EMD Lending: How to Close More Real Estate Deals, Faster

Deals in commercial real estate rarely wait for perfect conditions. They reward the people who can move decisively.

Yet, moving fast can feel risky.

Earnest money deposit (EMD) funding solves this dilemma by letting you secure deals quickly while keeping most of your capital liquid.

Most investors and developers run into the same three problems when trying to tie up a deal, including:

- Six-figure sums sitting idle in escrow for months during due diligence

- Losing competitive deals simply because they can’t post a deposit fast enough

- Being forced to choose between one “safe” deal and several riskier “high-potential” ones.

This is exactly where smooth, well-structured EMD funding becomes a strategic advantage.

Instead of freezing cash in escrow, you can place refundable deposits through a dedicated EMD lender and strengthen your offers. You can even keep multiple deals moving in parallel.

In this guide, we’ll break down what EMD lending actually looks like in practice for commercial real estate right now, including how it works step by step, when it makes sense to use it, and how to avoid the common pitfalls – so you can grow your portfolio without slowing your deal flow.

We’ll cover:

- What is an EMD in real estate?

- What is an EMD lender?

- When should you use EMD lending (and when not to)?

- Why EMD lending helps you win more deals

- How EMD lending works (step-by-step)

- Who can benefit from EMD lending?

- How much does EMD lending usually cost?

- The biggest mistakes with EMD escrow (and how to avoid them)

- How to secure your next deal with Duckfund’s EMD financing

What happens when you pair EMD lending with a funding partner built on speed? Contact Duckfund to discover how our flexible financing can secure your next deal in just 48 hours.

What is an EMD in real estate?

An earnest money deposit (EMD) is a payment a buyer makes to a seller to show good faith when entering into a purchase agreement.

In commercial real estate, it helps secure the property because it shows the buyer's commitment to the deal while they complete the necessary due diligence and financing requirements.

During this period, the deposit is held in a third-party escrow or title account until the buyer and seller either proceed to closing or formally terminate the transaction.

This is where EMD lending comes in. Instead of parking large amounts of their own capital in escrow, investors can use short-term EMD funding to cover the earnest money deposit and lock in the opportunity. They also get to keep their liquidity free for other deals.

If you’re the buyer, EMD lending doesn’t replace traditional financing or fund the acquisition itself: it simply removes the upfront friction of placing the deposit. You’re then free to move deals forward without slowing down your capital or your pipeline.

Is EMD usually refundable?

In most commercial real estate transactions, an EMD is refundable, at least at first. This is what’s known as a soft deposit.

During the inspection or due diligence period, the buyer can typically exit the deal and recover the funds, as long as they follow the terms set out in the purchase agreement.

The deposit only becomes hard (non-refundable) once specific conditions are met, for example, when the inspection window expires or when the buyer formally waives due diligence. At that point, the EMD is usually forfeited if the buyer walks away.

This is why escrow structure matters. With proper EMD escrow, the deposit is held in a third-party escrow account managed by a neutral title company or closing attorney. In more protective setups, such as sole-order escrow, the funds can only be released with the buyer’s explicit approval, which adds an extra layer of control.

In short, EMDs are usually refundable by design. Whether they actually remain refundable depends on three things: your inspection period, your contract language, and how the escrow is structured.

Get those right, and the deposit stays as the safety mechanism you need it to be.

What is an EMD lender?

Coming up with the earnest money deposit is one of the most common (and least glamorous) problems in real estate, and an EMD lender’s job is to solve it.

As a specialist financing provider that funds the earnest money deposit on your behalf, they help move a real estate deal forward without you having to wire a large sum from your or your business’s account just to get started.

Instead, the EMD lender places the deposit directly into a third-party escrow account or with a title company and keeps the transactions clean and secure. They can also review the purchase agreement, the amount of earnest money, and the closing timeline as part of the process.

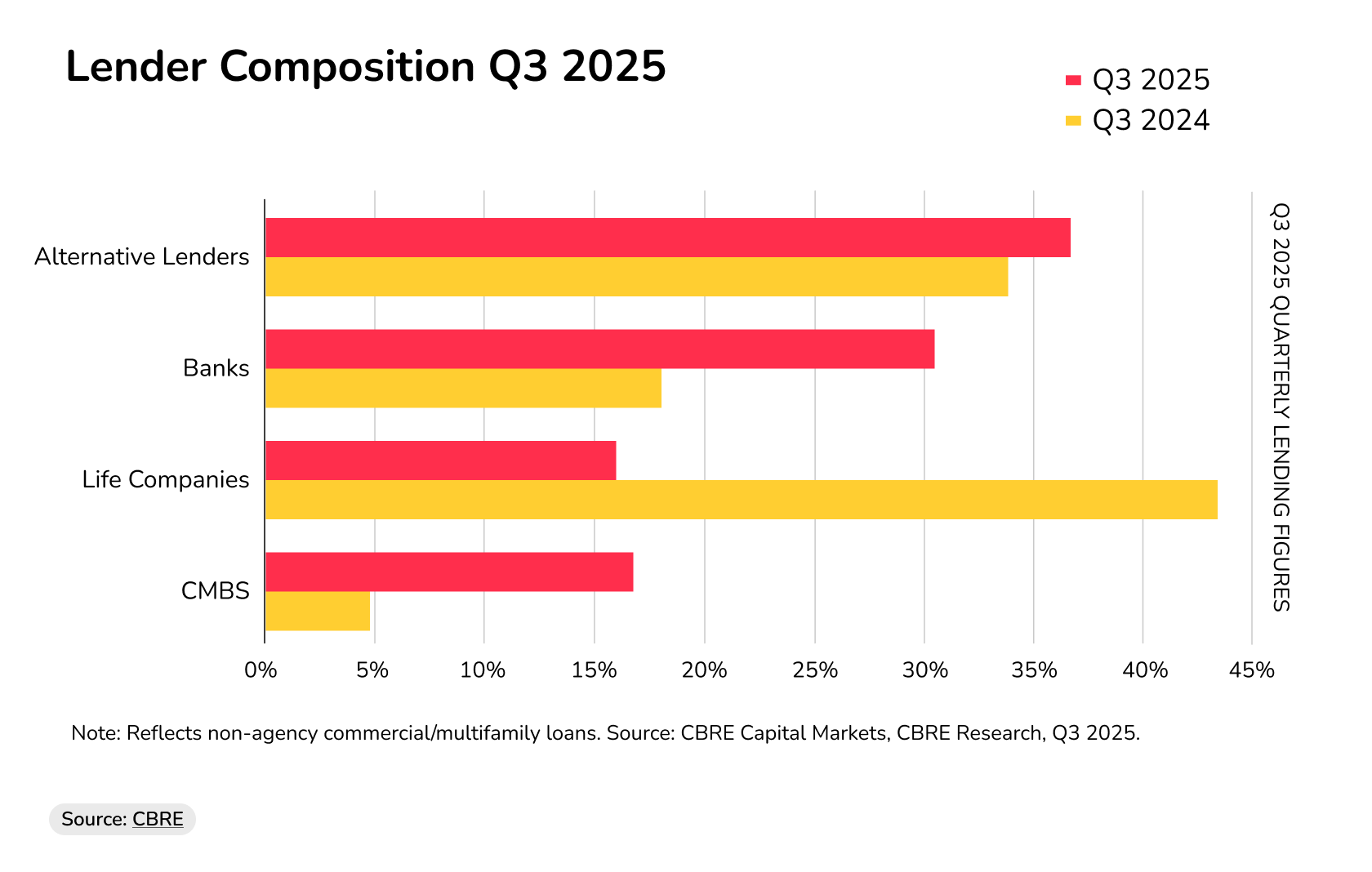

This role has become more common as the CRE lending market has shifted. In recent years, data shows a steady rise in alternative lenders operating alongside traditional banks, creating space for more specialized financing models like EMD lending. This space grew to 37% of the US market share in 2025, according to CBRE.

The Rise in Alternative Lending (2024-2025)

Source: CBRE

As capital becomes more expensive and deal timelines stay tight, more real estate investors are turning to alternative and private lenders for this kind of targeted financing.

Banks don’t fund deposits, and parking six figures in escrow is rarely a great use of cash flow. Modern EMD lenders like Duckfund help you work around this, with fast approvals and less hassle.

The result? You close deals without slowing down your pipeline.

When should you use EMD lending (and when not to)?

EMD lending works best when timing matters more than anything else.

It’s a short-term financing tool designed to help you move quickly on real estate investments without putting unnecessary strain on your cash flow.

In practice, EMD lending makes the most sense when:

- You’re in a competitive bidding situation and need to stand out

- You’re running multiple deals in parallel and want to stay liquid.

- The deposit is fully refundable during due diligence.

In these scenarios, EMD lending turns speed into a real advantage, helping you secure investment opportunities without overcommitting capital too early.

It becomes less useful when the fundamentals of the deal are weak. For example:

- The title is unclear or legally messy

- The margins are so tight that fees erase the upside

- The timeline stretches far beyond what’s reasonable for short-term funding.

In other words, EMD lending amplifies good deals, but it doesn’t rescue bad ones.

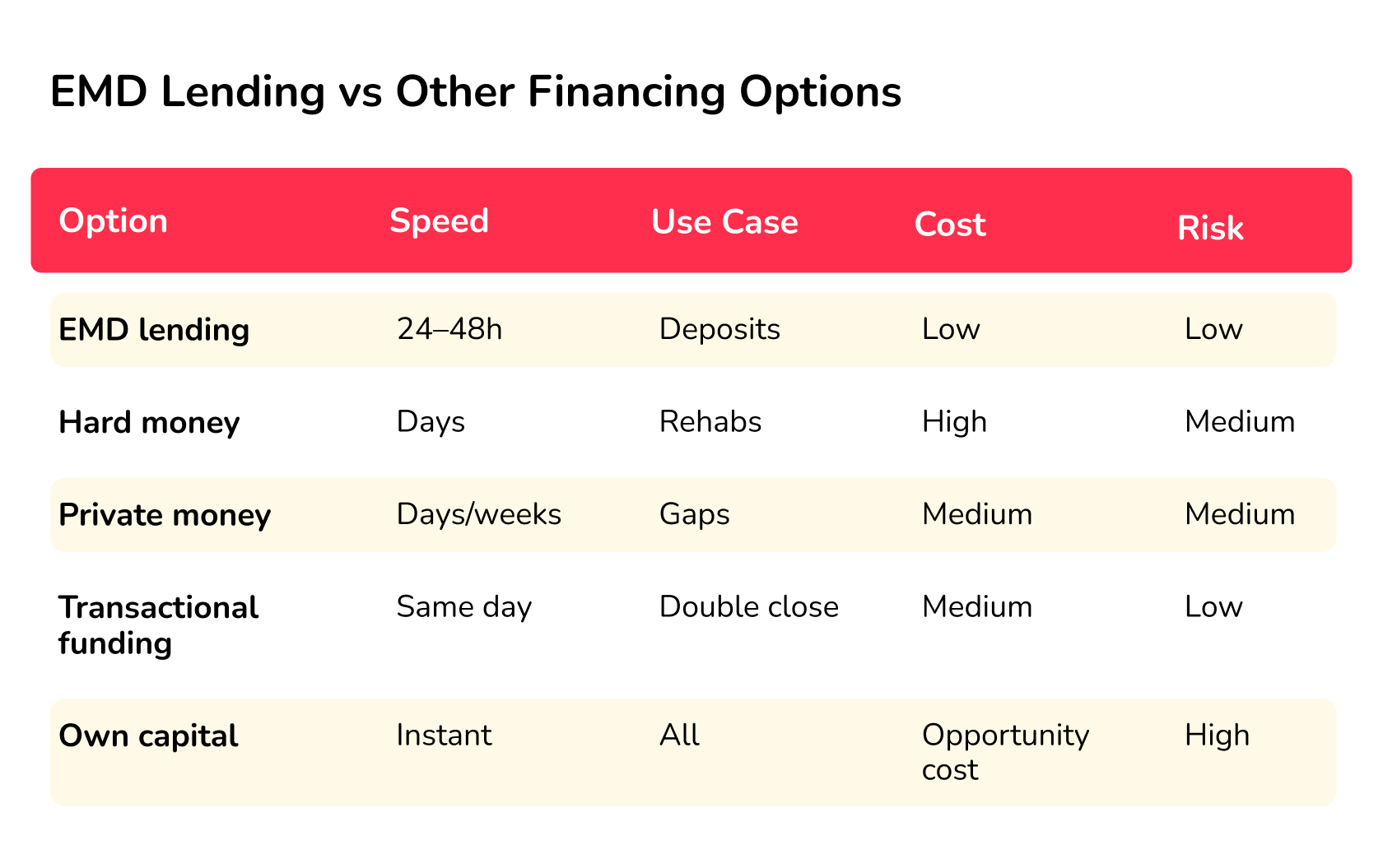

If you’re unsure which financing solution fits your situation, it helps to see how EMD lending compares with other common options like private money, hard money, or transactional funding.

EMD Lending vs Other Financing Options

EMD lending sits in a very specific (and very useful) niche. It doesn’t fund the deal but gets it started by making sure the deposit is in escrow, and the seller takes the property off the market.

Why EMD lending helps you win more deals

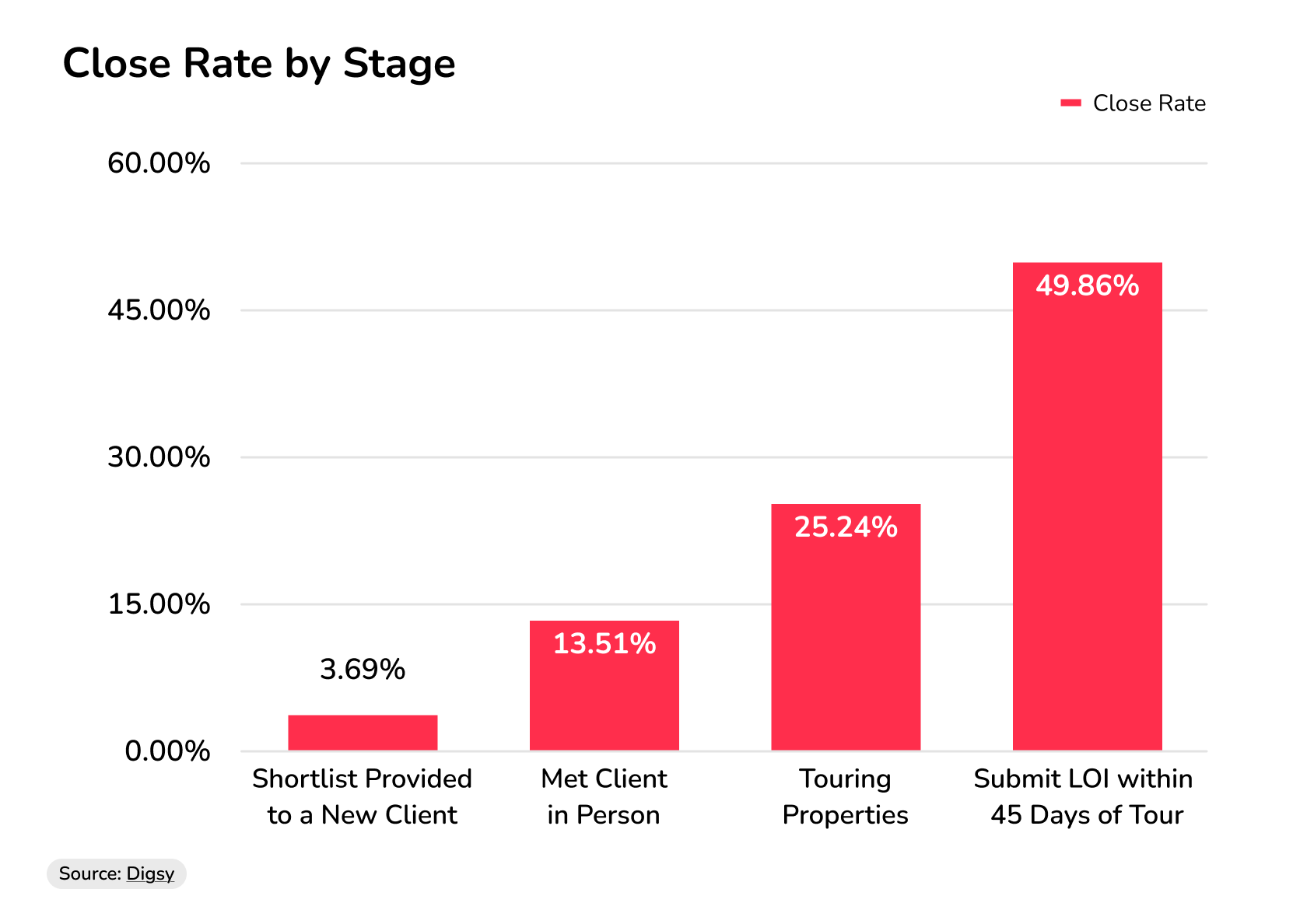

In commercial real estate, deal speed is a core competitive advantage. The faster you can move from handshake to funded escrow, the more often you end up controlling the asset.

Real CRE transaction data backs up that intuition. Industry research of more than 2,000 CRE deals by lead generation platform Digsy.AI shows that the probability of closing a deal rises sharply as buyers move decisively through early stages, with close rates jumping to nearly 50% once an LOI is submitted within a defined timeframe.

How Speed Influences CRE Deals

Source: Digsy

In other words, the faster you progress from interest to action, the more likely the deal is to hold together.

Effective EMD lending makes that transition smoother by taking the deposit off your internal to-do list.

If approved quickly, buyers can secure their earnest money deposit within a few business days, which keeps momentum high and conversations short.

Instead of juggling internal sign-offs or chasing partners for capital, you can go straight to a signed purchase agreement and look like the most organized person in the room.

There’s also a simple truth about seller psychology: funded deposits feel reassuring. A larger, promptly wired deposit sends a clear signal that you’re serious, capable, and ready to execute, which is often more persuasive than a slightly higher price paired with uncertainty.

On the capital side, EMD lending keeps things flexible. Your cash stays available, your cash flow stays healthy, and your pipeline stays active. You’re free to pursue multiple opportunities at once, respond quickly when new deals appear, and close deals without your capital constantly playing catch-up.

In a tight market, that kind of operational calm can make a big difference.

How EMD lending works (step-by-step for CRE)

When done well, EMD lending should remove friction from the very start of a real estate deal.

Instead of scrambling to free up cash or delaying timelines, you use short-term earnest money deposit funding as a form of targeted gap funding, or just enough capital to keep the transaction moving.

Duckfund’s EMD lending is designed to be fast, simple, and focused on one goal: helping you secure a real estate deal without tying up your own capital.

“Customers find our service useful when they have a property they want to inspect, but do not have the capital at hand for the deposit,” says Anna Kogan, CEO and Founder of Duckfund.

Here’s how we help buyers nail their deal down within 48 hours.

1. Letter of Intent (LOI) accepted

You’ve agreed on headline terms with the seller. The only thing standing between you and control of the asset is the earnest money deposit.

2. Apply for EMD funding

You submit a short online application with the purchase agreement, property details, and the amount of earnest money you need. There’s no heavy paperwork, and no drawn-out underwriting: Duckfund focuses on the deal, not traditional credit checks.

3. 24-hour approval

Duckfund reviews the transaction, timeline, and escrow structure. In most cases, we issue approvals within one business day, making us one of the fastest soft deposit providers available for earnest money in commercial real estate.

4. 48-hour deposit wired

Once approved, Duckfund sends the funds via secure wire transfer directly to the relevant title company or closing attorney, into a third-party EMD escrow account.

5. Held in escrow

The deposit sits safely in escrow while you complete due diligence. Your own capital stays liquid, protecting cash flow and keeping other investment opportunities open.

6. PSA signed, and the deal moves forward

With the deposit funded, the purchase contract becomes binding, and the seller takes the property off the market.

7. Closing or refund

At closing, you either repay the EMD to Duckfund from proceeds, or it gets refunded if the deal exits during the inspection period.

How Duckfund Works in 2 Minutes

Who can benefit from Duckfund’s commercial EMD lending?

EMD lending shows up in different ways depending on the type of investor, but the goal is always the same: control the real estate deal without overcommitting capital too early.

Active CRE investors

EMD lending is a great liquidity tool for active CRE investors running multiple transactions at once.

Instead of having large deposits tied up across several PSAs, they use EMD funding to keep cash flow flexible. This makes it easier to manage parallel deals and stay responsive when new opportunities appear.

Developers

EMD is a key feature of commercial property development finance, including land acquisition and predevelopment.

Deposits can sit in escrow for months while zoning, permits, and feasibility studies are completed. EMD lending allows developers to secure sites without freezing capital that’s better used for design, legal work, and early-stage costs.

Syndicators

Syndicators use EMD lending to control assets before the full raise is complete.

If they can fund the deposit upfront, they’re then free to sign the PSA, lock in terms, and begin investor outreach with a real asset under contract. It also means they avoid trying to raise capital for commercial real estate based on a hypothetical opportunity.

Wholesalers (CRE only)

EMD lending can also support double closings for CRE wholesalers, without them risking their own funds.

They can use it as a form of short-term transactional lending to place the deposit, secure the contract, and complete the exit once the end buyer is ready. This keeps the real estate deal moving without unnecessary exposure.

EMD lending gives a wide range of buyers a practical way to secure opportunities while keeping capital available and deal flow steady.

This is ideal for commercial real estate, where the advantage tends to follow the parties who can move decisively and stay liquid at the same time.

How much does EMD lending cost?

The cost of EMD lending is usually small compared to the size of the deal, and often far smaller than the cost of freezing your own capital in escrow.

Most EMD lenders price based on the loan amount (or the amount of earnest money) and the expected timeline because the capital is only used for a short period.

This contrasts with some private or transactional lenders who structure fees based on purchase price, a legacy practice that can lead to disproportionately high costs on big deals where only a small deposit is advanced.

Earnest money itself is often around 1%–5% of the purchase price in commercial transactions, depending on how competitive the market is and what the seller requires.

Duckfund charges a fee of 2.3%–3% of the deposit amount, with a discounted rate of 2% available for deposits above $1M held for four months or longer. Fees are structured as LP soft costs and pass through at closing, so they’re built into the deal’s cost structure rather than paid out of pocket upfront. This is important when you’re managing liquidity across several deals.

All fees are disclosed in advance and paid upfront, based on the planned due diligence period.

The biggest mistakes with EMD escrow (and how to avoid them)

Most problems with EMD escrow come from moving too fast without enough structure. Ironically, the same urgency that makes EMD lending powerful can also create unnecessary risk if a few basics are missed.

Here are the most common mistakes investors make (and how to avoid them):

- Letting the deposit become non-refundable too early

This usually happens when due diligence timelines are unrealistic. Always align your inspection period with your actual ability to underwrite, raise capital, and clear title. - Wiring outside escrow

If someone asks you to send a wire transfer directly to an individual or LLC, that’s a red flag. Deposits should always go through a third-party escrow or title company, not to a non-neutral agent.

“Investors frequently accept escrow agents affiliated with the seller,” says Anna Kogan. “ When a dispute arises, a non-neutral escrow agent can delay or complicate the release of funds.”

- Unclear PSA terms

Vague purchase agreements create hassle later. Make sure the PSA clearly defines refund conditions, deadlines, and what happens if the deal doesn’t close. - Ignoring timing risk

Overly optimistic closing dates can lead to rushed decisions, extra closing costs, or lost deposits. Build a buffer into every timeline.

When deposits are refundable, escrow-held, and backed by clear documentation, EMD lending stays what it’s meant to be: a low-risk tool for moving deals forward, instead of a source of expensive surprises.

How to secure your next deal with Duckfund’s EMD financing

For CRE investors and developers operating in a tight market, the real advantage is more than just finding good deals, it’s being able to act on them faster than everyone else.

That’s exactly what Duckfund is built for. Instead of offering broad loan programs, Duckfund focuses exclusively on EMD funding and soft deposit financing, which means every part of the process is optimized around one thing: getting your deposit into escrow as quickly and smoothly as possible.

With fast, streamlined approvals and funding typically completed within 48 business hours, Duckfund helps you move from accepted offer to funded deposit without the usual delays, paperwork, or internal capital reshuffling.

The result is simple but powerful. You strengthen your offers, keep your cash flow flexible, and stay in control of multiple deals at once – all without tying up your own capital unnecessarily.

“What’s amazing about Duckfund’s model is that it keeps your balance sheet where it’s at,” says Robert Clippinger, a leading property investment expert . “You’re using outside capital to control the deal, and your lender still sees you have the reserves you need for their deal. It lets you keep your money in the bank and keep your deal flow moving.”

For sponsors raising equity, the benefit extends even further. “By sourcing the EMD from Duckfund, investors get to kill two birds in one stroke: tie up a property, and open the floor for equity conversations,” says Anna Kogan.

In practice, that means control first, capital second, and momentum that carries all the way to closing.

If you’re ready to move faster, protect your liquidity, and put yourself in a position to win more deals, Duckfund’s EMD financing is built to help you do exactly that.

Ready to grow your company’s portfolio? Sign up for Duckfund and unlock fast, flexible EMD funding in minutes.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence