on with the contract or not: The results of the due dilligence will largely determine if you are willing to close the deal or not. Another important factor is whether you are able to secure the financing to pay for the property.

- The investor refunds the EMD to the bridge capital provider if the deal succeeds: If everything goes well, you will close the deal with the seller and repay the EMD to the financing company.

- The escrow refunds the EMD to the bridge capital provider if the deal does not succeed: If the deal does not succeed because the seller pulls out, the escrow will refund the EMD to the original funding source, in this case, the bridge capital provider.

Also, the EMD will be refundable if you pull out due to a reason associated with any of the agreed contingencies.

Issues are likely to arise if you pull out of the deal for a reason not associated with the contingencies. In that case, you may lose the EMD to the seller and then have to repay the EMD lending provider.

You can also see all of these steps in the chart below:

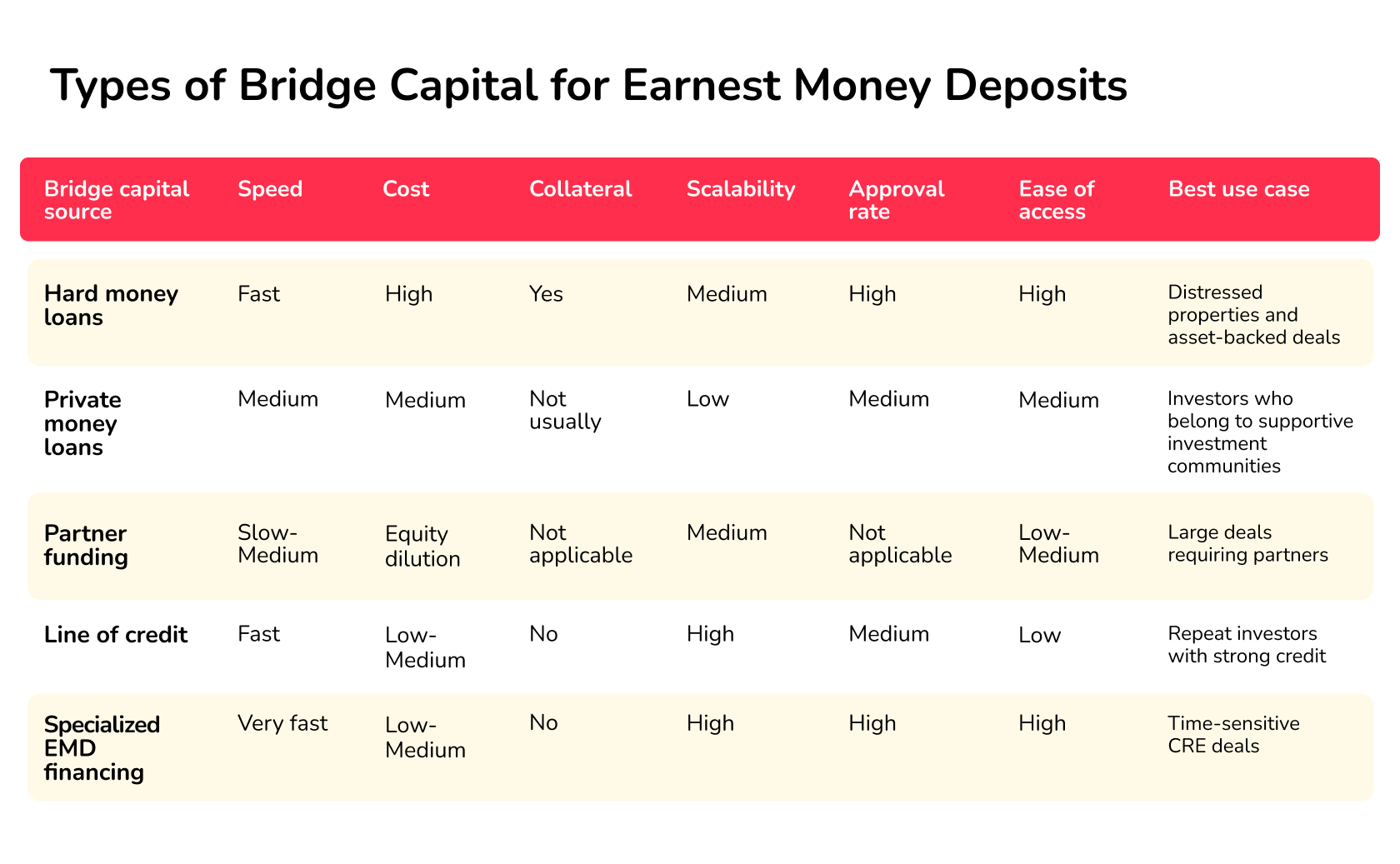

3. What are the different types of bridge capital for earnest money deposits?

The different types of bridge capital for EMD include hard money loans, private money loans, a line of credit, partner funding, and specialized EMD financing.

Though all of these financing methods can help secure earnest money financing, they have different pros and cons that affect their suitability. We cover each in turn:

- Hard money loans

These are short-term loans that are secured by a ‘hard’ asset. In other words, hard money loans are backed by collateral rather than the borrower’s income or credit score.

Hard money loans are often used as bridge financing to pay for a property while investors wait for more permanent funding. Some investors also use them to secure EMD while waiting for a loan to fund the property’s purchase.

Pros of hard money loans

- High approval rate

- Quick access to funds

- Can fund risky or distressed properties

Cons of hard money loans

- High interest rates

- Usually requires collateral

- Private money loans

Private money loans are advanced by private lenders (usually high-net-worth individuals). They are often based on the personal relationship between the lender and the borrower. As a result, the terms are more flexible.

Pros of private money loans

- Flexible terms

- Based on personal relationship rather than collateral

Cons of private money loans

- Cannot be easily scaled for multiple deals

- May require personal guarantees

- Partner funding

A solo investor may receive the EMD from an investor who wants a share of equity in the property. Instead of repayment (with interest), the investor receives a share of the profit/loss on the property.

Also, if the General Partner (GP) or Sponsor of a joint venture cannot raise the EMD, one of the Limited Partners (LPs) can offer to pay it for a chance to get priority returns or a co-General Partner (co-GP) position.

Partner funding is common in larger deals that require more significant EMD.

Pros of partner funding

- No repayment needed

- Ideal for large deposits

Cons of partner funding

- Dilutes ownership

- Slower to structure

- Negotiations can be complex

- Line of credit

Experienced and credit-worthy CRE investors, especially sponsors or GPs, often have a business line of credit with financial institutions that they can explore when cash is tight.

A line of credit allows them to borrow funds as needed up to a given limit.

Pros of a line of credit

- Reusable capital

- Fast access due to preapproval

Cons of a line of credit

- Requires a strong credit score and a prior relationship with the financial institution

- May include restrictions and covenants

- Specialized EMD financing

All the methods we have explored so far are generic financing solutions that investors use for a variety of purposes.

In contrast to them are fintech platforms that are specially dedicated to financing EMDs across different CRE types.

Pros of specialized EMD financing

- Quick approval

- Fast funding (24-48 hours)

- No collateral required

- No credit score required

- Streamlined process

Cons of specialized EMD financing

- Will require a PSA

- Limited to verified deals

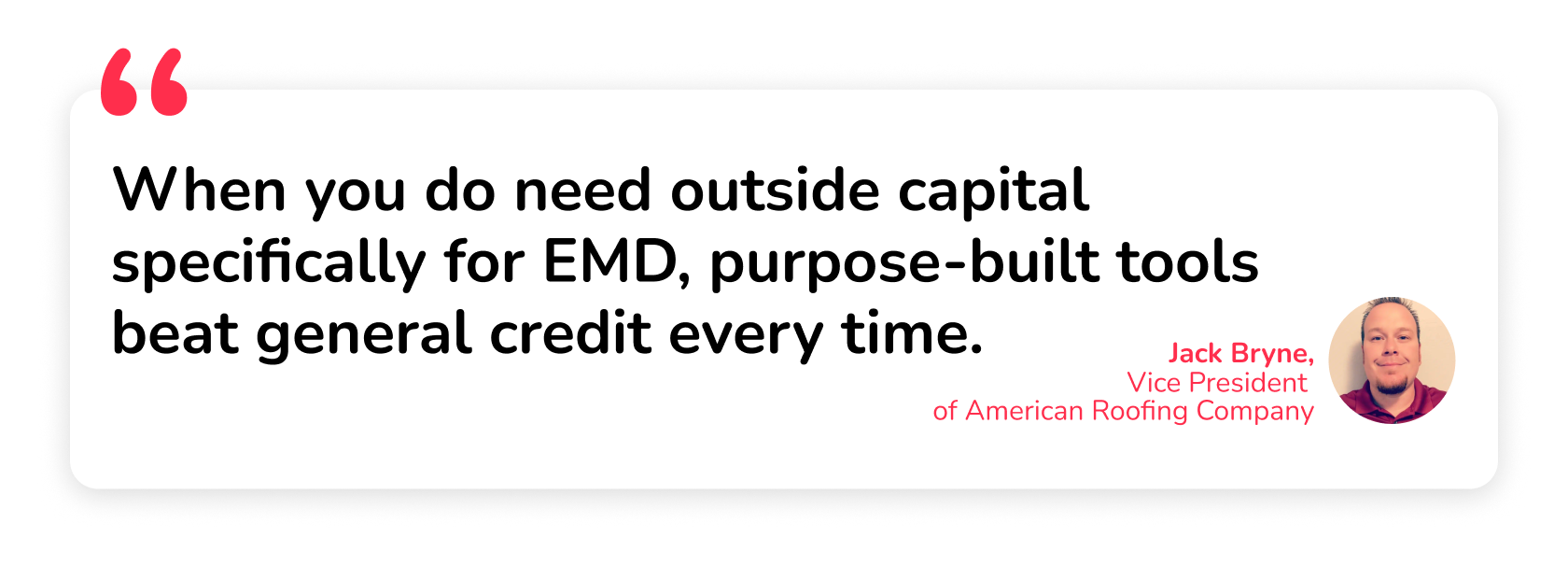

Many investors with experience in the CRE space prefer specialized EMD financing to generic financing for its speed, flexibility, and high approval rate.

“When you do need outside capital specifically for EMD, purpose-built tools beat general credit every time,” according to Jack Bryne, the Vice President of American Roofing Company, a construction roofing company. “The underwriting speed, the terms, and the approval criteria are just built differently when the product is designed for one specific problem. That purpose-specificity matters since a generalist lender will slow you down at exactly the wrong moment.”

The alignment between the terms of the funding and the deposit window is another key advantage.

“What makes a purpose-built EMD product stand out is that the timeline and terms are built around the actual deposit window, not retrofitted from a generic loan product,” according to Nancy Avila, a community manager at ViewPointe Executive Suites, a real estate company. “That alignment matters when you're racing a contract deadline.”

Also, you can build a long-term relationship such that you can pursue all the deals you want without having to worry again about where to get a commercial property loan deposit.

Having a dedicated provider can provide an advantage in competitive markets.

The chart below compares these five bridge capital sources based on key factors important to investors:

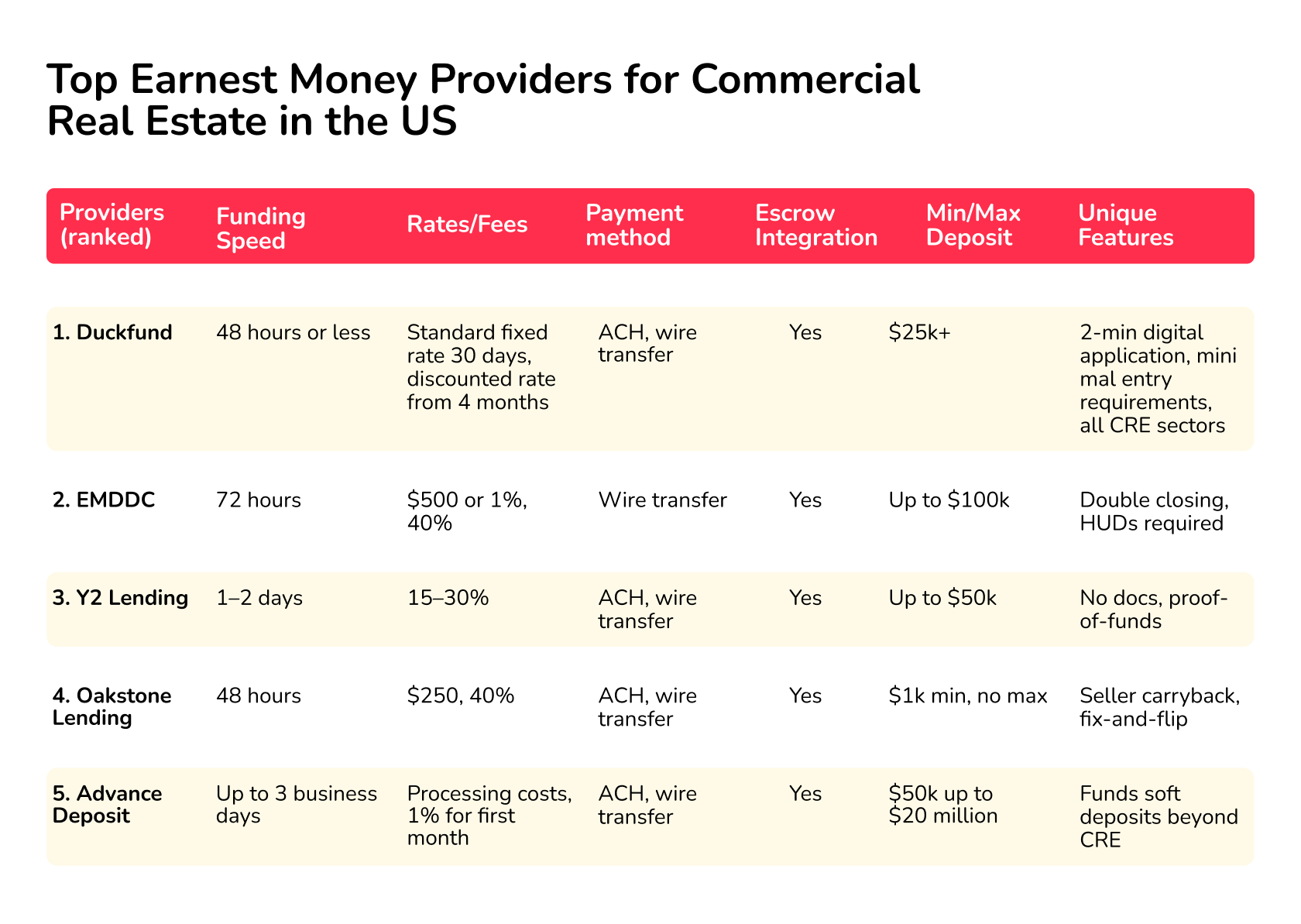

4. Who are the top providers of specialized earnest money financing?

Duckfund, EMDDC, Y2 Lending, Oakstone Lending, and AdvanceDeposit are some of the best earnest money deposit providers for CRE financing in the US.

Below is a comparison table showing how their product offerings differ:

5. How do I choose an earnest money financing provider?

The most important factors when it comes to choosing a specialized earnest money financing provider are funding speed, accessibility, fee structure, funding reliability, flexibility, deal size, and long-term relationship.

Let’s consider how these five providers compare across these factors:

- Funding speed: With Duckfund, Y2 Lending, and Oakstone Lending, you can be assured that the funds will get to the escrow in not more than 48 hours (2 days) from application approval.

- Accessibility: EMDCC requires three HUD-1 settlement statements as evidence of prior experience. The other providers only require a signed PSA.

- Fee structure: EMDCC and Oakstone Lending charge an upfront fee, and they also expect a certain rate of return depending on the term. AdvanceDeposit also charges a processing fee in addition to the financing fee.

Though Y2 Lending does not require an upfront fee, the financing fee is on the high side.

In contrast, Duckfund charges a single fixed financing fee and even offers a discounted rate from the fourth month of the due diligence period.

- Funding reliability: All providers will send the necessary funds to the escrow after a successful application.

- Flexibility: One of Duckfund’s unique selling propositions (USP) is that they allow you to propose higher EMD amounts in competitive markets. If the seller is asking for 5%, you can propose 10% to show seriousness, and Duckfund will provide the funds.

- Deal size: EMDCC and Y2 Lending have maximum thresholds. This may make them inappropriate for larger CRE deals. On the other hand, Duckfund, AdvanceDeposit, and Oakstone Lending do not have any upper limit, which makes them appropriate for larger deals.

- Long-term relationship: Duckfund and Y2 Lending place a premium on becoming a dedicated source of EMD financing for their users.

However, Duckfund takes this a step further by allowing you to work on multiple simultaneous deals. You don’t need to conclude one deal before you get EMD for another.

Having a dedicated source of bridge capital for earnest money is essential in a CRE market where EMDs are becoming even more important.

Investors who operate in competitive markets especially need a specialized earnest money financing company that can offer speed, flexibility, reliability, and cost-effectiveness.

With Duckfund, you can gain a competitive advantage irrespective of the market where you operate.

Our goal is to be your success partner, offering you just what you need to stand out, whether that is higher EMD amounts, EMDs for multiple simultaneous deals, or longer term for an extended due diligence period.

Are you ready to build a CRE portfolio without worrying about earnest money deposits? Sign up for Duckfund for quick and seamless earnest money financing across multiple deals.

Takeaways

- Timing wins deals in CRE. Investors often lose deals not on price, but on their ability to fund EMD quickly.

- Bridge capital solves liquidity gaps by enabling investors to secure deals without tying up cash or missing opportunities.

- Specialized EMD financing outperforms generic funding with faster approvals, better alignment with deal timelines, and higher success rates.

- Selecting the right provider is a competitive advantage. Speed, flexibility, and reliability can directly impact your ability to win deals.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence