How Commercial Property Development Finance Is Evolving: 5 Trends for 2026

Success in CRE as a developer depends on many market factors, and quick access to commercial property development finance is atop that list.

With lenders loosening standards and CRE developers hoping to capitalize on market recovery, it’s the informed borrower who has the best shot at obtaining a construction loan. Yet most developers:

- Don’t know which types of business loans are available to them

- Don’t choose the right property development loan for their needs

- Can’t find short-term loans at reasonable terms to cover down payments and earnest money deposits

That's starting to change. New commercial real estate loan originations surged 90% year-over-year through early 2025, according to CBRE's Lending Momentum Index, as interest rates dropped and financial institutions opened up to CRE markets.

Developers pursuing new commercial property acquisitions or development projects are finding improved terms, relaxed underwriting, and abundant development finance options they didn't have a year ago.

In this CRE expert guide, we examine the five most important trends shaping commercial property development finance in 2026.

From private credit's dominance to AI-powered underwriting and ESG-linked financing, understanding these shifts helps smart CRE developers secure deals and stay ahead of the competition.

[Looking to move quickly on CRE opportunities without hurting your cash flow? Sign up for flexible soft deposit financing options designed for today's market — with approval in just 48 hours.]

How does commercial property development finance work?

Commercial property development finance covers funding for every stage of a CRE project – from initial acquisition through construction to pre-closing needs.

In short, commercial development finance includes three components: acquisition capital for purchasing land or properties, development loans for construction and improvements, and earnest money deposits that secure deals before closing.

And how does property development finance work? Developers typically layer multiple financing sources depending on project phase and risk profile. A ground-up commercial property development might combine senior construction debt, mezzanine financing, and equity — while value-add projects often rely on bridge loans and seller financing.

We've covered the six main types of commercial property development finance in detail previously. But heading into 2026, it's not just the financing solution types that matter.

CRE developers also have to understand which lenders are active, what terms they're offering, and how market dynamics are reshaping access to capital in 2026. With that said, let’s look at five major trends in CRE development financing.

5 top trends in commercial property development finance

1. Private credit is a driving force in commercial real estate finance

Private lenders have gone from niche players to driving force in commercial real estate development finance. These non-bank entities – debt funds, mortgage REITs, and private equity credit arms – now account for a whopping 24% of US CRE lending volume, according to Deloitte's 2026 outlook. That’s 1.7 times their 14% average of the past 10 years.

Why do borrowers prefer private financing solutions for finance for property developers? Speed trumps cost. Private lenders close deals in weeks while banks typically take much longer. On top of that, banks might pull a conditional approval if market conditions change.

Private lenders are also more able to structure unique terms, whereas banks and big financial institutions have narrower margins to play with.

The tradeoff? Interest rates charged by private lenders typically run higher than for bank loans. But for developers seeking how to get funding for property development with proven track records, those higher interest rates buy execution certainty and industry know-how.

“Our extensive borrower relationships, built over the past decade, have enabled us to continue our disciplined deployment into an attractive market,” said Joel Traut, Partner and Head of Originations for Real Estate Credit at KKR, a global investment banking firm.

“We believe private capital will play an increasingly important role in the commercial real estate market as loan demand continues to climb, and this positions us very well to deliver attractive risk-adjusted opportunities for our investors,” Traut added.

This reflects a new financing reality, where private capital is redefining how deals get done instead of just filling short-term cash flow gaps.

2. AI-powered underwriting isn’t accelerating deal execution – yet

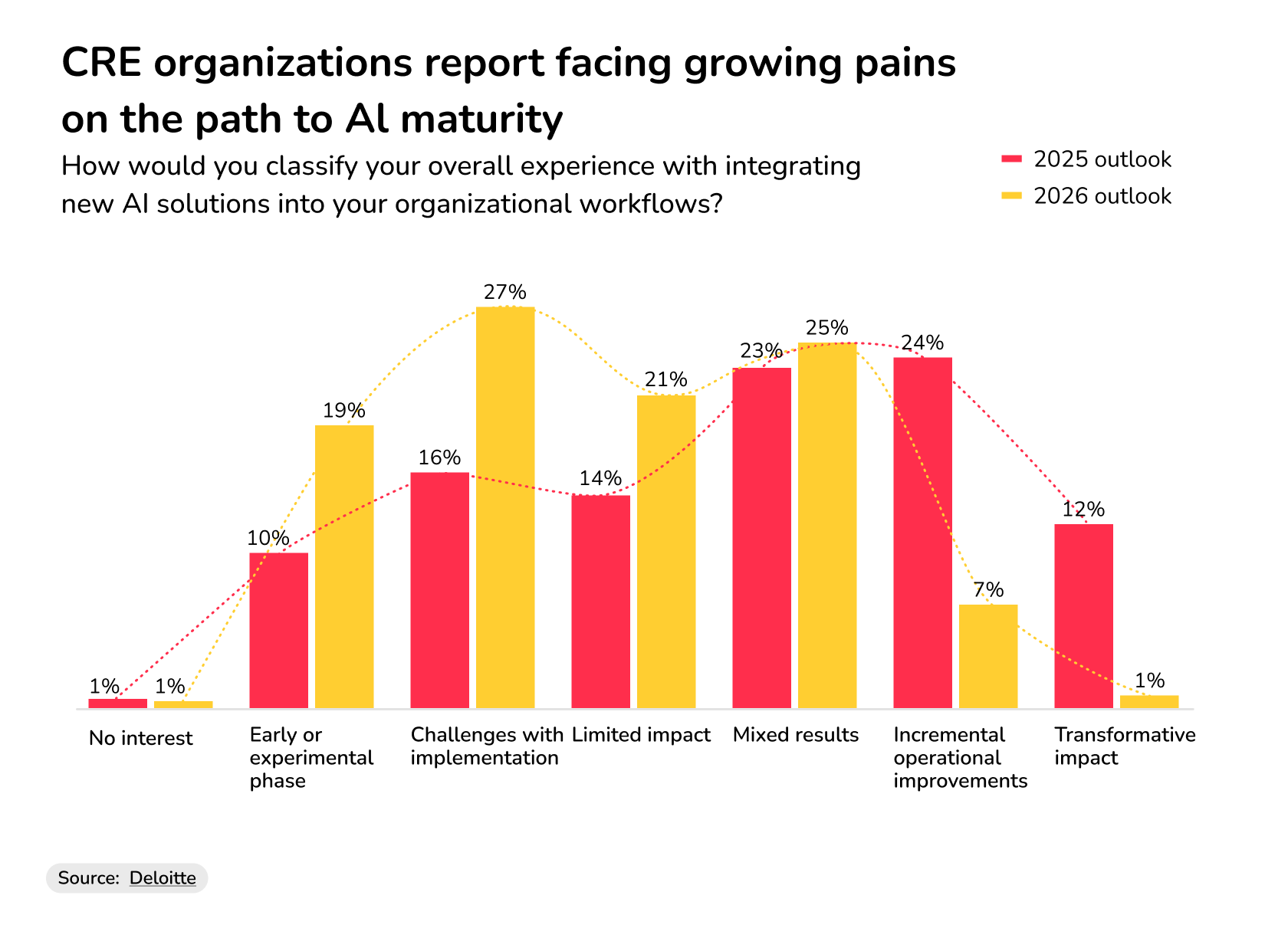

Technology is changing the CRE landscape – but how fast? Not nearly as fast as CRE leaders expected.

Only a third of companies expect to see mixed to transformational results from AI implementation, according to Deloitte’s 2026 Commercial Real Estate Outlook. That’s a noticeably different outlook from last year, when 59% of CRE organisations expected as much.

Source: Deloitte

So while last year’s hype might have led to high expectations, this year’s reality check is hitting hard.

88% of CRE investors are now piloting AI initiatives, with most pursuing an average of five use cases simultaneously. Yet, only 5% report achieving all their program goals, according to global real estate services firm JLL.

Another 47% hit two to three goals at best, and most implementations remain stuck in experimental mode with limited scaling. But lenders funding property development who've cracked AI implementation are seeing real advantages in underwriting speed and accuracy. These lenders can better determine creditworthiness and improve asset management.

For borrowers seeking commercial development finance, the takeaway isn't that AI doesn't work. Nor should they fall for empty AI promises.

CRE developers looking for smart banking solutions should work with tech-forward lenders who've successfully implemented AI into underwriting processes to shorten approval timelines and get commercial property financing closed before anyone else.

3. ESG-linked financing is becoming a lending requirement

Environmental, social, and governance metrics have shifted from nice-to-have differentiators to important underwriting criteria for commercial property financing.

The global green building market represents a $24.7 trillion opportunity by 2030, according to Rhino Energy's 2026 ESG trends report. And 90% of major real estate organizations now align new development projects with green building standards — up from barely half just two years ago.

So what does this mean for funding property development in reality? Better terms if you're ESG-compliant, worse if you're not.

Lenders are embedding sustainability into every aspect of development finance. Fannie Mae's Green Financing program, for example, offers 0.10% interest rate discounts on multifamily development loans for properties meeting energy efficiency standards — plus higher LTV ratios up to 85% versus 80% for conventional deals.

"Buildings and construction sectors combined account for approximately 33% of total global energy consumption and nearly 15% of carbon emissions," Marco Meyer notes.

Meyer, who is Head of Sustainable Banking Germany at tech consultant Capgemini Invent, further explains that "Banks need to define criteria that enable them to grant sustainable loans," as regulators increasingly require ESG risk assessments in loan amount determinations.

For developers pursuing how to finance commercial property development, the winning strategy is to integrate ESG from project conception.

Energy-efficient designs, renewable energy systems, and green certifications are the sustainable path to better financing terms and faster approvals from lenders prioritizing future-proof assets.

4. Alternative lenders are filling traditional bank gaps

As banks reduced CRE exposure in recent years, non-bank lenders have become the go-to source for borrowers seeking how to get funding for property development. This is especially true for needs that traditional institutions won't touch.

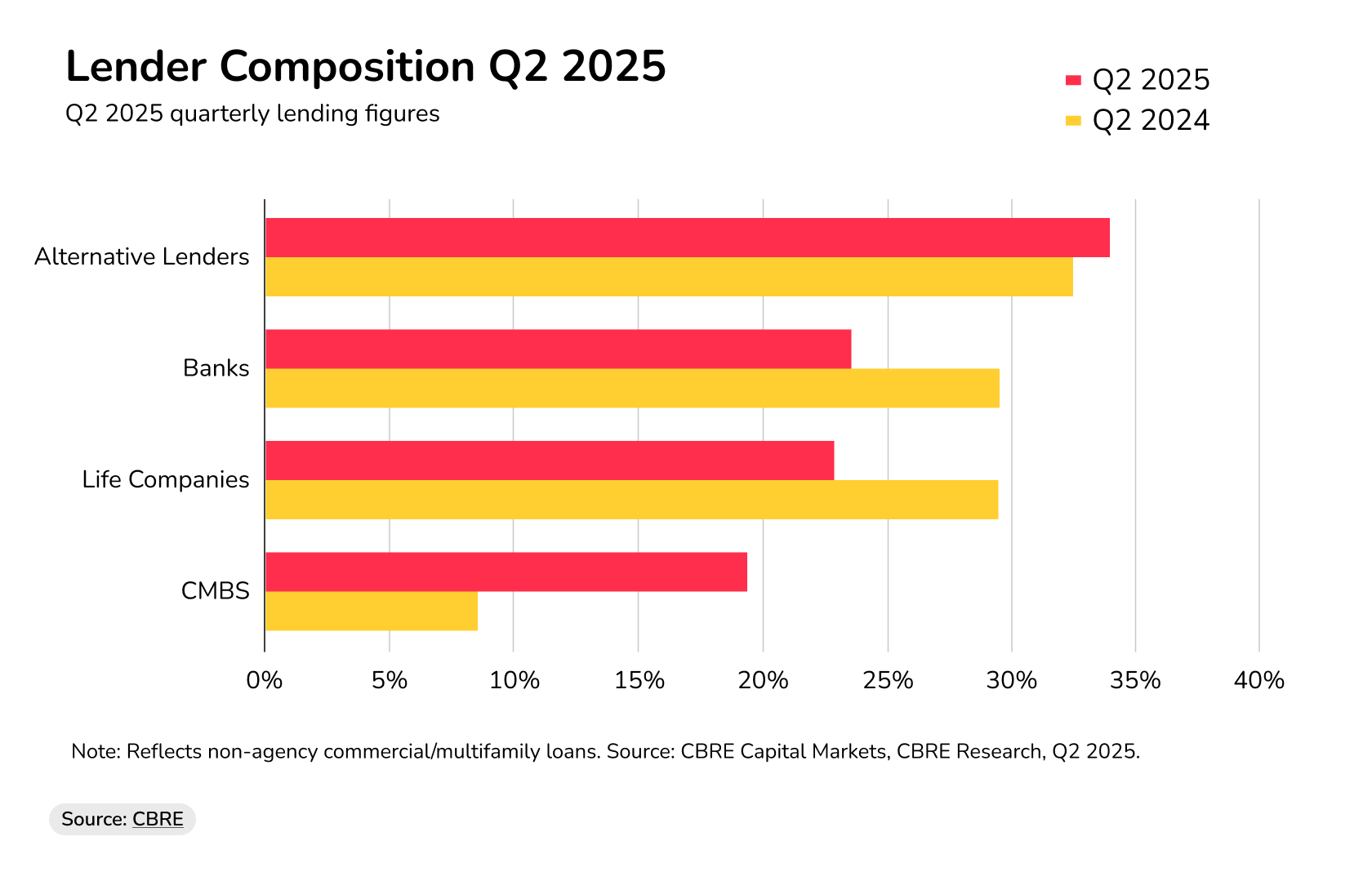

Take alternative lenders like debt funds and mortgage REITs, for instance. They captured 34% of non-agency loan closings in Q2 2025, up from 32% the prior year, according to CBRE. Debt fund volumes specifically surged 89% quarter-over-quarter and 52% year-over-year.

Source: CBRE

Meanwhile, banks dropped from 29% to 24% market share as they continued trimming commercial mortgage portfolios.

What's replacing traditional bank loans? Financing options banks overlook entirely. Bridge loans for transitional properties, mezzanine financing to fill capital stack gaps without diluting ownership — and most critically, specialized commercial bridging loans for property development needs like earnest money deposits.

"There are three things needed for success in the CRE market today: fast capital for earnest money, a good investment profile, and access to senior debt/proof of funds," said Anna Kogan, CEO and founder of Duckfund.

Take earnest money. EMD requirements strain investor capital, often demanding up to 10% of property value upfront to secure deals. With deposits ranging from $500,000 to several million on competitive properties, developers face a choice – tie up working capital for 60-90 days during due diligence, or lose deals to competitors with faster access to finance for property developers.

That's where specialized EMD lenders changed the game. Providers like Duckfund offer 48-hour earnest money funding with fully refundable deposits starting at $25,000, letting developers secure multiple properties simultaneously without depleting liquidity.

In 2026’s construction development finance landscape, CRE developers with alternative financing solutions can fasttrack land purchases while banks stay on the sidelines.

5. Construction lending stabilizes (but only for winning sectors)

Can you get a loan for property development in 2026? Yes. But your odds at getting a construction loan depend on which sector you're building in.

Construction loans aren't flowing evenly across CRE. Capital is concentrating in sectors with strong fundamentals while avoiding troubled asset classes. Current rates run from 6.8% to 13.8% depending on borrower strength and project type, according to CRE mortgage intermediary Janover.

Multifamily construction financing is leading the recovery. The Federal Housing Finance Agency just raised Fannie Mae and Freddie Mac's combined lending caps to $176 billion for 2026 — a 20% jump from 2025's $146 billion — signaling strong appetite for apartment development projects.

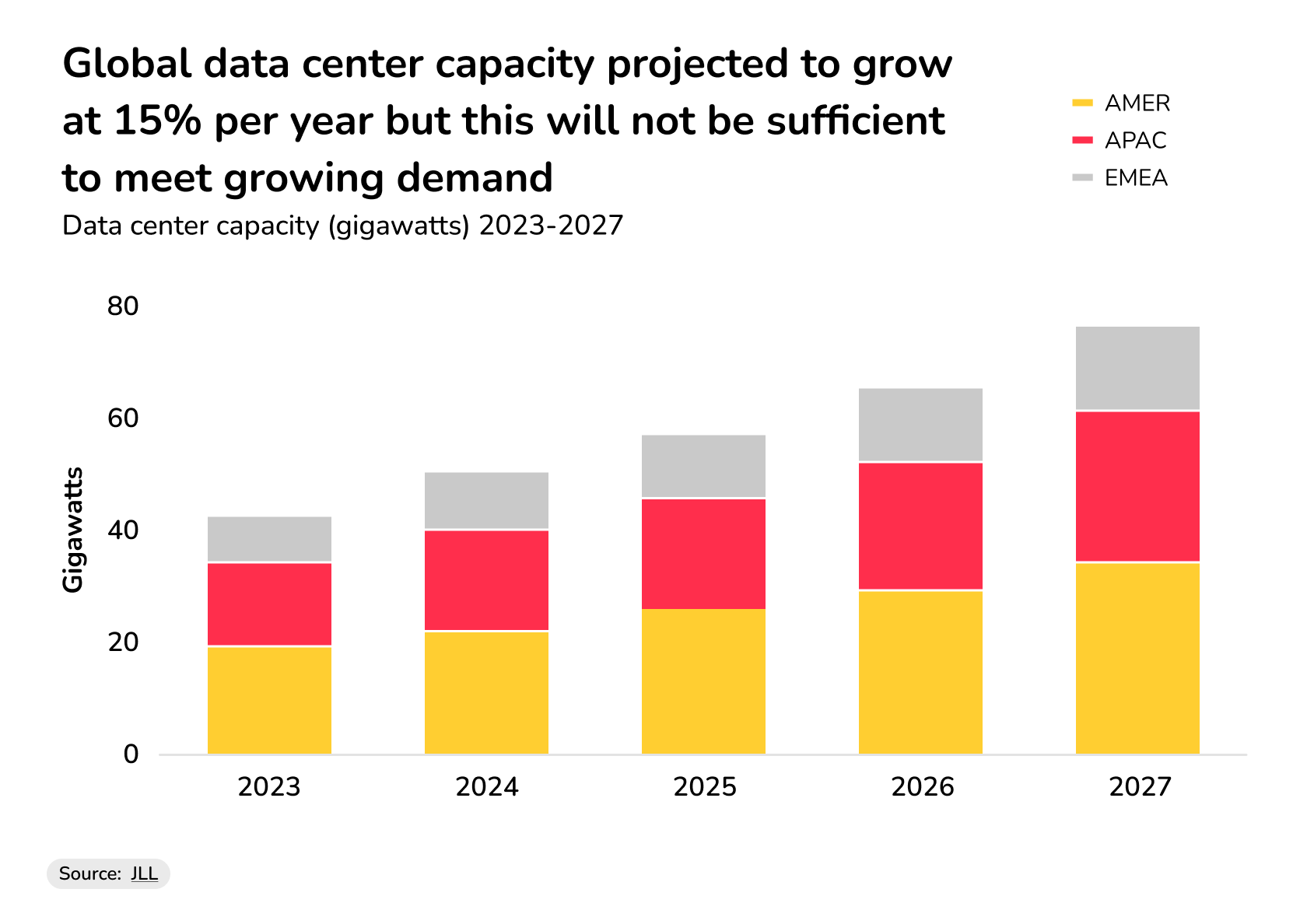

Data center construction financing is even hotter. An estimated $170 billion in asset value needed development or permanent financing in 2025, with typical construction debt at 65-80% loan-to-cost, according to JLL. Going forward, a booming AI industry is expected to keep demand growing.

Source: JLL

Finally, industrial and manufacturing properties remain strong in key growth regions, while office building construction has essentially frozen outside selective Class A suburban developments.

The message is clear: for developers pursuing how to finance a real estate development project, sector fundamentals drive financing availability. Some sectors simply see better returns than others.

What is the 2% rule in commercial real estate?

For developers assessing whether a project warrants pursuing how to finance a real estate development project, the 2% rule serves as a quick feasibility check. This rule suggests that a rental commercial property should generate monthly rent equal to at least 2% of its purchase price.

A property generating 2% monthly returns typically produces sufficient cash flow to service debt, cover operating expenses, and provide adequate returns. But don't mistake this for a strict lending requirement.

Modern CRE financing looks at multiple factors beyond simple rent-to-price ratios. Loan-to-value ratios, debt service coverage (typically 1.25x minimum), tenant quality, property type fundamentals, and market conditions – they all matter more than hitting an arbitrary 2% threshold.

Your next move in CRE development financing

Commercial property development finance in 2026 rewards strategic investments over simple creditworthiness. Private credit dominates, AI adoption lags behind hype, ESG requirements tighten, alternative lenders fill bank gaps, and construction capital flows to winning sectors — not struggling ones.

The developers closing deals aren't waiting for perfect conditions. They're building relationships with non-bank lenders, integrating sustainability early, and focusing capital on sectors where financing actually exists.

[Don't let earnest money deposits slow your land purchases. Join 4,000+ CRE investors who've secured over $1.5 billion in deals with Duckfund's Sign Now, Pay Later model. Get 48-hour approval, zero upfront capital, and discounted rates starting month four.]

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence