7 Commercial Real Estate Lessons to Apply in 2026

Last year offered several instructive commercial real estate lessons that can help propel this year's investing strategies.

It was a year that forced investors to rethink how to get property deals over the line, with many assumptions that carried the industry through the low-rate years no longer holding up under scrutiny.

The market is entering the year with clearer visibility and more realistic pricing, which is helping cautious momentum return to both leasing and capital markets.

At the same time, economic uncertainty, policy risk, and uneven asset performance remain part of the equation.

This article focuses on the commercial real estate lessons that matter most coming out of 2025. First, we look at what last year revealed about risk, capital, and decision-making across the industry. Then we turn to what the 2026 CRE market is shaping up to be, and how professionals can prepare for the year ahead with clearer expectations and stronger fundamentals.

7 commercial real estate lessons we can learn from 2025 (and what they mean for 2026)

Lesson 1: Selective liquidity beats “no liquidity”

Scare stories about liquidity “disappearing” in 2025 didn’t come to pass, but it did narrow.

Capital was available, but only for commercial properties with strong fundamentals, including durable cash flow, leverage, and a clear execution path. Transactions that relied on aggressive rent growth or vague exits stalled, while simpler, better-underwritten deals continued to trade.

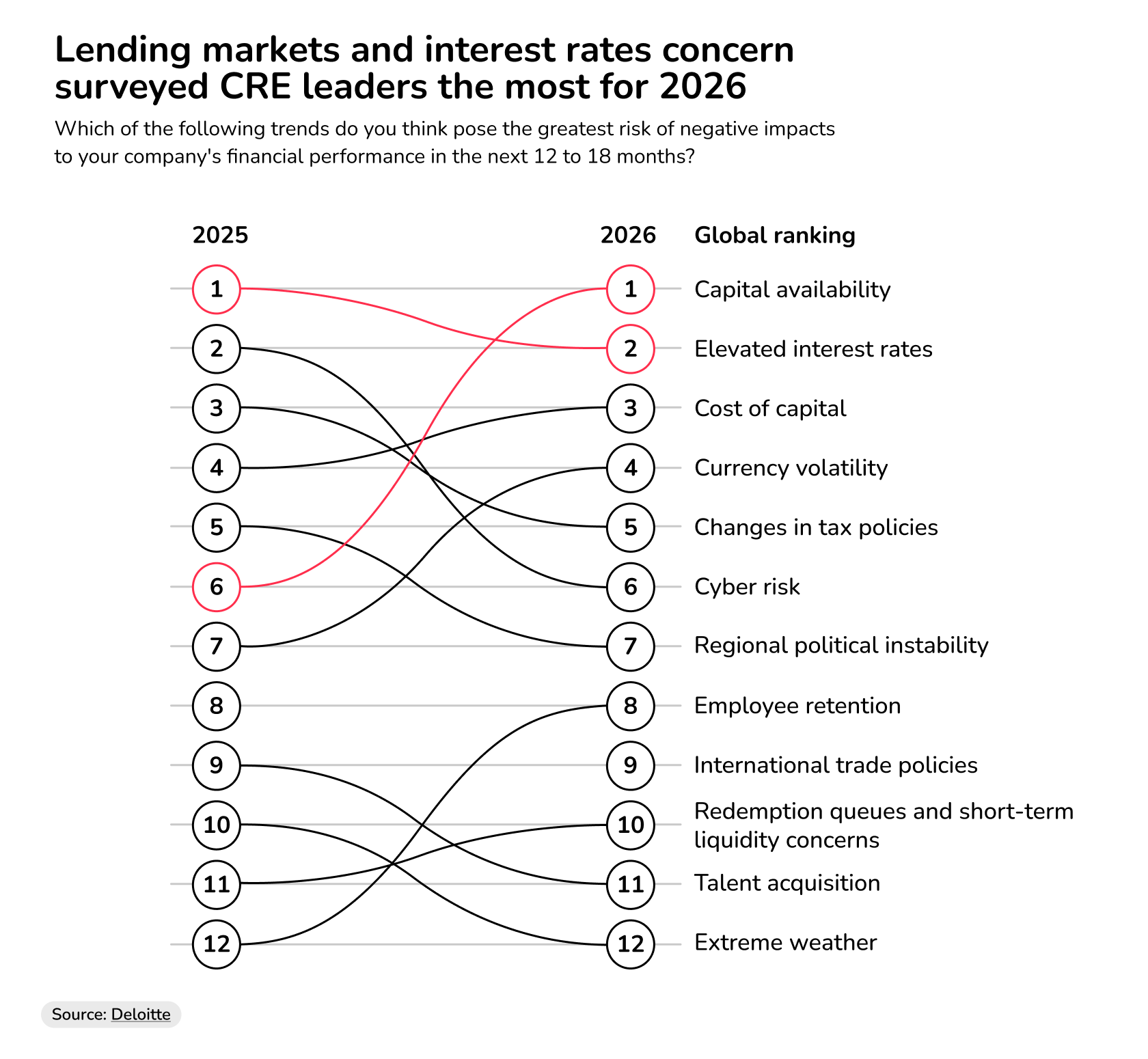

This pattern shows up repeatedly in capital markets commentary from Deloitte, an industry leader in this regard, which notes that capital availability shot up to the top investor concern, from sixth place at the start of 2025, even as investors stayed active.

What this means in 2026 for CRE professionals

Pipeline screening in 2026 starts with financeability. Factors such as NOI, DSCR sensitivity, and refinance options now matter as much as location or design.

If we take Deloitte’s recommendation to focus on prioritizing “agility in capital allocation decisions” at face value, then CRE professionals should focus on execution-ready deals. This includes deals with flexible alternative CRE financing options, realistic timelines, and enough downside protection to adjust if market conditions shift.

Lesson 2: 2025 was an underwriting reset, not a rate-cut story

Many 2025 business plans failed for the same reason: they assumed lower rates would arrive in time to save them.

When borrowing costs stayed high and lenders remained cautious, weak underwriting was often identified as the cause. Deloitte backed this up, advising CRE leaders to “recalibrate how they evaluate deals, properties, and their debt strategies; factor in higher financing and exit cap rates in underwriting”.

What this means in 2026

Underwriting in 2026 must now stand on its own. Deals should work with conservative exit pricing and realistic rent growth, with any rate relief viewed as upside rather than a requirement.

As Deloitte points out, resetting underwriting assumptions and stress-testing income and refinancing should now be standard practice for serious real estate investment decisions. Structures that only work under ideal conditions are unlikely to attract lenders or equity in the year ahead.

Lesson 3: Policy risk became a real cost, not background noise

Policy shifts in 2025 had some very real consequences. Tariffs increased material costs, while immigration constraints tightened labor. Uncertainty in federal funding also disrupted confidence.

These impacts are well documented by J.P. Morgan, which linked policy uncertainty directly to downturns in development feasibility and dealmaking sentiment.

“Tariff changes have already impacted building material costs,” said Ginger Chambless, Head of Market Insights, J.P. Morgan Commercial Banking. “For example, steel, aluminum, and copper parts are all subject to a 50% tariff. Other building material costs could also be subject to finalized reciprocal rates and trade agreements with varying trade partners.

What this means in 2026

In 2026, policy risk belongs inside the pro forma. Development budgets should be built around labor availability, material pricing volatility, and timing risk.

J.P. Morgan’s outlook also stresses the need for scenario planning around shutdowns or regulatory delays, especially where approvals or public funding are involved.

For real estate professionals, the ability to explain these risks clearly to lenders and partners is now part of basic deal execution.

Lesson 4: Legacy debt and new debt became two different markets

One of the clearest commercial real estate lessons learned from 2025 was the split between existing loans and new originations.

Legacy debt ran into maturity walls and valuation gaps, while new loans quietly returned on repriced assets with tighter structures. Deloitte and others characterize this as a bifurcated CRE loan market, shaped by refinancing pressure rather than a lack of capital.

Deloitte’s research highlights the growing role of private credit, preferred equity, and alternative capital sources. According to them, they are the driving force behind a resurgence in access to debt capital: private credit funds alone accounted for 24% of US CRE lending volume in 2025, exceeding the 10-year average of 14%, which shows how much the market’s funding mix has changed.

What this means in 2026

CRE professionals need a clear maturity map across portfolios and acquisition targets. Some assets will refinance, others will require recapitalization, and some may need to change hands.

Alternative funding is set to play a key role. This shift affects everyone – from lenders and investors to brokerage teams structuring deals – because capital stacks in 2026 are no longer standardized or interchangeable.

Lesson 5: Flight-to-quality is permanent, and obsolescence is accelerating

High-quality assets continued to perform, while weaker ones struggled to lease or refinance. This was true of multifamily but especially visible in office buildings, where demand concentrated in newer or upgraded space.

“High-quality office space has good demand from end users,” said Burke Davis, Head of Real Estate Banking at J.P. Morgan. “Lower quality space is at risk of obsolescence. That could mean upgrades, but more likely repurposing buildings for different uses.”

What this means in 2026

In 2026, capex determines whether an asset stays competitive or gets left behind. Colliers points out that obsolete office properties are being removed from inventory through conversions, which tightens vacancy for viable buildings and accelerates the split between winners and stranded assets.

Owners of weaker properties need to decide early: do they upgrade, repurpose, or exit before time and vacancy narrow the options?

Lesson 6: Execution replaced capital as the real bottleneck

By 2025, it became clear that in some growth segments, access to capital alone was no longer enough to deliver new supply. In areas like digital infrastructure, demand remained strong, and financing was available, yet development was increasingly concentrated in a small number of markets that could actually execute. Power availability, permitting timelines, zoning, and local coordination emerged as the real gating factors.

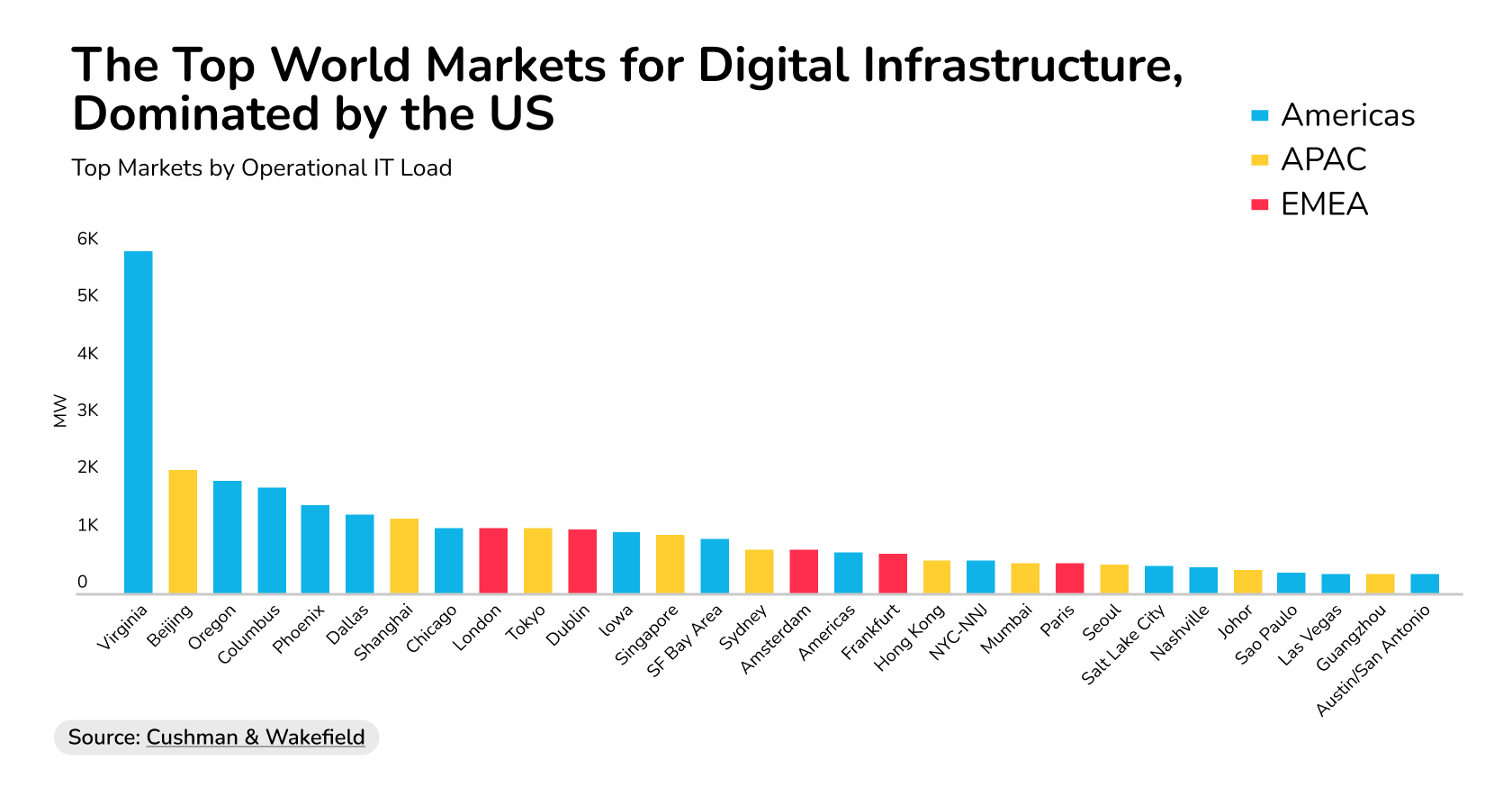

Deloitte’s research shows this dynamic most clearly in data centers, where demand continues to outpace supply even as new construction pipelines are often fully pre-leased. At the same time, research from Cushman & Wakefield shows that operational capacity has clustered in infrastructure-ready markets with established utilities and scalable systems. The graphic below shows this concentration, with the U.S. – particularly Virginia – accounting for six out of the top eight markets.

The takeaway? In today’s commercial real estate industry, projects move forward where barriers are lowest.

Source: Cushman & Wakefield

Taken together, these signals show that having capital is no longer enough. Projects move forward only where execution is realistically achievable.

What this means in 2026

Infrastructure risk now needs to be underwritten as early as land and capital. Utility access, interconnection timelines, permitting pathways, and local political dynamics should be treated as core feasibility issues, not downstream considerations.

Deloitte also emphasizes partnerships as a practical response to these constraints, which include working with local operators, utilities, and specialized partners to reduce execution risk. In 2026, many of the biggest development risks sit outside the balance sheet.

Lesson 7: Technology only matters if it protects NOI

In 2025, the gap widened between tools that actually improved performance and those that looked good in demos.

Technologies that helped lease space faster or control operating costs were effective. Investors also found tools that improved visibility across portfolios to be valuable. Yet others stalled once budgets tightened and expectations rose.

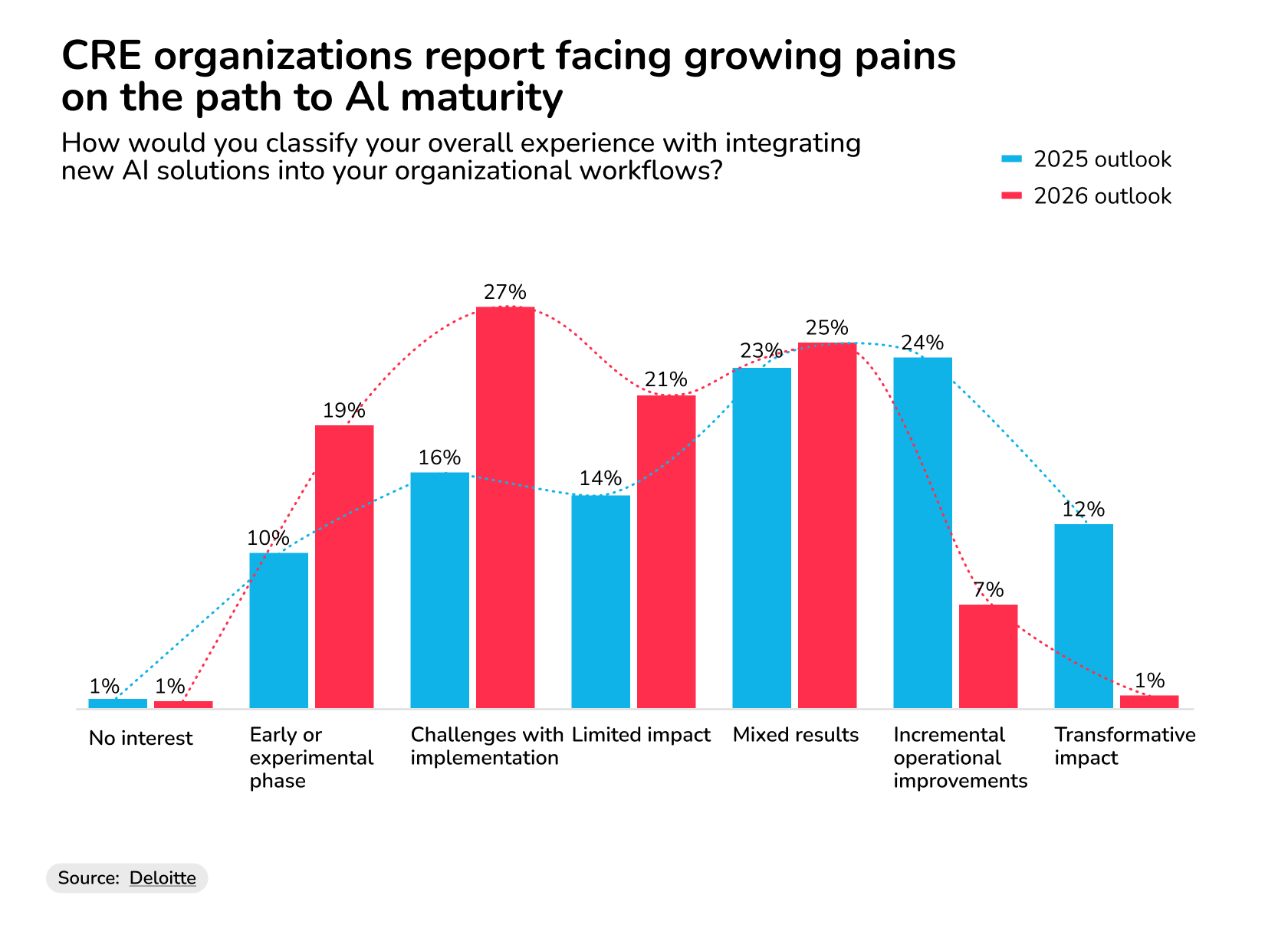

Deloitte’s latest survey data captures this shift clearly: 27% of CRE organizations report challenges with implementation – a rise from 16% last year. These obstacles range from technical hurdles to a lack of internal expertise and resistance to change.

Obstacles Among CRE Firms in Implementing AI

Source: Deloitte

Clearly, AI hype hasn’t disappeared; it just met with reality.

What this means in 2026

In 2026, technology decisions need to be tied to outcomes that investors and lenders care about. These include leasing velocity, tenant retention, expense control, and risk monitoring.

Deloitte also emphasizes the importance of human oversight to reduce operational and compliance risk. For commercial real estate professionals focused on professional development, the priority should be practical, in-depth skills that support underwriting, asset management, and decision-making.

Technology earns its place in the stack by strengthening NOI, not by sounding innovative.

What the 2026 CRE market looks like – and how to prepare for it

Stabilization replaces speculation

If we learn commercial real estate lessons from last year, 2026 might well become a year of stability rather than a rebound.

Expectations appear to be more grounded as pricing has mostly reset. There appears to be less guesswork around where deals can actually trade, and the research backs this up. Cushman & Wakefield and Colliers point to firmer fundamentals and improving visibility, even as performance varies by asset quality and location.

How to prepare

Focus market analysis on places where leasing, pricing, and transactions are already functioning. It’s good to have momentum, but durability matters more.

Operations and NOI protection drive returns

Value creation in 2026 leans heavily on execution. Occupancy, expense control, and tenant retention are doing more of the work across most property types. This shift shows up consistently in lender feedback and investor behavior.

How to prepare

Treat property management and leasing as value drivers, not support functions. Small improvements in NOI now have a bigger impact on valuation and financing outcomes.

Public and private markets are still misaligned

Public real estate pricing lagged private markets through much of 2025, creating valuation gaps that may narrow as capital markets normalize.

Industry commentary from Nareit suggests this divergence won’t persist indefinitely.

How to prepare

Carry out financial analysis for metrics like REIT performance, public-to-private spreads, and recent closed sales. These signals often move before sentiment does. Even if they aren’t that useful at first, knowing how to analyze them is a key part of real estate education.

Capital is coming back, but with rules

Funding conditions in 2026 are better than a year ago, but not perfect.

Capital availability may be improving, but investors are prioritizing structure, downside protection, and income stability over growth for its own sake.

How to prepare

Build lender-ready materials early. Be clear on downside cases and refinance paths, not just entry pricing.

A real estate finance strategy is part of the investment thesis

In this cycle, how a deal is funded can matter as much as what’s being acquired or developed – be it commercial or residential real estate.

Banks, private credit, preferred equity, and joint ventures all play roles, but they aren’t interchangeable. Commentary from J.P. Morgan underscores a market where forcing the wrong capital onto the right asset can undo an otherwise solid deal.

This means knowing how to finance a commercial property smartly rather than just going with whatever works

How to prepare

Match assets to the right capital source. Understand lender preferences, covenants, and timelines before you commit, not after. Clean deals move faster, so work closely with a lending partner early to pressure-test structure, assumptions, and timing before going to market. This is a smart idea for professionals at any stage of their commercial real estate career.

Prepared beats aggressive in 2026

The industry professionals positioned to win in 2026 aren’t the loudest or the most bullish. They’re the ones who absorbed the commercial real estate lessons of 2025, including underwriting conservatively and communicating risk clearly. They’re also the ones who know how to fund thoughtfully and be able to move quickly when the time is right.

How to prepare

Invest in in-depth commercial real estate analysis, real-world execution skills, and continuing education. In this market, credibility opens more doors than bold forecasts.

Learn from CRE mistakes of the past and get yourself a funding partner.Sign up for Duckfund in minutes to unlock fast, flexible funding for your next deal

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence