Earnest Money Deposits in Real Estate: Rules, Risks, and Best Practices for CRE Investors

Earnest money deposits (EMDs) are no longer a side detail in commercial real estate (CRE); they are often the first real test of whether a deal will move forward or fall apart.

In today’s competitive CRE market, understanding how EMDs work can be the difference between winning a property and losing it.

Yet despite their importance, many CRE investors still misinterpret how EMDs function, largely because most explanations are rooted in residential real estate (RRE). This gap leads to costly assumptions around deposit size, refundability, timing, and buyer protection.

In this guide, we break down the role of EMD in real estate, focusing on how they operate in commercial transactions. You’ll learn what they are, how they differ from residential deals, and how smart investors use them strategically to stay competitive and protect capital.

We’ll cover:

- What is EMD in real estate?

- How does EMD in CRE differ from RRE?

- How does earnest money work in practice?

- Securing consistent earnest money with EMD lending

Do you want consistent access to EMD financing for all types of CRE deals? Contact us to learn more about how our financing product can give you an advantage in competitive markets.

1. What is EMD in real estate?

An earnest money deposit (also known as a good faith deposit) in real estate is a portion of the property’s purchase price that the property’s seller expects you to pay as a sign of serious intent to purchase.

From the seller’s perspective, an EMD is a good way to separate serious buyers who are financially ready and committed to purchase from those who are only doing a market survey or exploring their options.

“Today, EMD is used in more than 90% of all commercial transactions,” according to Steve Case, a financial services consultant at Insurance Hero. “If you want to show a seller you're serious, the quickest way to do so is by paying a deposit.”

With the payment of EMD in real estate, you can:

- Kickstart the due diligence period: The due diligence period is a window within which you can inspect the property and certify that everything is as it should be. This includes verifying the property’s title and ensuring there are no environmental concerns.

- Negotiate the details of the deal: Many sellers become more open to serious negotiation once you have paid the EMD.

- Get exclusive rights to the property: In many markets, you can include an exclusivity provision in both the initial Letter of Intent (LOI) and the final Purchase and Sale agreement (PSA). It legally prohibits the seller from negotiating with, marketing to, or accepting offers from other buyers during your due diligence window.

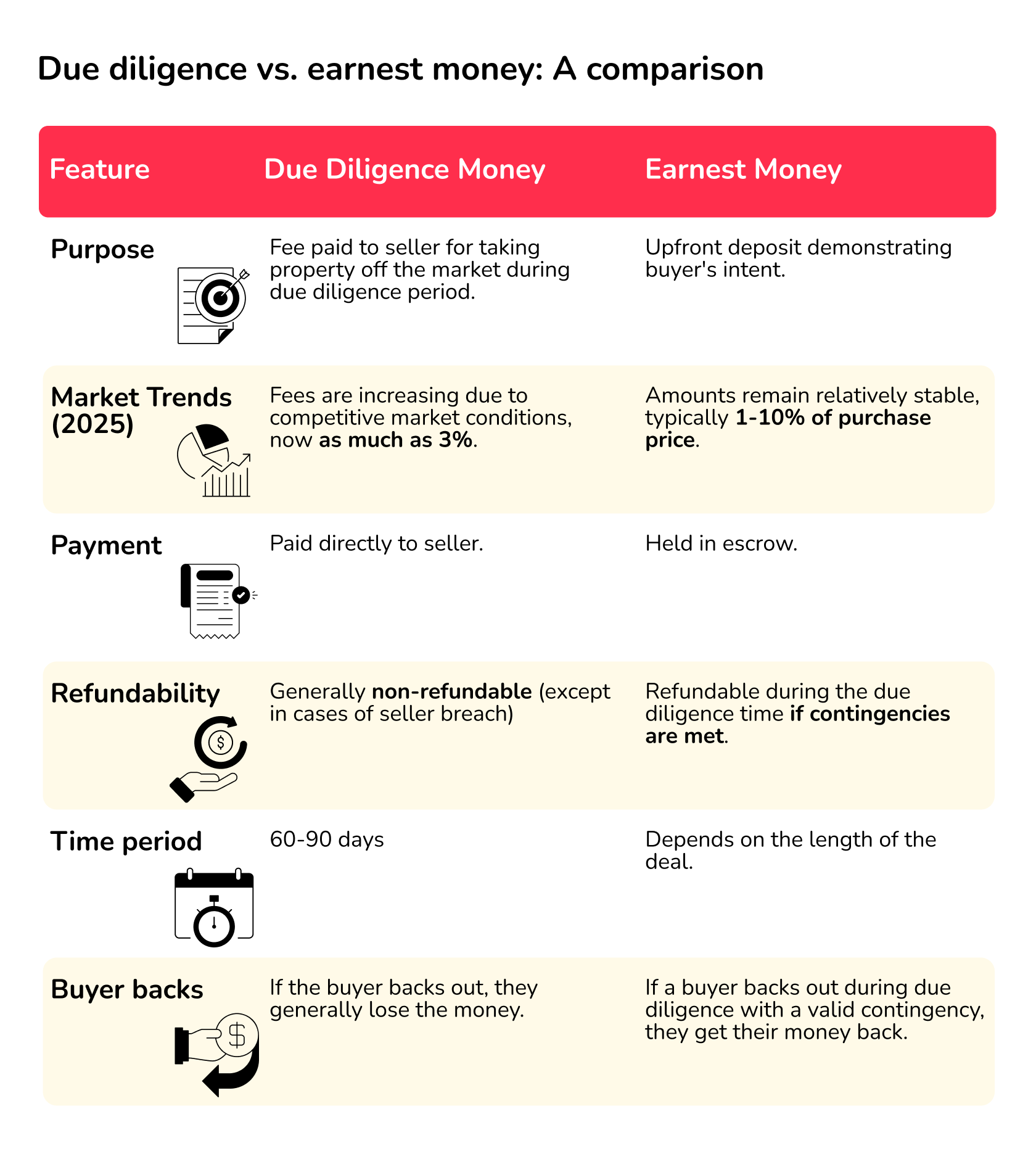

However, in certain markets, this exclusivity might require the payment of due diligence money. This is a non-refundable fee that gives you the exclusive right to the property until the end of the due diligence period. While the due diligence money is common in RRE (especially in North Carolina, South Carolina, and Texas), it is not usually required in CRE.

Below are the differences between due diligence money and earnest money:

- Buy time to raise capital: While conducting due diligence, you can also start exploring equity and debt capital solutions to finance the property’s purchase price.

2. How does EMD in CRE differ from RRE?

Let’s now explore some of the important details about the use of earnest money in CRE and how they differ from RRE.

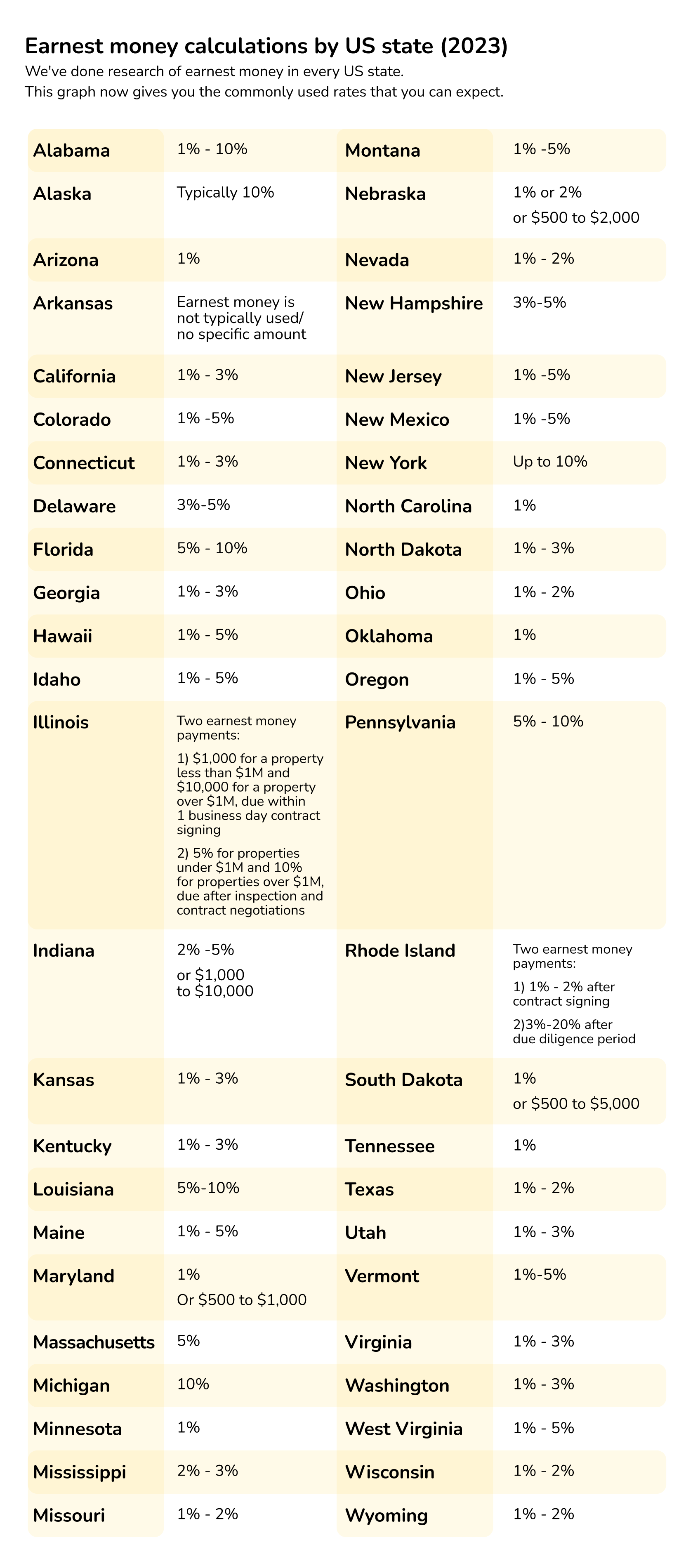

Amount required

How much is earnest money for commercial property in the US?

Though there are no stated amounts required by law, you can expect to pay an average of 3-10% for commercial properties. This is higher than the average rate in the RRE market (usually between 1-3%).

“In contrast to residential real estate, where EMDs typically serve as a simple indicator of good faith, commercial deals may require more substantial deposits due to the higher dollar amounts at stake,” according to Catherine Mack, the CEO of House Buyer Network, a real estate company.

Below are some specific ranges for US states:

Refundability

We will discuss refundability further below.

But for now, you should note that while RRE deals tend to have multiple contingencies designed to protect buyers (financing contingency, appraisal contingency, inspection contingency, title contingency, home inspection contingency, and home sale contingency, among others), CRE deals rely on the due diligence period.

In other words, CRE deals tend to have a longer due diligence period, after which it becomes almost impossible to get an EMD refund if you back out of the deal.

“Commercial EMD structures are usually more complex because CRE transactions involve longer diligence periods, more financing variables, lease analysis, environmental reviews, and operational risk assessment,” according to Deepak Shukla, CEO of Pearl Lemon Properties.

Buyer protections

Given that many average Americans purchase residential properties (as a part of the American dream), the government is more interested in that market. There are standardised rules, such as state-approved forms and escrow neutrality, designed to protect home buyers (especially first-time homebuyers).

In contrast, since your goal as a CRE buyer is to make a profit, the onus is on you to design agreements and contracts that will protect your interests.

“Unlike residential, there's no standard percentage or timeline; everything is negotiated, which means your accountant and attorney need to be aligned before you sign anything, because the tax and cash flow implications of a forfeited deposit can be significant,” according to Michael Spitz, an accountant with experience in the real estate market.

Nature of escrow

In the homebuying process, EMDs are usually held by brokerage title companies under state-regulated escrow rules. On the other hand, EMDs in CRE can be held by escrow agents, attorneys, realtors, title companies, and even sellers themselves in off-market deals.

Negotiability

Though there is an average range of EMDs in CRE, there is usually a greater room for negotiation compared to RRE (where contracts are standardized).

“In CRE, the deposit is usually more negotiable and tied closely to deal size, due diligence timelines, financing risk, title review, and how competitive the property is,” according to Tricia Watts, founder of MaxNet Homes, a real estate company. “For new investors, the biggest rule is to match the deposit to the risk.”

This is especially evident in competitive markets where multiple CRE buyers compete for the same property. In such situations, you can offer to pay a higher EMD amount than what the seller requests.

Similarly, since CRE depends on the due diligence period, you can negotiate a longer due diligence period while offering to pay a higher EMD amount.

Also, some buyers have negotiated a lower sale price for higher EMD amounts.

3. How does earnest money work in practice?

Now that we have clarified the unique features of earnest money deposits in commercial real estate, let’s see how it works in practice.

We do this by answering (in a logical order) some of the questions CRE investors like you have about earnest deposits.

Who keeps the earnest money?

As said above, earnest money deposits for CRE deals are held in an escrow account operated by escrow agents, attorneys, or title companies. Only in unique circumstances (like off-market transactions) do sellers keep the earnest money.

What is the earnest money used for?

There are two main uses of the earnest money when the deal becomes successful: to finance a part of the closing costs or the down payment.

Since CRE transactions rely on detailed negotiations, how the earnest money is used depends on your agreement with the seller. This agreement will usually be stated in the PSA, also known as the purchase agreement or contract.

The PSA is a custom and attorney-drafted document that includes details such as the escrow company that will be employed, the EMD amount, what the EMD will be used for, the purchase price, the property’s description, conditions for refundability, contingencies, due diligence period, representations, warranties, and covenants, among others.

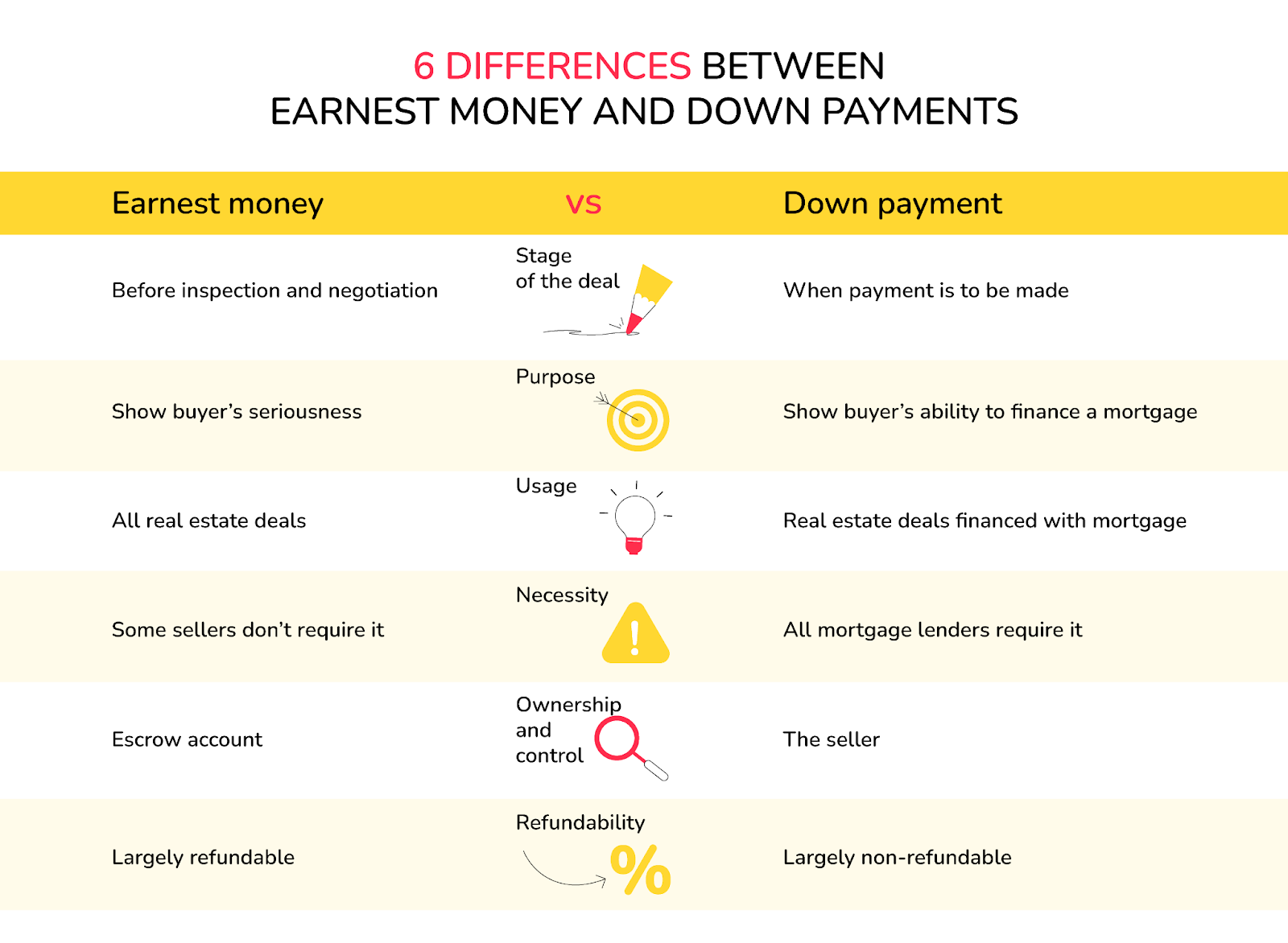

Is an EMD the same as a down payment?

It’s also important to clarify the relationship between earnest money and down payment.

The down payment is a portion of the purchase price that the lender expects you to provide. It is usually seen as a sign of your financial competence to repay the loan, and it is a determinant of the loan amount.

It’s obvious that while the earnest money can be used later as a part of the down payment, the two are not the same. For one, the earnest money is paid at the beginning of the deal, while the down payment comes into play when the deal is ready to be finalized.

Below are some of the other differences:

Can you get your earnest money back?

Are earnest money deposits refundable?

This is one of the most important questions that CRE investors have about EMDs.

Thankfully, the answer is not complicated.

As said above, CRE deals do not usually have a long list of specific contingencies. Instead, there is a broad due diligence period that covers all inspections, financials, and approvals.

If you terminate the purchase contract within the agreed due diligence period, for whatever reason, you will get your EMD back.

On the other hand, EMD becomes non-refundable once this timeframe has elapsed. The only exception is when the seller breaches the contract.

However, some CRE PSAs also include detailed contingencies that you can count on even after the due diligence period. In other words, if explicitly negotiated into the PSA, the EMD may remain refundable past due diligence if specific, hard milestones are missed. Though this is less common in CRE, it does happen.

Furthermore, some CRE deals employ a staged EMD structure where you pay a portion of the EMD before the due diligence period starts. This portion remains refundable until the due diligence period ends. Once the period ends, you pay the remainder of the EMD, and the whole amount becomes hard (non-refundable).

For example, if the total EMD is $100,000, you may pay $50,000 before the due diligence period starts. This amount is refundable until the end of the due diligence period. At the end of this period, you will pay the remaining $50,000, and the entire $100,000 become non-refundable.

Who keeps earnest money if a deal falls through?

The escrow will return the money to you if the EMD is refundable (based on the conditions above) and to the seller if it is non-refundable.

How much earnest money can you expect to pay?

As said above, the average rate ranges from 3-10%.

However, in competitive markets, you might have to propose higher EMD amounts to get an advantage. Even real estate agents now advise their clients to do this.

How much earnest money to offer in these markets depends on what the seller is already requesting, the nature of the competition, and current market conditions.

4. Securing consistent earnest money with EMD lending

As a CRE investor, you can expect to pay bigger EMDs than what is obtained in the RRE market.

Also, if you operate in competitive markets, you will usually need to propose higher EMD amounts to gain an advantage.

Yet, EMDs present certain working capital challenges.

First, why should you lock tens and hundreds of thousands of dollars in escrow accounts when you can use the money to pursue other investment opportunities? This is especially concerning since money deposited in these accounts does not earn any interest.

Second, how do you cope when you are cash-strapped but still have to deposit earnest money for a property of choice? In this case, you don’t have any problem securing financing for the purchase price, but you are temporarily illiquid to pay the earnest money and get the deal to closing.

This is where EMD lending comes in.

Instead of reducing your flexibility to pursue other deals by locking your money in escrow accounts, you can get low-cost EMD financing from EMD providers like Duckfund. This frees you up to pursue other investment opportunities where you can earn higher returns.

“Specialized EMD funding solutions like Duckfund can play a vital role for investors by providing the necessary capital to secure an EMD for attractive properties,” according to Brandon Beatty, the owner of Southern Hills Home Buyers, a real estate company. “This allows investors to present competitive offers without tying up their own liquidity, enabling more flexibility and speed in acquisition efforts.”

Also, instead of passing up opportunities due to temporary illiquidity, specialized EMD financing companies like Duckfund can provide what you need while you keep working on financing the purchase price.

“Access to EMD funding doesn't just solve a cash flow problem; it permanently expands what you can compete for,” according to Chad Silver, the CEO of Silver Tax Group, a tax law firm.

Moreover, with Duckfund, you can propose higher EMD amounts in competitive markets and get EMD financing for multiple simultaneous deals.

Furthermore, you can complete an EMD application in under two minutes and get the funds delivered to the selected escrow within 48 hours.

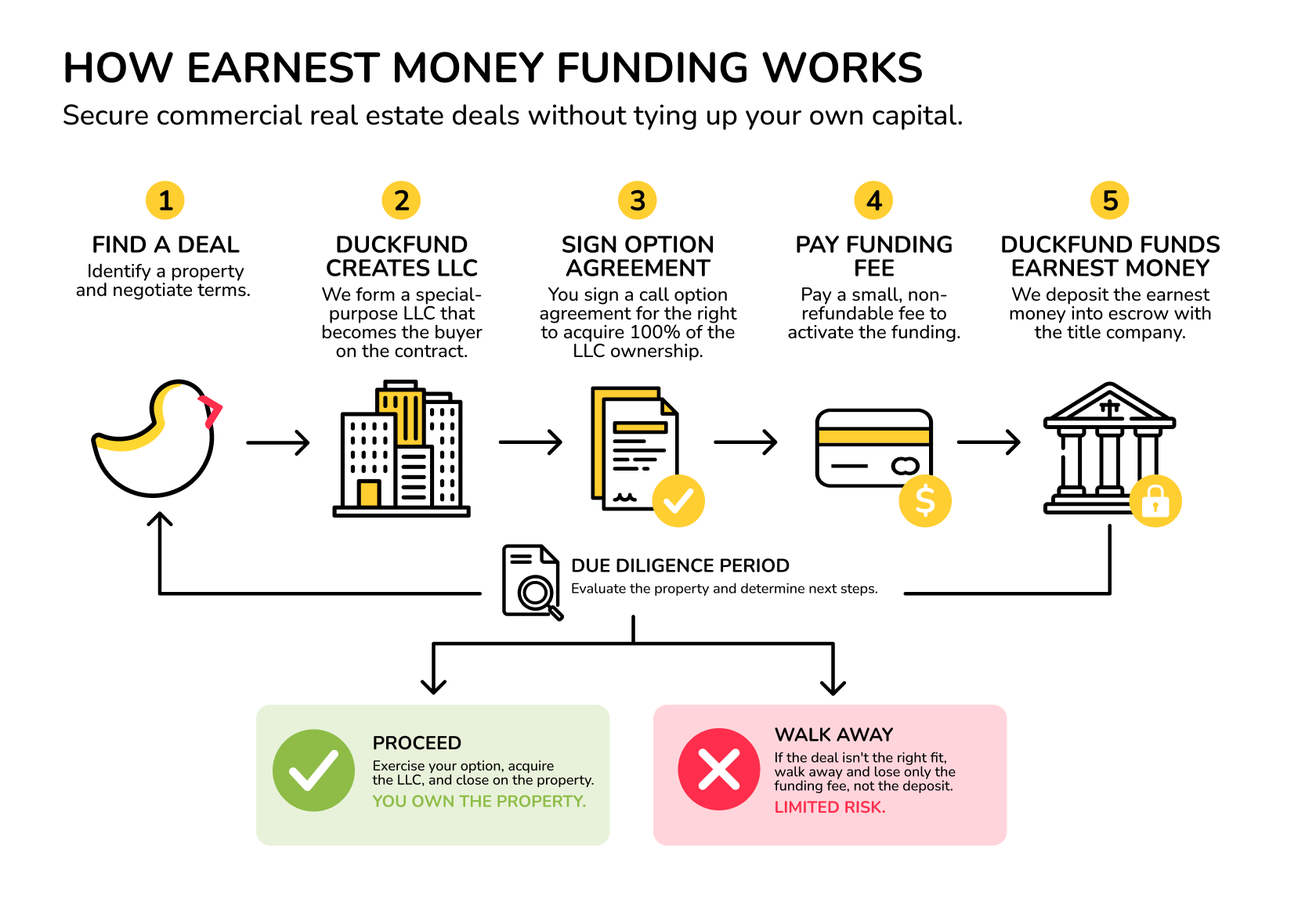

Duckfund has a low-risk approach that allows you to pay earnest money online using an LLC. This occurs in five simple steps:

- Step 1: Duckfund will create an LLC, which will act as the legal entity for the purchase.

- Step 2: You will sign a call option agreement, which gives you the right to buy 100% of the stake in the LLC.

- Step 3: At this point, you will pay the financing fee, which is a percentage of the purchase price.

- Step 4: The LLC will sign the PSA, after which the earnest money will be sent to the designated escrow.

- Step 5: If you decide to continue with the deal at the end of the due diligence period, you will repay the earnest money and get 100% stake in the LLC.

However, if you choose to cancel the deal during the due diligence period, the LLC gets a refund from the escrow, the PSA is terminated, and you won’t have to pay any cash back to Duckfund.

These steps can be summarized in the chart below:

With such a simplified process, you can safely explore various CRE deals until you find the ones that align with your investment goals.

Are you ready to secure EMD financing for all your important CRE deals? Sign up now with Duckfund for quick and convenient access to earnest money deposits for multiple simultaneous deals.

Frequently Answered Questions (FAQs)

What does earnest money deposits Mean in real estate?

Earnest Money Deposits (EMDs) are funds a buyer pays upfront to show serious intent to purchase a property. They are typically held in escrow and later applied toward the down payment or closing costs if the deal goes through.

Are earnest money deposits in real estate refundable?

Yes, but only under certain conditions. In most commercial real estate deals, EMDs are refundable during the due diligence period, but become non-refundable once that period ends unless the seller breaches the contract.

How much are earnest money deposits in real estate?

In commercial real estate, EMDs typically range from 3% to 10% of the purchase price, depending on the deal size and competition. Residential deals usually require lower deposits, around 1% to 3%.

Who holds earnest money deposits in real estate transactions?

EMDs are usually held in an escrow account managed by a third party such as a title company, attorney, or escrow agent. This ensures the funds are protected until the transaction is completed or terminated according to the contract.

Takeaways

- While residential buyers often put down 1–3%, CRE investors should expect earnest money deposits of 3–10% or more in competitive markets.

- In most CRE deals, your earnest money remains refundable during due diligence but becomes non-refundable once that period ends.

- Unlike residential real estate, commercial real estate transactions rely heavily on negotiated contracts, making legal and financial review critical.

- EMD financing can unlock more opportunities. Specialized providers allow investors to preserve liquidity, compete with larger deposits, and pursue multiple deals simultaneously.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence