How to Tell a Good Faith Deposit from Earnest Money in a CRE Deal

Look up good faith deposit and earnest money online, and you’ll get roughly the same definition.

In the residential housing market, this works. But in commercial real estate (CRE), they represent two different payments that go to different parties and often under different sets of rules.

CRE investors can use either to make a deal work, but can also put their money at risk if they mix the two financing tools. This can be very costly for six- or seven-figure deals.

This guide is about how to avoid this type of situation. We look at exactly what each deposit means in CRE, where it goes, and just how refundable each type of deposit really is.

We'll cover:

- What is a good faith deposit?

- Good faith deposit vs. earnest money deposit: the key differences

- Down payment vs. earnest money (and other terms people mix up)

- Is a good faith deposit refundable?

- How much should a good faith deposit be?

- Are good faith deposits legal in NYC?

- How to protect your deposit and keep your capital free

Not sure which deposit your deal actually requires? Contact Duckfund to find out how you can buy your property without dipping into your capital.

What is a good faith deposit?

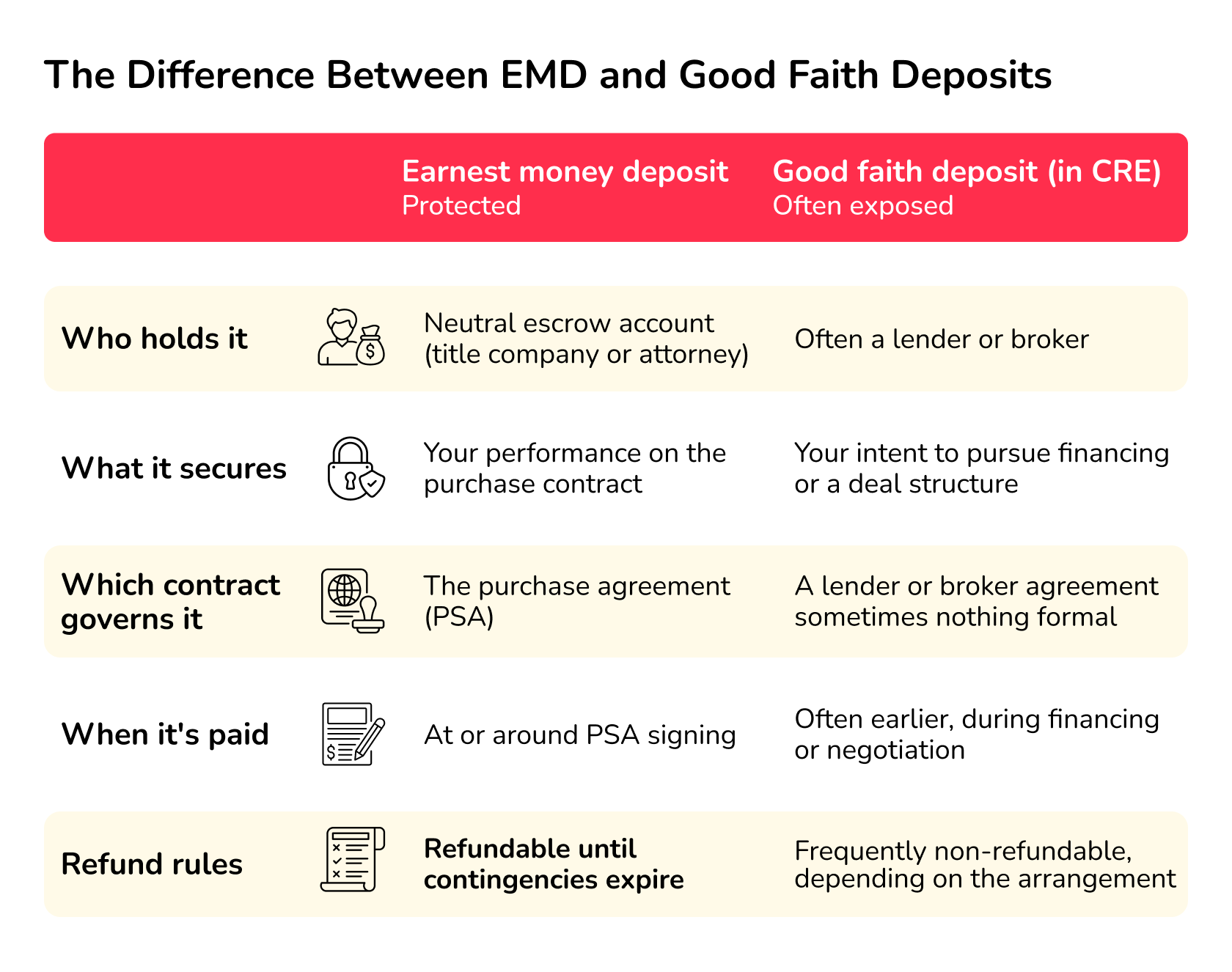

A good-faith deposit in commercial real estate is a payment the buyer makes to show serious intent in purchasing a property. The "good faith" is their honest commitment to follow through.

This type of payment is often outside the purchase contract, so it isn’t protected. Many buyers are cautious about using it for this reason.

The good-faith deposit appears early in the buying process. The buyer typically sends it to the lender (or broker) to show that they’re serious about financing, and it can cover the appraisals and legal fees that lenders often use to test whether a loan is viable.

The catch is that it’s usually not enough to secure the property itself, which is where buyers run into trouble. "Good faith money" can mean the formal escrow deposit, or it can mean an informal payment that no contract is protecting.

Is a good faith deposit refundable?

The honest answer here is “probably not”, at least not before closing.

Once a lender receives a good faith deposit, you’ve paid for work that’s probably already under way, including appraisal and underwriting. In short, you’re buying the process up front.

There are a few ways in which you could get all or some of your money back before closing.

- If the contract says so. Lenders might offer a refund if they don’t complete the work on time or correctly. There should be a clause in the contract stating this.

- They only use part of the deposit. This only happens if the GFD is used as a float against real costs – if they don’t spend all of it, then you’ll get the unused balance back.

- Misuse of funds. It’s possible that the lender acts in bad faith or misuses the funds. If so, you have grounds to launch a lawsuit, but a dispute is very likely.

There are some notable exceptions from this list, including failing to secure financing or finding out a problem with the property. These are all covered in the PSA, which typically protects your earnest money, not a good faith deposit.

Good faith deposit vs. earnest money deposit: the key differences

Let’s forget definitions for a second. We can actually see the differences between these two deposits by asking two simple questions:

- Where does your money actually go?

- What does it secure?

“A good faith deposit happens much earlier (in the purchase process), often during the application for financing, and goes directly to a lender or broker, says Matt Vukovich, a real estate expert who handles property acquisitions daily “It covers upfront expenses like appraisals and legal fees to see if a loan is viable, rather than serving as skin in the game for the real estate.”

As mentioned, this deposit sits outside of the PSA and is vulnerable. The good news, however, is that earnest money works differently and is legally protected by the agreement.

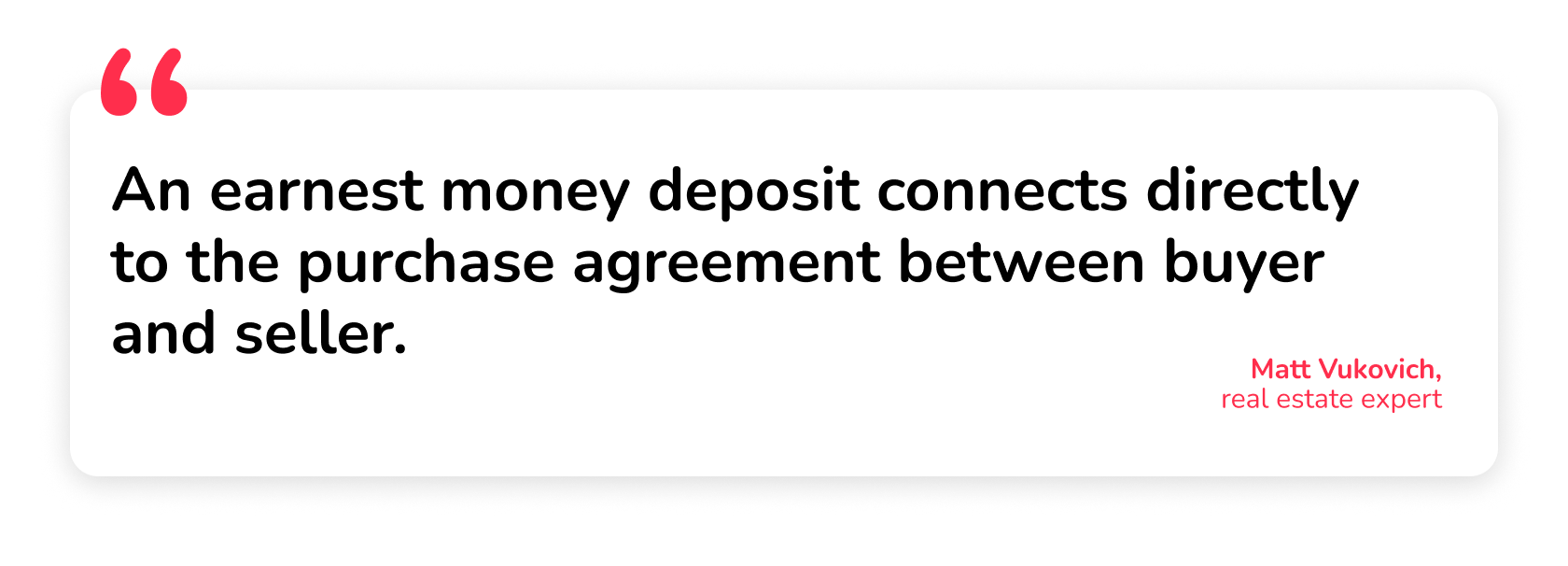

“An earnest money deposit connects directly to the purchase agreement between buyer and seller,” continues Matt. “It sits in a neutral escrow account to assure the seller that you will buy the property.

What’s more, an EMD is tied to your commercial real estate purchase. As the buyer, you send the money via wire transfer to a neutral escrow account held by a title company or attorney, and governed by the PSA.

If the deal goes through, the amount contributes to the purchase price at closing. If it doesn’t, you may be entitled to a refund, subject to certain conditions.

A good faith deposit in commercial real estate behaves entirely differently and comes with none of these PSA protections. If, as a borrower, you send it to a lender for an appraisal, its refund conditions have nothing to do with the terms of the agreement, and possibly nothing to do with any written contract at all.

Down payment vs. earnest money (and other terms people mix up)

Mixing up a good-faith deposit with earnest money deposits is common among investors because both are deposits that confirm a buyer’s intent.

There are also a few other similar-sounding payments that get tangled in, and they don’t all behave in the way you might expect.

- Down payment

The down payment makes up the equity you must provide at closing to cover the Loan-to-Value (LTV) shortfall. This is typically 20-35% of the property value in the commercial real estate market and is a much larger sum than earnest money, which is usually credited to your purchase price.

- Due diligence fee

The due diligence fee works similarly to earnest money in that it shows your commitment to a deal and you can lose it if the deal collapses, but there are important differences.

First, due diligence money goes straight to the seller, and they normally take the property off the market while you complete property checks. It does not sit in escrow and is generally non-refundable from the start, unlike earnest money, which you can get back under certain conditions.

Knowing the difference between due diligence and earnest money is an important distinction because both will cost you the deposit if you back out at the wrong moment, but only one is at risk from the start.

- Option fee

The option fee gives you the right to buy commercial real estate within a set window, not the obligation. People often conflate this with earnest money because you also pay it up front, and it lets you lock something into the deal.

With the option fee, you get the right to decide later, which can turn out to be a very good thing if something doesn’t stack up.

These are almost always non-refundable because you’re paying the seller to keep the property back for you while you make up your mind.

How much should a good faith deposit be?

A good faith deposit is much smaller than earnest money, which can be up to 10% in competitive markets.

In some markets, these GFD costs may be as little as $500, rising to a few thousand dollars in more expensive areas.

Whatever the amount, it’s always worth knowing your commercial property deposit obligations before you sign so that you don’t over-expose your cash.

How to fund your deposit without tying up your capital

There’s one thing that hopefully this article has made clear: a good faith deposit is money you commit to a deal to cover underwriting, appraisal, or legal work that’s underway. This is money that you shouldn’t expect to get back.

Yet the earnest money, the larger deposit in a CRE deal, is different. This ties up real capital and, if done correctly with a PSA, earnest money can be refundable.

If you’re buying $5 million commercial real estate with a 5% EMD requirement, then that’s $250,000 you’ll need to put in escrow for up to 90 days, at a risk of losing it should the PSA not not work out as planned.

“Putting up more capital than your contingencies protect is a real exposure,” says Emma Alves, real estate lawyer at Alves Law. And even when capital is protected, it's still capital you can't deploy on the next deal.

This is where EMD, or soft deposit, financing can have a dramatic effect. The best soft deposit providers for CRE in the USA fund the EMDs held in escrow, so you don’t need to dip into your own funds or provide collateral. You can also work on multiple deals at once as a result.

"Good faith deposit" and "earnest money deposit" might sound like two ways of saying the same thing. In a CRE deal, the difference can be six figures.

Ready to stop putting your own capital at risk for a deposit? Sign up for Duckfund and find out how we fund your next deal with no collateral, no delays, and no strings attached.

Good faith deposit FAQs

Is a good faith deposit refundable?

Most likely not. A good faith deposit is used to cover costs like appraisals and other work to be done right away, so is normally non-refundable.

An earnest money deposit, meanwhile, is put in an escrow account and can be refunded subject to certain conditions, known as contingencies.

How much should a good faith deposit be?

Earnest money in commercial real estate is often between one to five percent of the sale price, but can rise toward 10% in high-demand markets.

A good faith deposit to a lender is usually far smaller than this because it covers basic appraisal and report fees instead of securing the property.

Is a good faith deposit the same as earnest money?

The two types of deposit usually work the same way in the home buying process, but they tend to differ in commercial real estate transactions.

Earnest money is tied to the PSA and is held in an escrow account, while a good faith deposit may go to a lender or broker outside of the contract.

What is another term for a good faith deposit?

As a CRE investor, you may hear people use the terms “earnest money” and “soft deposit” when they mean the “good faith deposit”, yet these are not exact synonyms because it’s a different payment with different rules.

You may also hear “good faith money”, which is talking about the same payment for appraisals and underwriting.

Are good faith deposits legal in NYC?

Yes. Both good faith and earnest money deposits are fully legal and common practice in New York, including New York City.

The NYC market is a particularly competitive one, however, so it’s worth going through your purchase agreement with a fine tooth comb to make sure you’re fully aware of the refund rules for any type of deposit.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence