Due Diligence vs Earnest Money: Everything You Need to Know in 2025

Knowing the difference between the two could save you a lot of time…and money.

You've found the perfect commercial property. The numbers align, the location is prime, and it has bags of potential. Now the real work begins: getting the deal over the line.

Knowing the nuances of the buying process in today’s competitive commercial real estate (CRE) market is essential when a misstep can cost you the deal.

Getting your head around due diligence vs. earnest money is a key example of this, but it’s a topic that many buyers struggle with.

In this guide, we’ll look at the difference between due diligence and earnest money and how a lack of funding for either can impact a CRE transaction.

After reading it, you’ll know the answers to the following:

- What is due diligence money?

- Is due diligence refundable?

- What is the due diligence fee in 2025?

- What is earnest money?

- Is earnest money refundable?

- Can you get earnest money back during due diligence?

- What is earnest money in 2025?

- What is the difference between due diligence vs. earnest money? A comparison

- Due diligence vs. earnest money: How to get funding

Due diligence and earnest money are simple concepts, but both require funding. Contact Duckfund to find out how we can help you lock down that CRE property you’ve got your eyes on.

What is due diligence money?

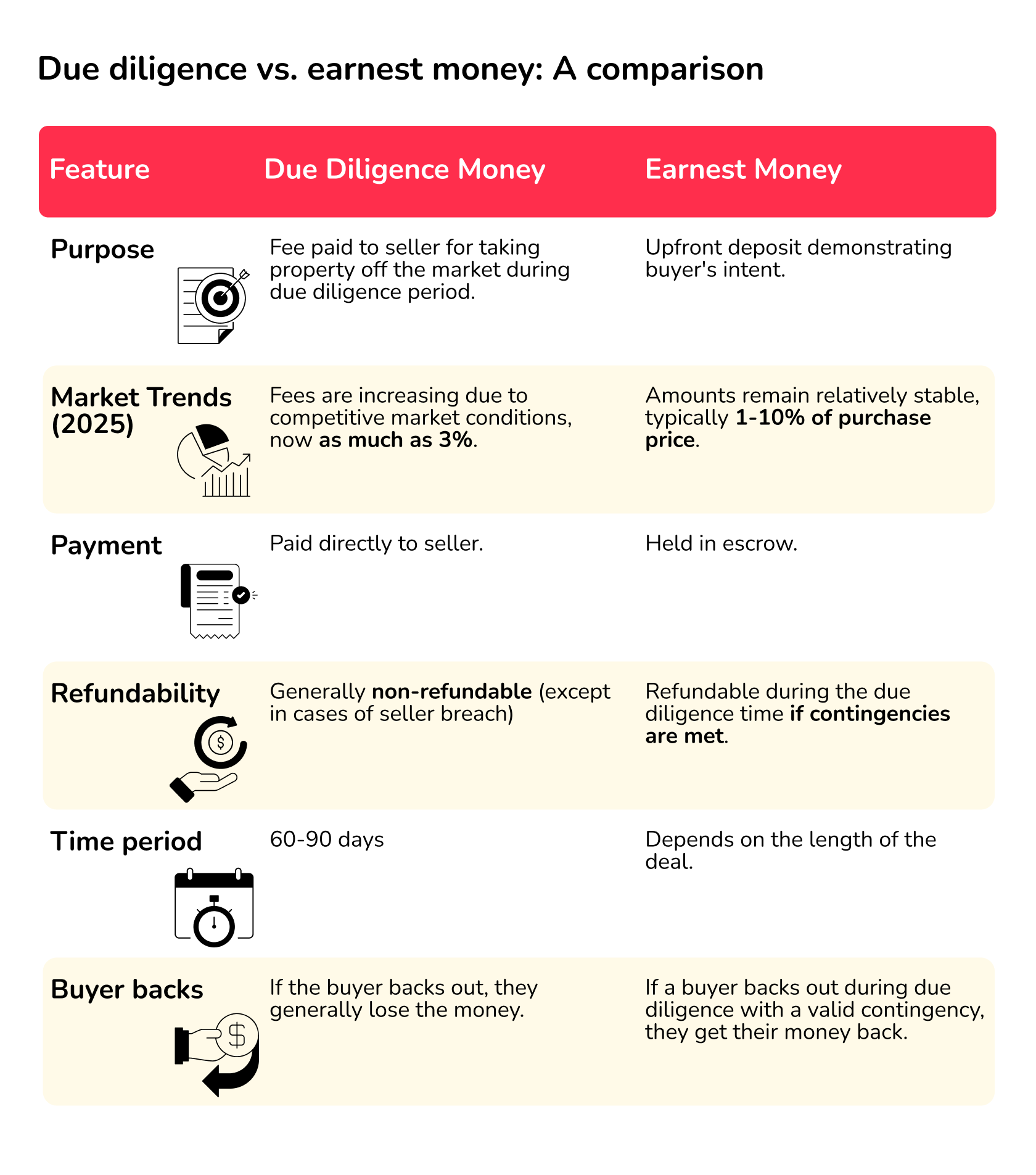

Due diligence money is the fee that a buyer pays a seller in a real estate transaction for them to take the property off the market so that they can carry out checks.

Compensating the seller in this way shows them two things:

- The buyer’s commitment to purchase the property (subject to checks)

- The buyer’s potential financial ability to complete the transaction.

Due diligence is becoming increasingly important across the United States, particularly in states like North Carolina, where it’s now a standard part of CRE transactions.

“Sometimes, you may hear someone refer to this fee as 'good faith' money, as it is a fee that you are giving the buyer directly to let them know that you are serious about buying the property,” says Ryan Fitzgerald, writing for NC-based Raleigh Realty. “It can also be considered a down payment towards the home's purchase price, as the due diligence money will be credited back to the buyer at closing.”

Once paid, the buyer has a certain timeframe (agreed between the seller) in which to complete the checks, which will usually include a property survey, inspection and a title search.

This due diligence process is a little like a property’s medical check-up. It lets potential buyers diagnose issues and make informed decisions about structural and interior health. With this information, they can work out if it’s likely to be a successful real estate transaction for them.

First-time home buyers, too, often must stump up this amount and factor it into the price of their home.

Is due diligence refundable?

As a general rule, due diligence is not refundable, especially in places where it’s a key part of transactions, like Raleigh, NC. We asked several real estate agents there, “Can you get due diligence money back in NC?” The answer was a resounding no.

A non-refundable fee is risky for buyers, who will lose it if they decide to pull out for any reason, but it does have one advantage. “Because due diligence is a cast-iron signal that the buyer is serious about getting to the closing table, they can use it to stand out from other offers”, says realtor Justin Daniel.

What is the due diligence fee in 2025?

The average due diligence fee in 2025 is higher than ever, thanks to an intensely competitive market.

“In normal times, we would see a due diligence amount of 1% (of the property sale price) on the table, but the current market has pushed this up to as much as 3%,” says Fitzgerald.

This means the due diligence fee for a million-dollar commercial property (the average sale price in the US) has risen from $10,000 to $30,000.

As mentioned, this fee can be used as leverage to make an offer look better than rivals. The higher it is, the more likely the seller is to accept. However, buyers risk losing this amount if the deal doesn’t complete.

Pro tip: Always seek realtor and legal advice when negotiating the due diligence fee. With it being non-refundable, the risks of going along (and making errors) are too high.

Buyers are thus conducting deeper, more thorough checks to justify these prices. What was previously “check-the-box” diligence is now becoming more comprehensive, with more buyers and sellers opting to employ third-party firms to carry it out for them.

As a result, a typical due diligence period is now between 60 to 90 days, up from 45 days, according to merger and acquisition experts TKO Miller.

The lower-to-middle market is feeling the largest impact caused by these changes, but the ripple effects are being felt right across the real estate market.

What is earnest money?

Earnest money is a type of good-faith deposit, or down payment, that a buyer makes to a seller during a real estate transaction.

Like with the due diligence fee, it demonstrates the buyer's serious intent to purchase the property, but there are certain differences.

This earnest money deposit is typically held in an escrow account until the purchase agreement is finalized. The seller, therefore, does not receive the amount until the deal is complete.

Is earnest money refundable?

The earnest money deposit affords the buyer more space than the due diligence fee: if the deal falls, then the escrow agent or a real estate attorney in charge of the account simply sends it back. However, this depends on the status of the due diligence process.

“Unlike the due diligence fee, the earnest money is refundable if the sale is canceled within the due diligence period,” says Ryan Fitzgerald. “If the buyer decides not to buy the home after the due diligence period and before closing, both the due diligence money and earnest money are forfeited”.

Like with the due diligence fee, the earnest money amount is subtracted from the property purchase price if the deal is successful. The buyer then sends the remaining balance (plus closing costs).

Can you get earnest money back during due diligence?

The buyer can normally get your earnest money back during the due diligence period, but it depends on the terms of the purchase contract and when you apply for it.

Here's a breakdown:

- If, during the due diligence period, you (the buyer) find issues that make you want to back out of the deal, you can typically do so and receive their earnest money back.

Purchase agreements often include contingencies, such as:

- Home inspection contingency: If the inspection reveals significant problems.

- Financing contingency: If the buyer cannot secure a mortgage.

- Appraisal contingency: If the appraisal comes in lower than the purchase price.

- If these contingencies are not met, the buyer can usually get their earnest money back.

- If the buyer backs out after the end of the due diligence period, they may forfeit their earnest money. This means it’s very important to understand the dates and terms of the purchase agreement.

In essence, the due diligence period is designed to protect the buyer, and the earnest money is often refundable during that time, provided the reasons for backing out are within the agreed-upon contingencies.

What is earnest money in 2025?

Earnest money has stayed at a consistent level over the last few years. Investors typing “How much is earnest money for commercial property?” into Google are likely to find similar results to a few years ago.

As a rule of thumb, expect earnest money to come in between 1 to 5%, however, this could reach as much as 10% in high-demand CRE markets.

Pro tip: Never make the earnest money payment directly to the seller. It should always go to the escrow agent.

What is the difference between due diligence vs earnest money? A comparison

In the current market, knowing the difference between due diligence money and earnest money is fundamental. Both play important but different roles in demonstrating a buyer's commitment and bringing about a successful real estate transaction.

Due diligence money, a non-refundable fee paid directly to the seller, grants the buyer a specific time period to thoroughly investigate the property, akin to a medical check-up that helps them make informed decisions. This fee has seen a significant increase due to competitive market conditions.

Earnest money, on the other hand, is a refundable deposit held in escrow and is typically credited toward the purchase price at closing. Earnest money is normally refundable, contingent upon meeting agreed-upon contractual terms.

Both these serve to protect the interests of both parties and push the deal toward completion.

Due diligence vs earnest money: How to get funding

Earnest money and due diligence fees are both key factors for someone trying to work out how to buy commercial real estate, but it can be hard to fund them.

Lenders" typically don't cover these upfront costs, leaving investors to bear the burden. For those dealing with a competitive local market, these high fees increase the challenge, often forcing them to dip into their private capital (if they have it).

Often, however, this capital is tied up in other ventures, meaning investors can miss out on important property deals to rivals.

This funding gap has led to a new wave of alternative lenders that provide earnest money or due diligence fees within 24 hours of acceptance.

Flexible and affordable, they are helping commercial investors secure deals ahead of rivals, often allowing them to work on multiple projects at once – a vital tool in today’s tough lending environment.

Ready to make your next CRE deal happen? Sign up to Duckfund and find out how our flexible funding can put you ahead of your rivals.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence