How to Use Commercial Real Estate Bridge Loans to Win More Deals in 2026

Commercial real estate bridge loans are being misused by investors in 2026 – and that’s exactly why the smartest operators are finding outsized opportunities.

Too many sponsors still treat commercial bridge funding like a bailout, something to lean on only when a bank backs out or a refinance collapses.

But the investors gaining real ground this year understand that commercial real estate bridge loans work best when used with intent, not desperation.

If you’re a CRE investor, you may have felt the pressure of deal timelines tightening thanks to:

- Lenders dragging their feet with approvals

- Lower than expected loan amounts

- Expensive contract extensions that eat into negotiating leverage.

In this environment, the right bridge loan becomes a strategy tool – one that shapes negotiations, provides early control of the asset, and keeps deals moving while long-term financing catches up. The key is using bridge capital with discipline.

That’s what this guide will break down: when to use commercial real estate bridge loans, how to structure them, and the pitfalls to avoid in 2026.

We’ll cover:

- What is a bridge loan in commercial real estate?

- How to use commercial real estate bridge loans: The top strategies

- What are the pitfalls of CRE bridge loans?

- What type of loan is best for commercial property?

Is a lack of CRE funding stopping you from investing? Contact Duckfund to find out how our fast, flexible financing can secure your next deal in 48 hours.

What is a bridge loan in commercial real estate?

A commercial bridge loan is an alternative CRE financing option that helps real estate investors act quickly when a property needs work or when a traditional lender can’t move fast enough.

Many investors turn to bridge financing when an asset sits in transition and won’t qualify for permanent financing until the numbers improve. Commercial real estate bridge lenders look at where the project is headed and how well you can carry out the plan.

Rates might come in higher, and loan-to-value (LTV) limits may run tighter, but the flexibility often gives investors the breathing room they need to strengthen the asset and set up better long-term options.

In 2026, knowing how to use that flexibility can decide whether you capture an opportunity or watch it slip away.

How to use commercial real estate bridge loans: The top strategies

Bridge financing works best when you build it into the deal from the start.

The right commercial real estate bridge loan can give you a path to completion when traditional financing options slow you down. Here’s where it delivers the most value in 2026.

1. Move first in competitive or distressed acquisitions

A bridge loan gives investors a way to act before a bank or agency lender finishes its paperwork.

Deals involving distressed sellers or off-market assets often demand proof of funds long before conventional underwriting wraps up.

Many investors gain control by using fast earnest money financing, like Duckfund, to post a stronger deposit and secure the contract. That early commitment buys time to finalize the full bridge loan or permanent financing while the deal stays locked in and competitors fall behind.

2. Reposition properties or complete value-add improvements

When an asset needs updates to qualify for permanent financing, a bridge loan supplies the runway.

Investors often use a commercial bridging loan for property development to support renovations that strengthen cash flow or help a property break into a new rent tier.

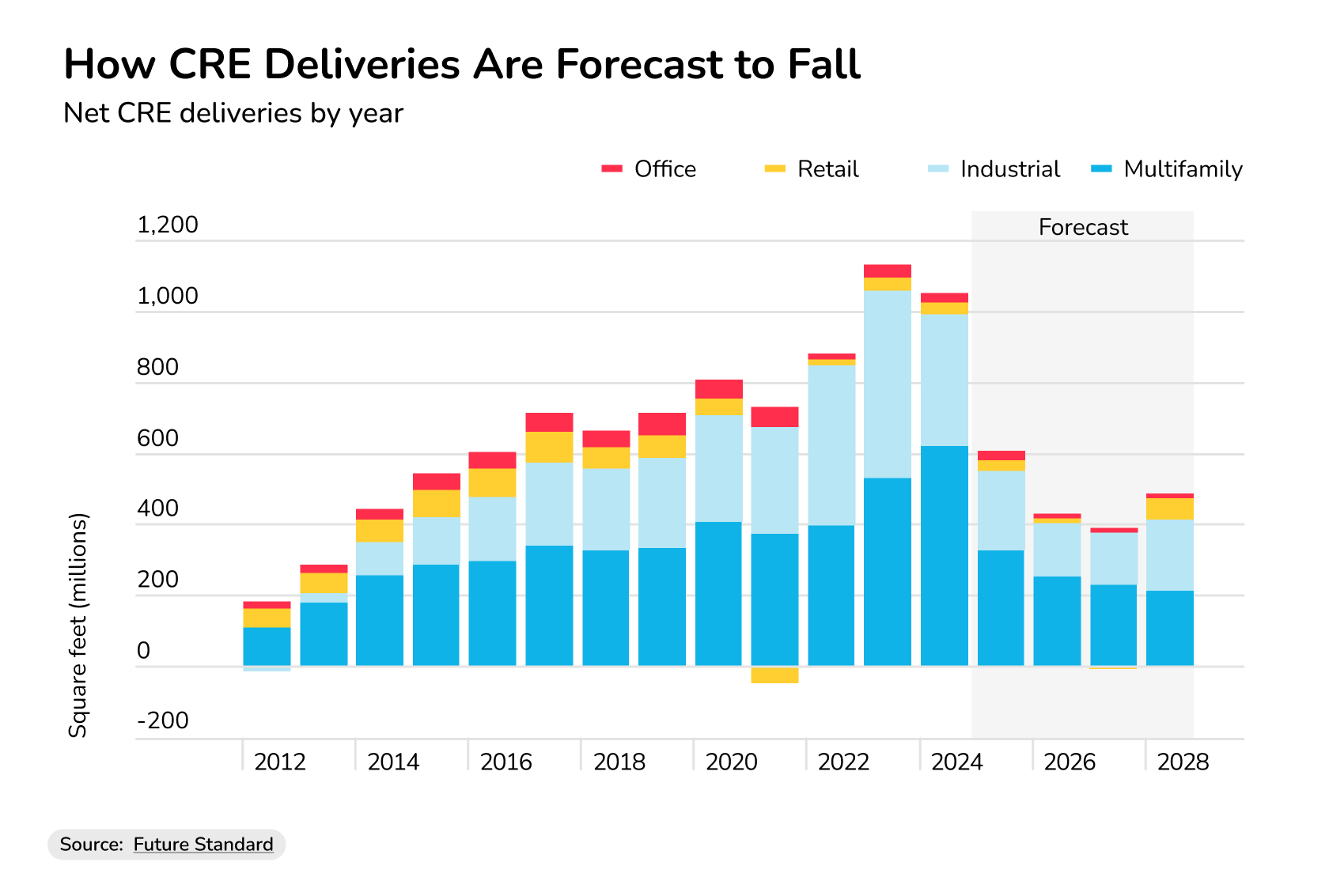

As the chart below shows, net CRE deliveries for multifamily and industrial are forecast to fall well below the recent peak, which supports healthier fundamentals for existing assets.

Source: Future Standard

This backdrop makes bridge financing especially useful for sponsors who want to reposition properties now and hold them through a period of limited new supply.

Lenders focus on the business plan, the sponsor’s track record, and whether projected income supports the capex timeline.

3. Stabilize assets with occupancy or revenue issues

Some properties fall into transition, like when income lags behind projections, or tenant improvements remain incomplete.

A bridge loan creates breathing room to reach stabilization. Borrowers typically see better LTV or LTC outcomes once lease-up advances and cash flow move in a healthier direction.

4. Cover a refinance gap when permanent financing falls through

In 2026, more investors face lower-than-expected appraisals or credit committees shifting loan terms late in the process.

A bridge lender steps in with short-term financing that keeps the asset out of distress and avoids unnecessary capital calls. This option buys time to rebuild the numbers for a stronger long-term financing package.

5. Acquire businesses with meaningful real estate value

Some business loans don’t fit SBA or bank requirements, especially when the operating company relies heavily on the underlying property.

A bridge loan for business acquisition lets investors close quickly and restructure the deal later. This approach often supports acquisitions in self-storage, RV parks, hospitality, and other asset types where the real estate drives most of the valuation.

What are the pitfalls of CRE bridge loans?

Bridge financing opens doors, but it also comes with traps that can shrink returns if borrowers don’t plan ahead. Most missteps happen when investors rush into a short-term loan without aligning it to the deal’s timeline or cash flow.

Here are the issues that show up most often in 2026.

Underestimating the real cost of interest-only payments

Bridge loans often rely on interest-only structures that look manageable on paper.

Monthly payments can pile up fast if the renovation or reposition plan drifts off schedule. Investors can protect themselves by modeling a slower stabilization, not the ideal one.

Relying on exit values that no longer match the market

Appraisals are coming in lower across many commercial real estate categories, and the pressure isn’t easing.

Deloitte notes that many older loans were underwritten during a low-rate environment, and today’s higher interest rates and stricter underwriting are forcing a broad repricing.

When investors rely on valuations anchored in a different cycle, refinance proceeds often fall short. Conservative valuation, in this case, helps avoid sudden surprises.

Sticking with a capital stack that doesn’t survive lender scrutiny

Some projects look solid until a lender digs into the business plan or the borrower’s credit score.

The FDIC (and other regulators) have stepped up scrutiny of bank CRE exposures, and the GAO found that over 40 % of banks have tightened underwriting standards for real-estate lending since the start of 2024.

That means even non-bank lenders feel the ripple effects through higher expectations and slower approval timelines.

Borrowers tend to get better results when they simplify the structure before the loan goes into review.

Taking on loan terms that restrict flexibility

Origination fees, extension costs, and prepayment penalties can erode returns if the timeline stretches.

A bridge loan often gives flexibility on day one but limits choices later in the deal. Investors avoid friction when they negotiate extension rights early and confirm repayment requirements before signing.

Using the wrong structure for the property type

A bridge product that works for multifamily development doesn’t always fit industrial, self-storage, or hospitality assets.

Each category moves through stabilization at its own pace, and cash-flow patterns vary more than most borrowers expect. Even in a cautious market, lenders still lean toward multifamily and industrial because the fundamentals hold up, so choosing a bridge structure that plays to those strengths gives sponsors a smoother path toward stabilization.

Selecting loan programs that reflect how the asset actually performs, rather than how the model looks, creates fewer surprises when you transition into long-term financing.

Assuming a bridge loan fixes operational issues

A bridge loan can buy time, but it can’t solve operational gaps inside value-add or repositioning deals.

If a project needs better leasing, stronger management, or a different renovation plan, extra debt won’t cover the shortfall. Investors who treat the loan as breathing room (not a repair tool) keep the project on track.

How to structure a successful commercial bridge loan

A strong bridge loan isn’t built on speed alone. In 2026, lenders want deals that look realistic and are resilient against market swings.

Here’s how to structure a fast commercial bridging loan that clears underwriting and supports the project’s path toward permanent financing

1. Start with a lender-ready business plan

A bridge lender decides quickly, but they still expect a clean package. That means having a financial model that makes sense and a realistic exit strategy.

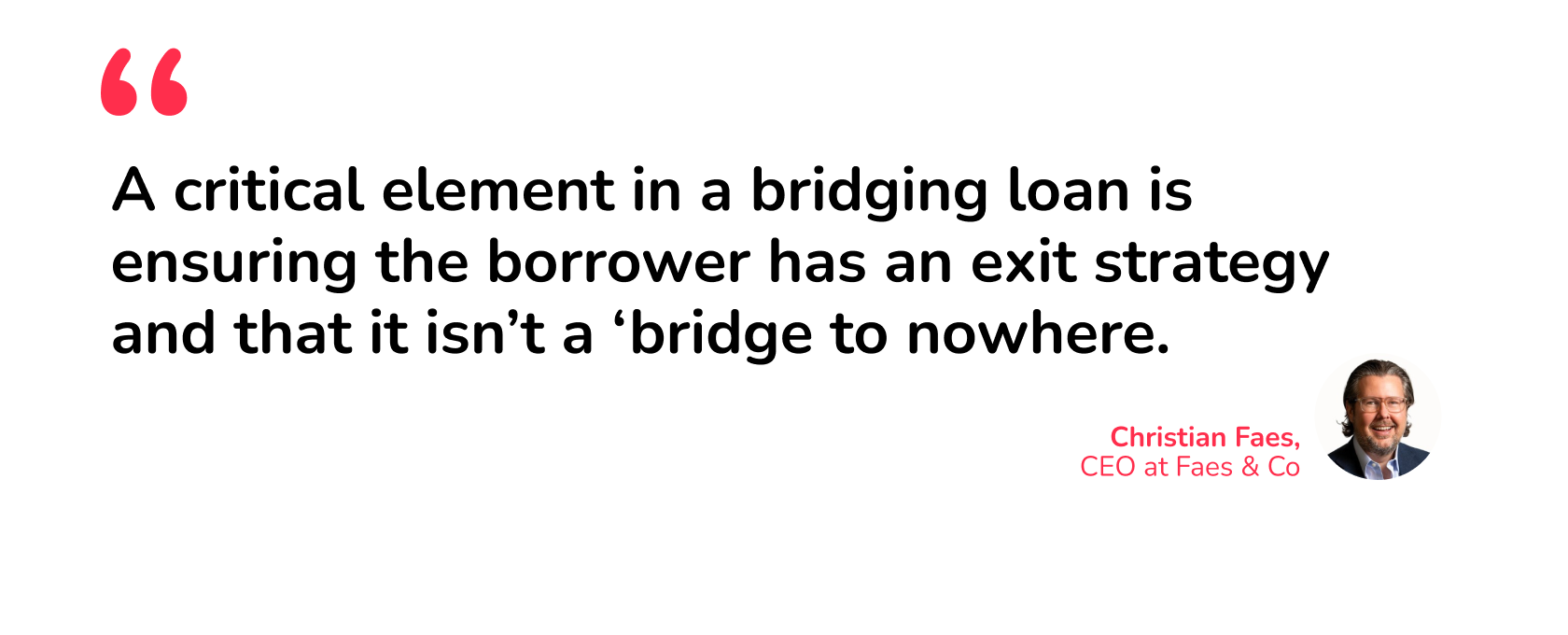

\“A critical element in a bridging loan is ensuring the borrower has an exit strategy and that it isn’t a ‘bridge to nowhere' (or, for the borrower, a foreclosure),” says Christian Faes, CEO of Faes & Co, a CRE investment firm.

A simple exit strategy usually means refinancing into permanent financing once the asset stabilizes or selling the property after completing the value-add plan, whichever supports repayment without stretching the hold period.

Lenders want cash-flow clarity, not presentation fluff, so the plan should show how the asset reaches stabilization without leaving gaps in repayment logic.

2. Know your numbers before you apply

Most commercial real estate bridge programs in 2026 land inside familiar ranges: LTV usually sits near 60–70%, and some sponsors secure higher LTC when they bring a strong track record.

Terms vary, but higher interest rates and interest-only structures remain common. Investors can protect themselves by modeling the impact of monthly payments across multiple lease-up speeds, not just the preferred one.

3. Strengthen your sponsorship profile

In a tighter credit environment, the sponsor matters as much as the asset. Lenders want proof you can run the project: completed renovations, past refinances, and clean repayment histories all help.

A strong sponsorship file marks you down as a reliable borrower in many lenders’ eyes and will reduce the chance of questions about risk, especially on value-add or reposition projects that need hands-on management.

4. Prepare for stricter underwriting – but more lender activity for clean deals

We’ve mentioned how regulators have pushed banks toward more cautious reviews, without going into specifics.

You can expect close attention to environmental items, appraisal swings, and your credit score, along with a tougher read on whether the capex timeline holds up in today’s construction environment.

Underwriting standards may be tighter, but that doesn’t mean capital has dried up. Well-structured projects still attract lenders, and 2025 data shows that activity is picking up for borrowers who bring clean numbers and a realistic execution plan.

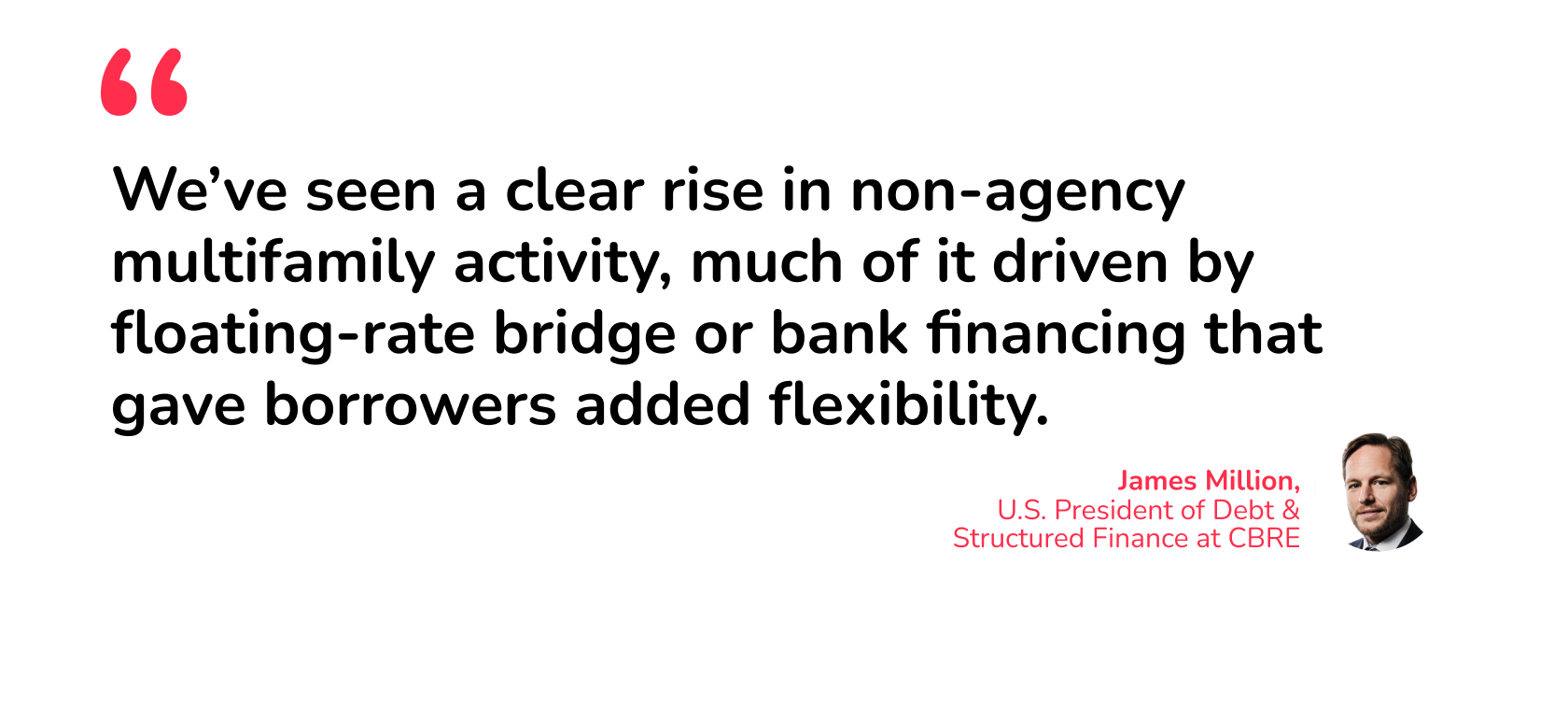

“Despite volatile Treasury rates, credit spreads continued to compress, and lenders became more active in 2025,” says James Millon, U.S. President of Debt & Structured Finance at CBRE. “We’ve seen a clear rise in non-agency multifamily activity, much of it driven by floating-rate bridge or bank financing that gave borrowers added flexibility.”

5. Plan for rate and fee stack-up

Higher-rate short-term financing creates breathing room, but it also adds friction if the timeline drags.

Origination charges, extension costs, and prepayment rules can affect your exit, especially when the refinance falls later in the year.

A clear read on fees helps you avoid surprises that shrink returns once cash flow tightens during renovations or lease-up.

6. Use fast capital to secure the deal while you finalize the larger loan

Many investors strengthen their position early by posting a sizable refundable deposit through fast EMD financing.

That move locks the property under contract and keeps negotiations steady while the broader capital stack, whether bridge or long-term financing, comes together.

How to use commercial bridging loans strategically in 2026 – with help from Duckfund

A bridge loan in commercial real estate only delivers its full value when it sits inside a clear plan. Investors who treat it as a structured step – not a last-minute rescue – tend to protect their capital, move faster, and keep leverage in negotiations.

As a CRE investor, winning deals in 2026 comes down to controlling the contract early and keeping your financing timeline flexible. If you map out the exit path upfront and manage cash-flow timing, you can avoid the rush that causes most bridge loans to stumble.

This is where fast liquidity matters. Many investors rely on fast earnest money deposit funding to book the property before the rest of the capital lis secured.

Duckfund plays that role well: we give you the upfront control needed to hold the deal in place while your bridge lender finalizes terms. That single move removes the pressure that slows many real estate projects and gives you a clean runway to execute the plan.

If you're securing a time-sensitive commercial acquisition or preparing for a bridge loan, Duckfund can help you confidently control the deal while you finalize your financing strategy.

Want to beat your rivals to the next deal? Sign up for Duckfund and unlock fast, flexible funding in minutes.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence