Good Faith Deposits in Real Estate: 8 Tips to Close Your Deal Faster

Good faith deposits are now a standard part of commercial real estate transactions, but beneath their simplicity lie complex rules, regional variations, and legal risks every CRE investor must understand.

Good faith deposit in real estate is here to stay. Sellers love it because it helps identify serious buyers who are truly interested in closing the deal. Buyers have also come to appreciate it as a way to gain a competitive advantage for desirable properties in prime locations.

Yet, certain complexities remain regarding how good faith deposits (also known as earnest money deposits) work in the US real estate market:

- Why are there diverse requirements for good faith deposits in different parts of the country?

- Is a good faith deposit refundable? If so, under what conditions?

- What roles do escrow agents play, and how do they navigate issues around refundability?

- What impacts do state regulations have on good faith deposits in real estate?

- How do you raise good faith deposits when you are currently illiquid?

These and many more questions continue to trouble commercial real estate (CRE) investors. Lack of clarity regarding them has led to legal issues for some and has thrown the plans of others off kilter.

In what follows, we seek to address eight complexities and the challenges they pose for CRE investors in the US. We will also provide tips that will help you gain mastery of good faith deposit in real estate so it can become a support rather than a hindrance to your investing goals.

Are you ready to gain a competitive advantage over other CRE investors? Contact us at Duckfund to learn more about how our good faith deposit financing can help you close more CRE deals.

1. Understanding how good faith deposit requirements differ across the US

It’s no news that some real estate markets are more desirable than others for various reasons (economic, security, diversity, lifestyle, etc). This difference in desirability results in varying levels of demand.

It’s not surprising, then, that in prime locations, where demand is high, good faith deposit requirements will be higher.

Thus, while a good faith deposit requirement typically ranges from 1-5% of the property’s price across the US, it is not unusual to find sellers in some prime locations requesting 10%.

So, how much is earnest money for commercial property in the US?

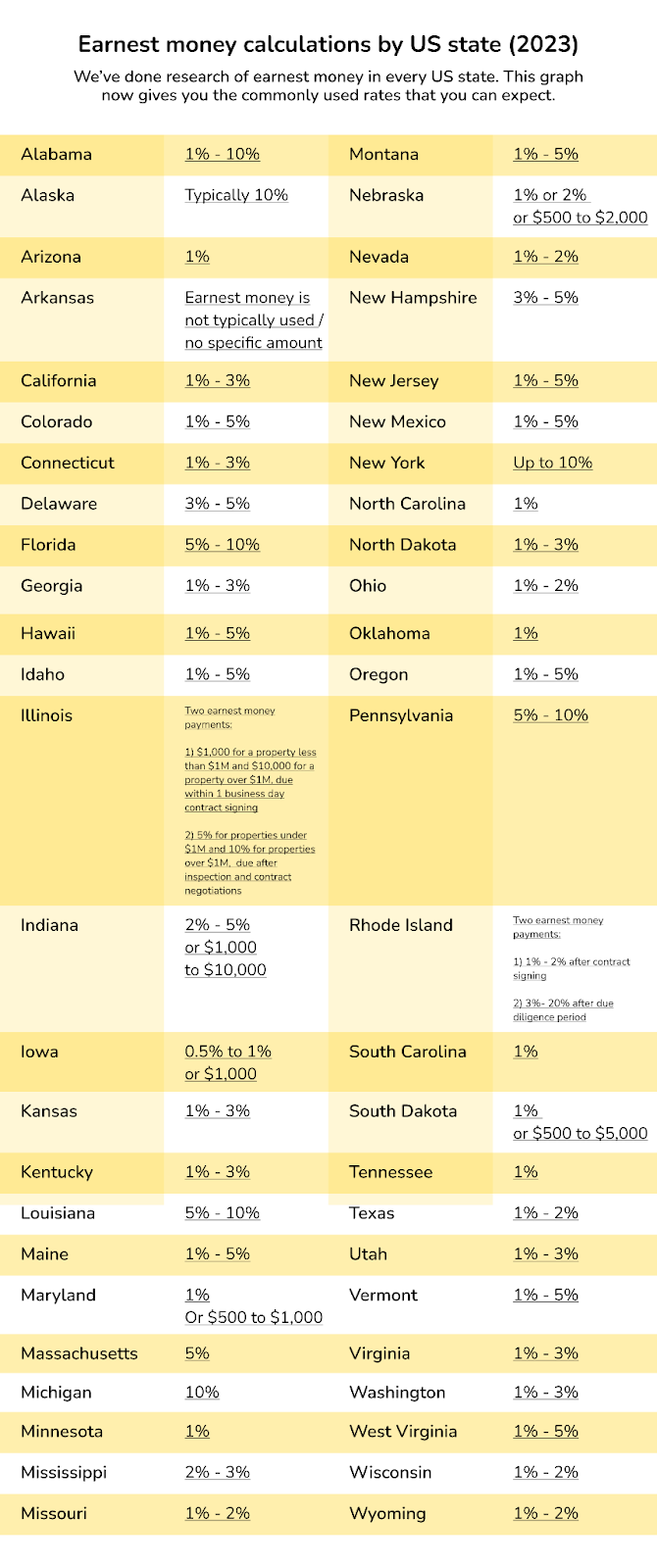

Our nationwide study reveals that the following are the average requirements for good faith deposit in commercial real estate across the US:

- 0.5%-1%: Iowa

- 1%: Arizona, Oklahoma, North Carolina, South Carolina, Tennessee, Maryland, Minnesota, and South Dakota

- 1%-2%: Nevada, Missouri, Nebraska, Texas, Ohio, Rhode Island, Wisconsin, and Wyoming

- 1%-3%: North Dakota, California, Connecticut, Utah, Georgia, Virginia, Washington, Kansas, and Kentucky

- 1%-5%: Hawaii, Maine, Montana, Oregon, Colorado, Vermont, New Jersey, West Virginia, New Mexico, and Idaho

- 1%-10%: Alabama

- 2%-3%: Mississippi

- 2%-5%: Indiana

- 3%-5%: Delaware, New Hampshire

- 5%: Massachusetts

- 5%-10%: Louisiana, Pennsylvania, Illinois, and Florida

- 10%: Michigan, New York, Alaska

It should be noted, though, that these are average figures. For example, a Class A property in California may have a 10% good faith deposit requirement, while the seller of a Class C property in Florida is requesting 3%.

Similarly, while you may pay less in a buyer’s market, you will typically pay more in a seller’s market.

Tip for success

Knowing the average good faith deposit requirement in a state will help you plan when you are interested in a property in such a state. You can quickly estimate how much cash the seller will likely require by multiplying the purchase price (sales price) by the average requirement.

Though the actual requirement for a given property may be higher or lower than the average, at least you are not approaching the seller clueless.

2. Is a good faith deposit refundable?

Are earnest money deposits refundable?

This is one of the most popular questions regarding the operation of good faith deposits.

There are times when the deal does not go through even after the payment of a good faith deposit. What happens in those situations?

First, it depends on who is cancelling the deal – the buyer or the seller.

When it is the seller, things are simpler. In that case, the good faith deposit is refundable.

Second, it depends on why the buyer is cancelling the deal.

If the deal falls through for reasons already included as contingencies in the purchase contract, the good faith deposit is also refundable.

What then are these contingencies? There are four common ones:

- Inspection contingency (also known as home inspection contingency in residential real estate): If the inspection of the property reveals significant faults, the buyer can choose to back out of the deal.

- Financing contingency: The buyer can opt out of the deal if they cannot secure the funding to pay for the property.

- Appraisal contingency: This allows the buyer to back out of the deal if their appraisal reveals that the house is not as valuable as the market price suggests.

- Home sale contingency: Though the name comes from the world of residential real estate, it also applies in the CRE market. If the buyer’s purchase of the property depends on the sale of another one, they can opt out of the deal if the sale does not succeed.

However, good faith deposits will be non refundable if the buyer backs out of the deal for any reason not previously agreed upon as a contingency, fails to meet the terms and conditions of the deal, or backs out of the deal after waiving the contingencies.

“It’s also unlikely for a buyer to get their earnest money back if they fail to meet the terms and conditions of their purchase contract,” according to Zillow, an online real estate marketplace. “Common breaches of contract are failure to meet payment deadlines, delaying important paperwork, and backing out of a deal without a valid contingency.”

A waiver of contingency can make a buyer more appealing to a seller. A buyer who has gotten a mortgage preapproval, for example, may not need a financing contingency, and some sellers will consider that an advantage.

But the downside is that the good faith deposit will not be refundable if you back out of the deal for any reason. For example, if a mortgage application falls through after a preapproval (which does happen), you will lose your earnest deposit if you didn’t include a financing contingency.

Tip for success

If the possibility of getting a good faith deposit refund is important to you, avoid waiving contingencies.

These contingencies are meant to protect you from a deal that turns out to be undesirable without losing your earnest deposit.

Also, ensure that all relevant contingencies are included in the purchase and sale agreement. Assume nothing, verify everything.

3. Understanding the roles of escrow agents

All the talk about sellers setting good faith deposit requirements may imply that they are the ones who receive the money. But that is not so!

Potential buyers typically transfer the good faith deposit to an escrow agent who holds the money on behalf of the seller and the buyer. Escrow agents include:

- Escrow companies: These are companies that specialize in acting as escrows for a variety of transactions.

- Title companies: In addition to verifying a property’s title, these companies can also act as escrow for real estate transactions.

- Real estate agent or brokerage: Some real estate brokerages include escrow services as part of their offerings. Individual real estate agents can also execute this role.

- Banks: It is not uncommon for banks and other financial institutions to act as escrows for certain transactions.

- Attorneys: Real estate attorneys can also play the role of an escrow agent.

What do escrow agents do with the money?

It depends on whether the deal succeeds or not.

If the deal does not succeed, they simply act based on the terms of the purchase agreement (also known as the sales contract).

As said above, the buyer is entitled to an earnest money refund if they back out due to contingencies included in the agreement (or if the seller is the one opting out). In that case, the escrow will issue a refund to the buyer.

However, if the buyer is not entitled to a refund (because of the three reasons highlighted above), the escrow will send the money to the seller.

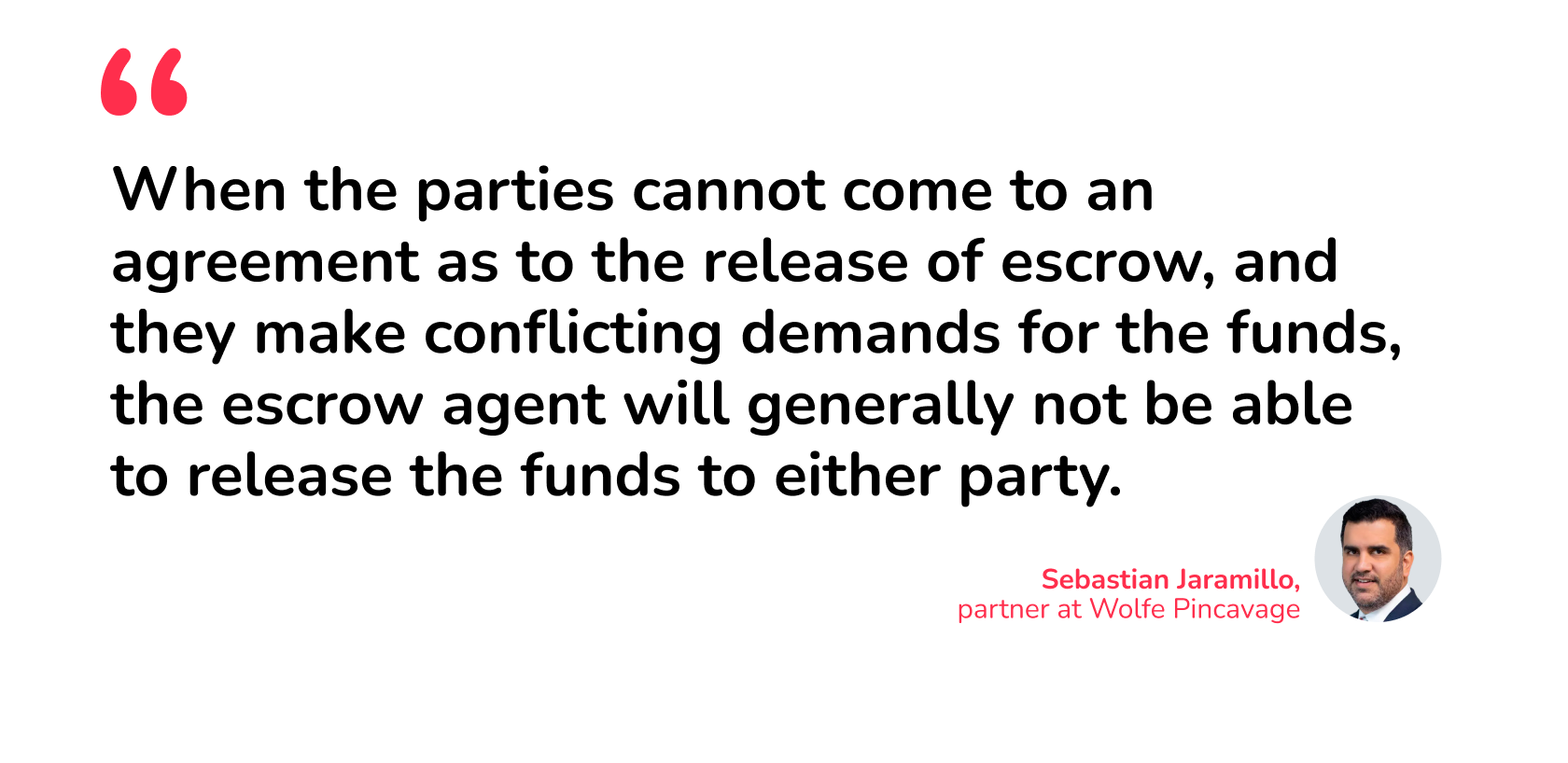

Unfortunately, both parties must sign before the escrow can release funds to whoever has a legitimate claim on the deposit. Why is this unfortunate? Well, there are times when there is a dispute with both buyers and sellers laying claims to the good faith deposit.

“When the parties cannot come to an agreement as to the release of escrow, and they make conflicting demands for the funds, the escrow agent will generally not be able to release the funds to either party,” according to Sebastian Jaramillo, a partner at Wolfe Pincavage, a law firm. “An escrow agent (or broker) shouldn’t release funds unless both parties sign a release.”

In some cases, both parties can resolve the issue through mediation and arbitration. However, if that fails, the escrow agent will file an interpleader action to remove itself from the dispute. The funds will then be deposited in the court’s registry.

Tip for success

Again, the purchase agreement is key. Ensure that it outlines what will happen to the good faith deposits when the deal does not succeed. Clarity in this regard will make a court case less likely and help you present solid arguments if it ever gets to that stage.

4. The various uses of good faith deposits

When the deal succeeds, there are two broad uses of good faith deposit in commercial real estate:

- Part of the down payment: If you are relying on mortgage financing, the good faith deposit can be added to the down payment required by the lender.

Some buyers even use it to offer a higher down payment (upfront payment) to the mortgage lender so they can lock in lower interest rates.

Depending on the terms of the purchase agreement, the escrow can send the money to you or directly to the lender.

- Settling closing costs: Alternatively, good faith deposits can be deployed to cover closing costs, thus reducing the amount the buyer must pay at the time of closing.

-

Tip for success

If you have a preference for how the earnest money should be used, you should include it in the purchase agreement.

5. How buyers are gaining a competitive advantage with good faith deposits

Many buyers initially considered good faith deposits an inconvenience, but that attitude is changing.

In competitive markets, the ability to offer a higher good faith deposit than what is required can make a buyer’s offer stand out.

There are three ways to use higher good faith deposits as a negotiation tool, according to Ramit Sethi, a personal finance coach and best-selling author:

- Compensate for other weaknesses of your offer: If you are not waiving contingencies or you need a longer closing timeline, the seller may place you lower in the pecking order. In that case, a higher good faith deposit can bring you further up.

- Negotiate a lower purchase price: Since good faith deposits demonstrate seriousness, a higher offer can make the seller consider you more serious than others. This can open the door to negotiating a slightly lower purchase price.

- Standout offer when there are multiple offers: When the field becomes competitive, a higher good faith deposit can help you stay above the pack.

Tip for success

Willingness to offer a higher good faith deposit can help you stand out. However, know when you should use this negotiation tool. If there is no competition, then there is no point holding up more cash.

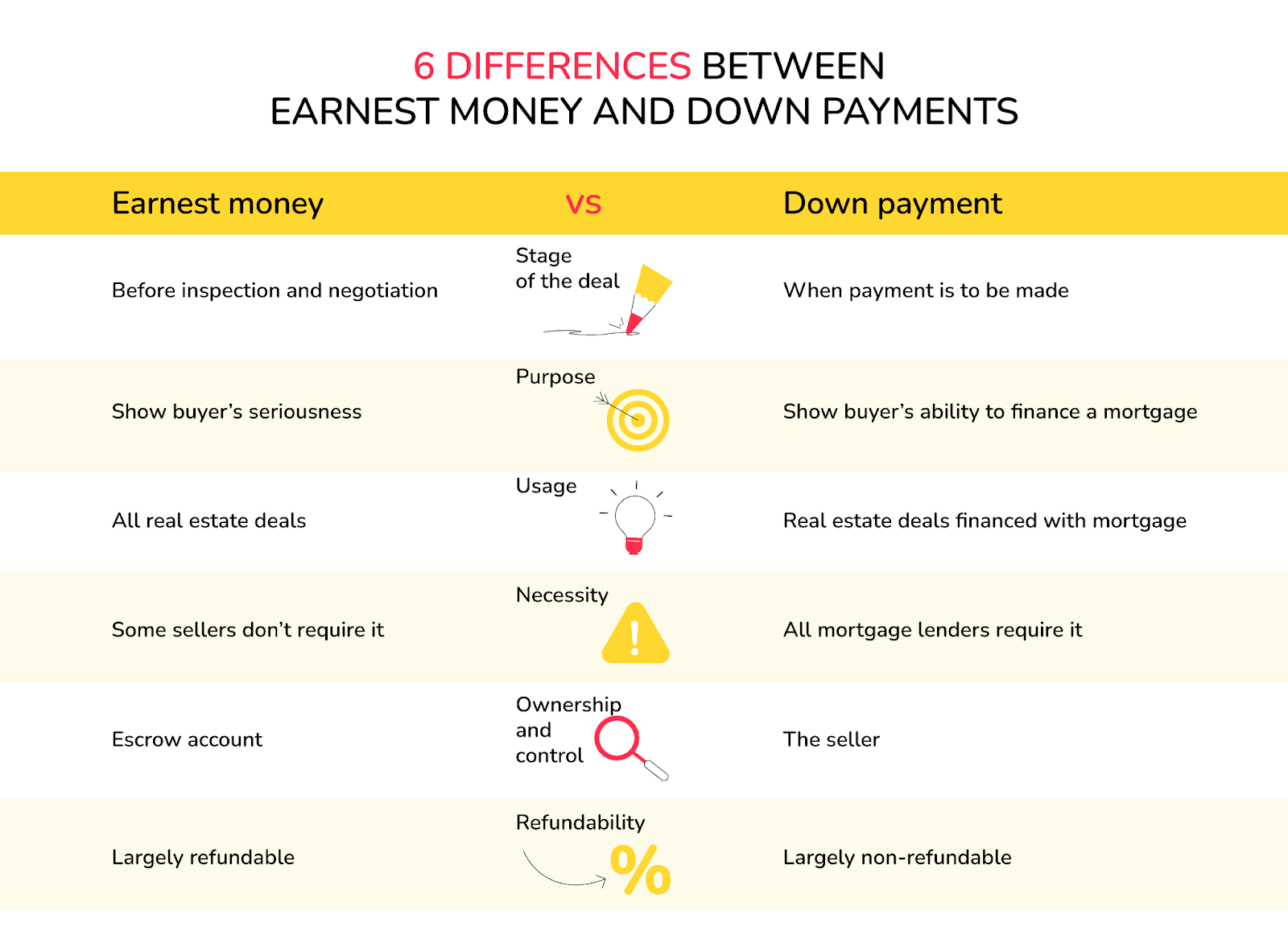

6. How good faith deposits differ from down payments and due diligence fees

What is a good faith deposit in real estate?

It may seem that the answer to this question is obvious, but some still confuse good faith deposits (also known as earnest money deposits and compared to security deposits by some) with other things like down payments and due diligence fees.

Good faith deposits vs down payments

A good faith deposit is a portion of the purchase price that the seller demands to show that a buyer is serious about the potential purchase of the property.

On the other hand, a down payment is a sum of money demanded by mortgage lenders to verify the borrower’s ability to repay the mortgage loan.

Below are six differences between the two:

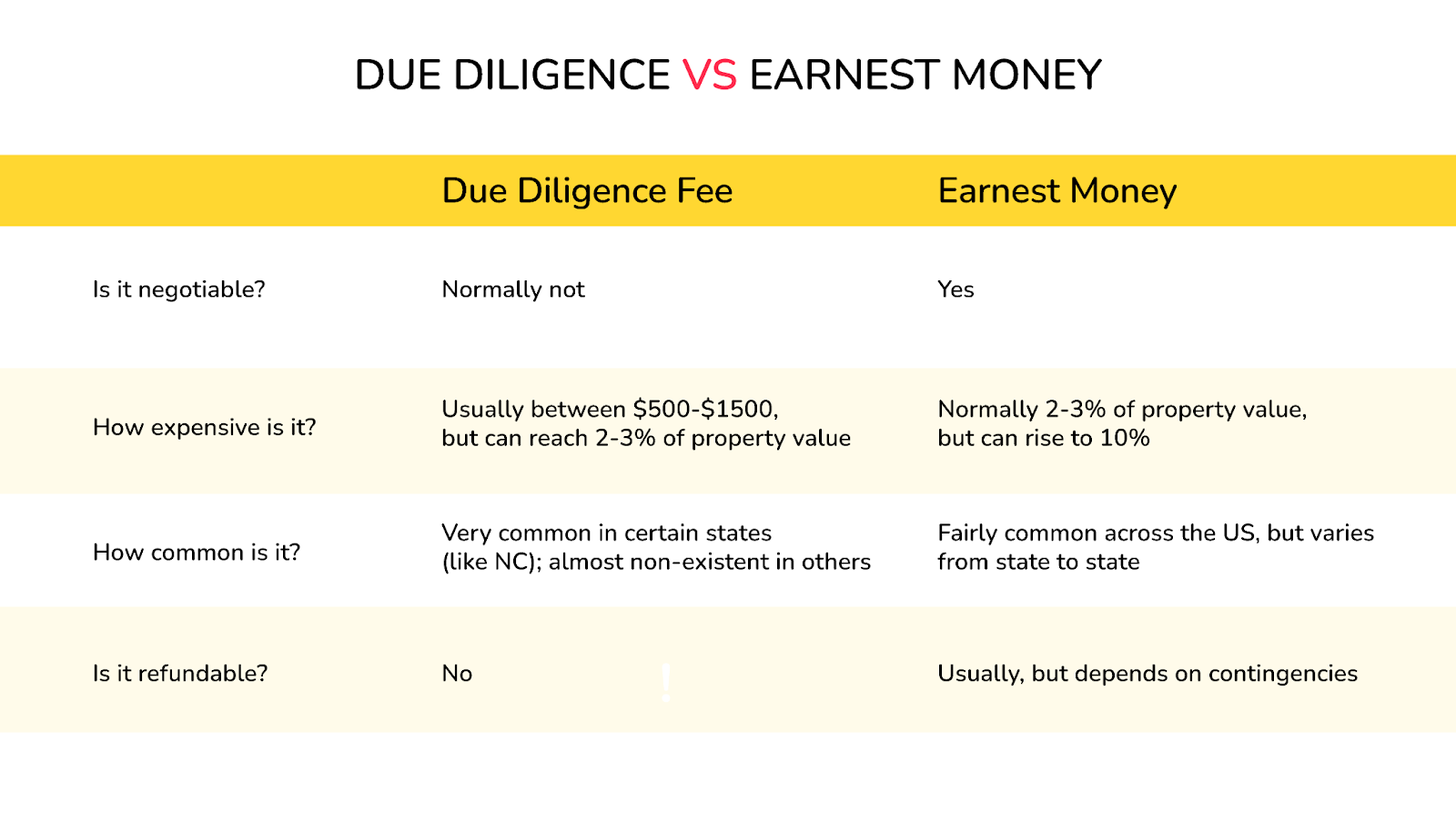

Good faith deposits vs due diligence fees

A due diligence fee is an amount paid by a buyer who is requesting more time to conduct due diligence on a property before closing the deal. The fee compensates the seller, who now has to take the property off the market and cope with a longer closing timeline.

Below are four key differences between due diligence and good faith deposits:

Tip for success

If a particular property is very important to you, consider paying the due diligence fees to close out other competitors while you conduct extensive due diligence on it.

However, don’t forget to include the inspection contingency in the purchase agreement so that you don’t lose both the due diligence fees and the good faith deposit if you choose to pull back from the deal.

7. The impacts of state regulations on how good faith deposits work

We mentioned at the beginning that good faith deposit requirements differ across US states.

In addition, states have varying norms that affect how earnest money works.

In places like Nebraska, Maryland, and North Dakota, you can pay a fixed amount ($500-$2,000; $500-$1,000; and $500-$5,000, respectively) instead of a percentage of the purchase price.

Also, you can pay the deposit twice in places like Rhode Island and Illinois. The first payment happens after the contract signing, while the second one is after the due diligence period.

There is also a variation in the mode of payment. For example, escrow agents in Colorado won’t accept cash, limiting payment methods to cashier’s checks, certified checks, personal checks, and wire transfers.

Furthermore, in California, the amount that can be awarded to the seller when the deal does not go through is limited to 3% of the purchase price, which is why good faith deposits in the state don’t usually exceed that amount.

Sethi also mentioned that California requires that good faith deposits be held by a neutral third party, while in New York, they are typically held by the seller’s attorney. Also, in Texas, the deposit is expected to be deposited no later than the third business day after offer acceptance.

The following surveys provide you with more information about the norms in some of the popular US states:

- Good faith deposit in NYC

- Good faith deposit in Michigan

- Good faith deposit in Texas

- Good faith deposit in Illinois

- Good faith deposit in Florida

- Good faith deposit in Colorado

- Good faith deposit in South Carolina

Tip for success

A good grasp of the norms that operate in a state (beyond average requirements) will aid your preparation and provide a competitive advantage.

8. Raising good faith deposit when you are illiquid

Perhaps the greatest challenge for CRE investors is consistently raising good faith deposits for all the deals that excite them.

Since it’s almost impossible to always have the necessary cash to pay, CRE investors must know how to secure good faith deposit financing so they are not left out of good deals due to temporary illiquidity.

But it is not enough to get access to the needed funds; speed is also a priority, especially for competitive properties. “After your offer is accepted, you'll need to submit earnest money within a specific timeframe, typically 1-3 business days,” said Sethi.

Given what we have said about using good faith deposits as a negotiation tool, it is also crucial to find a financing platform that can support depositing a higher amount than what is required by the seller.

Tip for success

Using a good faith deposit financing company like Duckfund can help you build a profitable CRE portfolio.

With Duckfund, you can complete an application for a good faith deposit in just 2 minutes and have the money sent to the escrow account within 48 hours, all without submitting a credit report.

Duckfund also allows you to pay a higher good faith deposit than what the seller requires to boost your chances of getting the deal done.

Furthermore, you can receive good faith deposit funding for multiple deals at the same time, allowing you to pursue as many deals as you desire.

Are you ready to build a profitable CRE portfolio? Don’t let good faith deposit stop you! Sign up with Duckfund for quick and convenient access to good faith deposits funding for all your deals.

Takeaways

- Good faith deposit requirements and norms differ across US states. A knowledge of the uniqueness of each state will help home buyers and CRE investors plan.

- A buyer can typically recover their deposit if they back out for reasons protected by contingencies in the contract (e.g., inspection, financing, appraisal). Without these, or if deadlines are missed, the deposit may be forfeited.

- Deposits are held by third-party escrow agents—not sellers—who disburse funds according to the purchase agreement. Disputes can delay or complicate the release, sometimes requiring mediation or court intervention.

- For investors facing liquidity challenges, good faith deposit financing platforms can provide quick access to funds. This enables participation in more deals and offers the flexibility to make stronger offers in competitive markets.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence