Duckfund vs Traditional CRE Crowdfunding Platforms: Why They're Not the Same Thing

Researching commercial real estate financing tools, Duckfund will often show up alongside funding tools like CrowdStreet, Fundrise, and RealtyMogul. Does that mean these CRE financial options are the same?

If you're an accredited investor doing a quick search, you might assume these tools do roughly the same job. But when you’re an active deal sponsor trying to lock up a property, that assumption might just cost you the deal.

When you stop and compare Duckfund to traditional commercial real estate crowdfunding platforms directly, you’ll see that these funding tools are nothing alike. They don't serve the same buyer. Nor do they serve the same investment strategy.

Here's where most active CRE sponsors get stuck:

- Your capital is tied up and you need a deposit in escrow before competing bids surface and the seller moves on.

- You need a way to fund the deal yourself but keep landing on passive investment platforms built for people who want returns from someone else's deal.

- You're unsure how Duckfund compares to other funding tools: is it crowdfunded, a traditional real estate lender, or something else entirely?

This comparison article breaks down how Duckfund and crowdfunding platforms work, what each funding tool is built for, and where they belong in a deal's capital stack.

If you're an active sponsor looking to secure a commercial property rather than passively invest in real estate projects, Duckfund might be your best bet. Let’s compare Duckfund to traditional commercial real estate crowdfunding platforms and find out why that’s the case.

Looking for fast EMD financing to compete on your next CRE acquisition? Contact Duckfund to learn how soft deposit financing can help you capitalize on investment opportunities.

What is commercial real estate crowdfunding?

Real estate crowdfunding platforms are online investment vehicles that pool capital from individual investors into commercial property deals managed by a third-party sponsor. You put money in, receive a proportional equity stake or debt position, and wait for distributions over a hold period of what is typically five to ten years.

The deal itself is managed entirely by the sponsor. That hands-off structure means you have no say in operations, tenant decisions, or exit timing.

The crowdfunding model is clearly geared towards passive capital deployment, giving retail investors exposure to commercial real estate without the operational headache of owning or managing a property directly.

With this structure in mind, crowdfunding investment comes with real pros and cons:

Pros:

- Low barrier to entry: platforms like Fundrise have a minimum investment of $10, far less than the $50,000 or more typically required for private equity real estate deals

- Passive income potential: returns through quarterly distributions, with no tenant management, maintenance obligations, or lease renewals attached

- Diversification: across multiple commercial asset classes and geographies, without direct property ownership

Cons:

- Capital is illiquid: Most deals run five to ten years, and early exit options typically come with heavy penalties

- No deal control: the sponsor manages all decisions, from renovation scope to sale timing, with no input from individual investors

- Platform risk: CrowdStreet's CEO was sentenced to 87 months in prison after diverting $62.8 million of investor funds, according to reporting by The Playbook. Startups like RealtyShares and Crowdestate had to close or shut down operations.

Even with these downsides and potential risks, the appeal of passive income through fractional ownership is real.

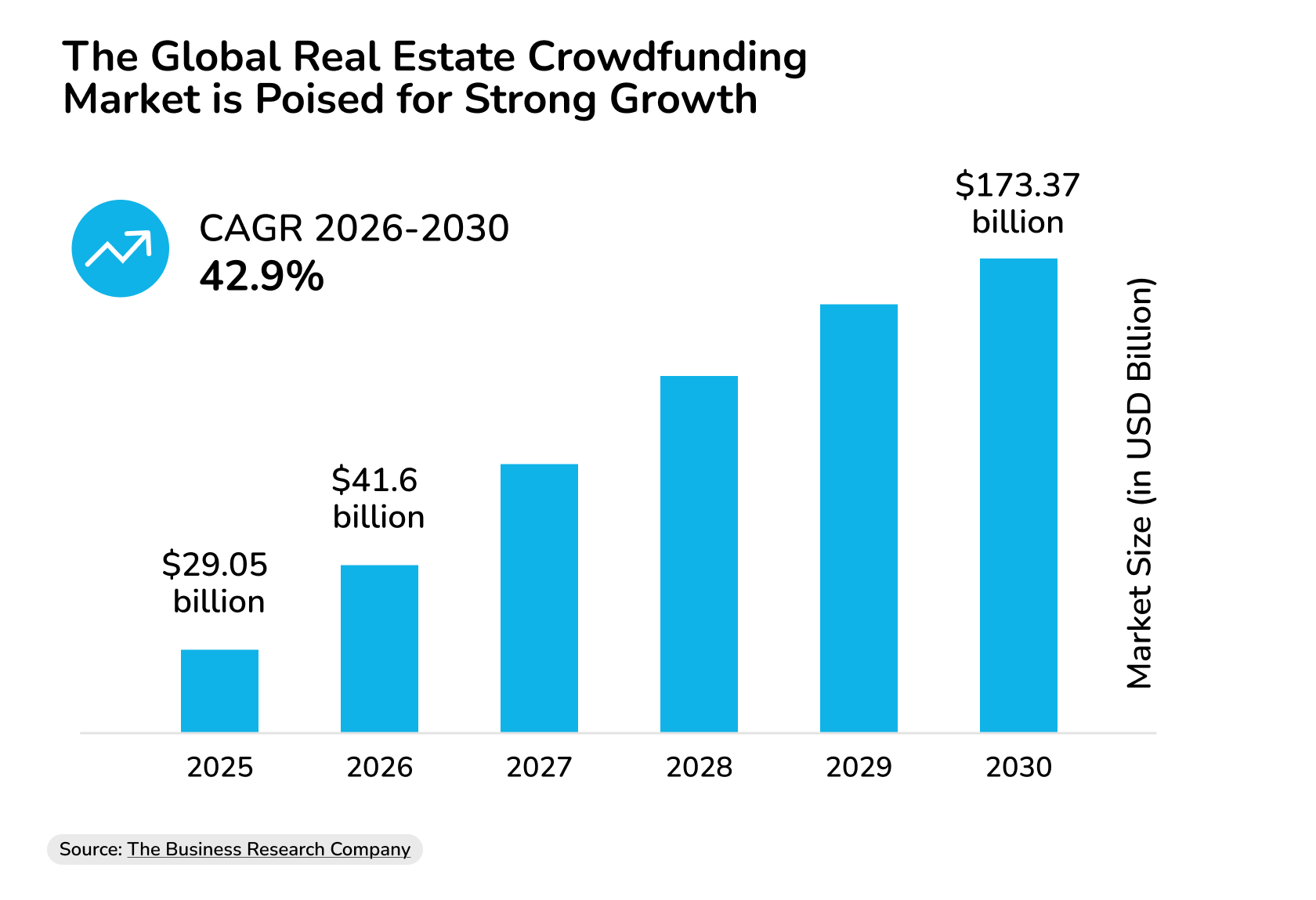

The real estate crowdfunding market size boomed from $20.31 billion in 2024 to $29 billion in just one year, according to analysts at The Business Research Company. The research company predicts the global real estate crowdfunding market to hit over $173 billion by 2030, growing 43% annually.

Source: The Business Research Company

What are the best real estate crowdfunding platforms?

Four platforms stand out in the US market, with each aimed at a different type of private real estate investor. Their minimum investments, fee structures, and target returns differ substantially.

- Fundrise is the most accessible entry point for retail capital. Non-accredited investors can start with $10, the total annual fee is 1% (split between a 0.85% asset management fee and a 0.15% advisory fee), and historical returns have ranged from 8% to 12%. Liquidity is limited to quarterly repurchase windows, and early exits carry penalties.

- CrowdStreet is built for accredited investors, with a $25,000 minimum per deal. Target returns run from 12% to 18%, hold periods span three to seven years, and investor-facing fees are zero – costs are covered by the deal sponsor. Liquidity before exit is effectively nonexistent.

- RealtyMogul sits between the two. Its REIT products start at $5,000 and are open to both accredited and non-accredited investors, with target returns between 6% and 12%. Private placement deals are reserved for accredited investors, and hold periods run from three to ten years, depending on the offering.

- EquityMultiple co-invests in every deal it lists. It’s the only platform among the four to do so. It also does rigorous due diligence: only about 5% of proposed investment options pass vetting. The investment minimum is $5,000, though equity investments require more. Annual fees run 0.5% to 1.5%, plus a 10% profit share on realized equity returns. Target returns range from around 7.4% annualized on short-term notes up to 14% to 20% on common equity.

Some crowdfunding sites might promise higher returns than others, yet all share one trait: you're allocating capital into a deal someone else controls.

For active CRE sponsors looking to raise capital for their own CRE acquisitions rather than invest in someone else's, Duckfund answers a different question. That distinction is what the rest of this article addresses.

What is Duckfund and how does it work?

Duckfund is another name that frequently pops up alongside alternative investment tools – but it addresses an entirely different problem than crowdfunding platforms. A problem that active CRE sponsors across all property types know all too well.

Let’s say you've found an interesting investment opportunity. It’s a multifamily asset of rental properties. Due diligence shows great potential annual returns and so you move. The seller accepts your LOI and asks for an earnest money deposit in escrow. Fast, because other buyers are already showing interest.

The problem? You’re illiquid because your capital is committed elsewhere.

That's where Duckfund comes in. Duckfund is a soft deposit financing provider built for active CRE sponsors who need to lock up a deal before their cash flow catches up.

Duckfund fills a specific gap in the acquisition timeline – the window between “accepted offer” and “capital in escrow” – that conventional lenders don’t cover. In this funding gap lies a timing problem, not a deal quality problem per se. And this timing problem only worsens as buying pressure grows in the CRE market.

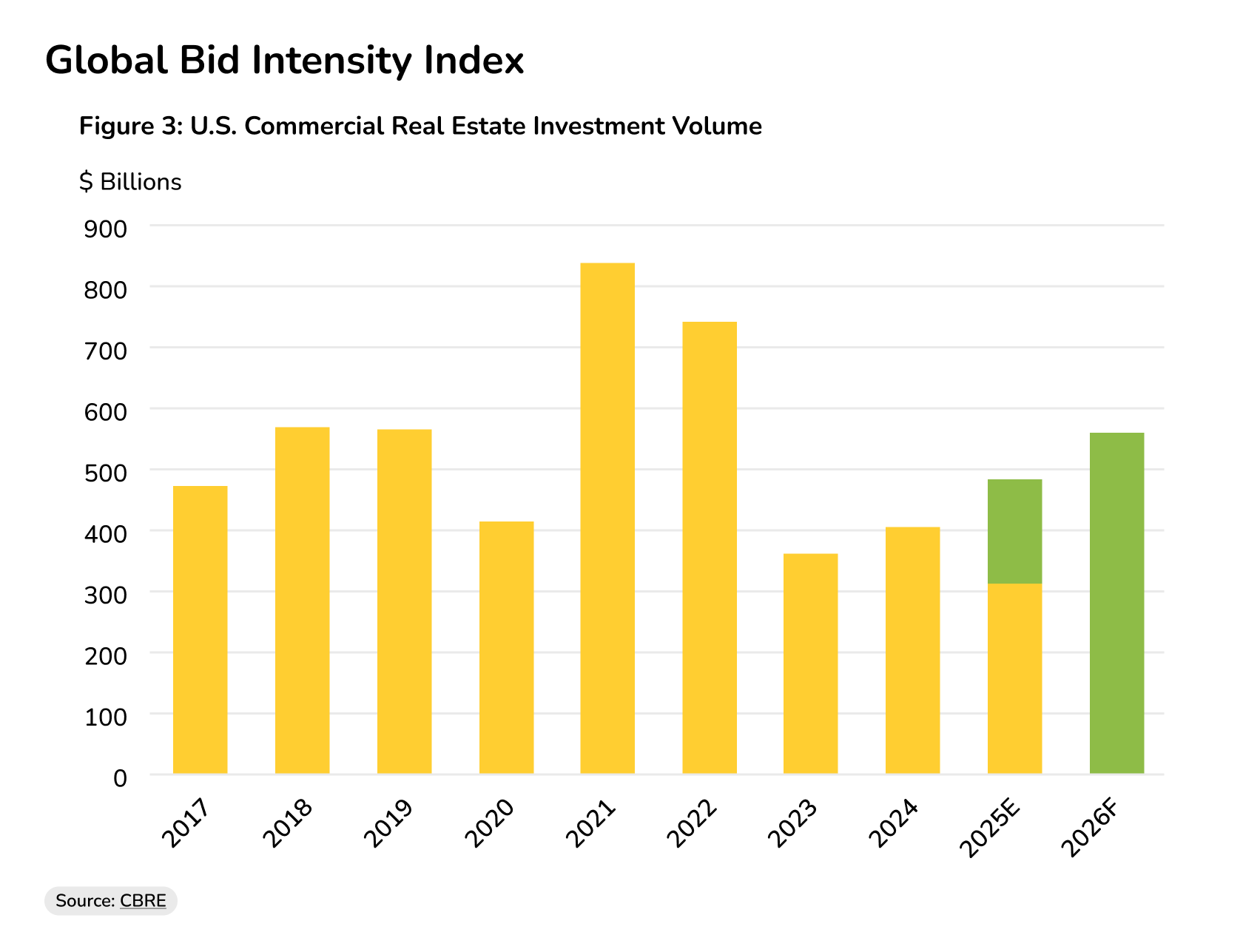

Commercial real estate investment activity is expected to grow 16% to $562 billion in 2026, according to CBRE's U.S. Real Estate Market Outlook. And more capital chasing deals means tighter competition.

The US CRE market is seeing growing investment activity since 2023

Source: CBRE

Research by Duckfund into EMD norms across the US found that the national average sits between 1% and 5% of the purchase price, with competitive or high-value assets regularly requiring 10% or even higher.

But it’s not just that earnest money deposits are getting bigger. Putting money down fast is equally important for investors. In competitive markets, the only way to stay in a deal like that is to have sufficient deposit capital ready as soon as the contract lands.

Brett Sherman, a tenant rep broker at Signature Realty who has spent 13 years structuring commercial acquisitions in Miami, has watched sponsors lose properties because their capital moved too slowly: “The deals that fall apart aren't usually bad deals. They're good deals with slow capital behind them.”

CRE sponsors need two things when chasing deals: enough liquidity and rapid deployment.

Duckfund's EMD funding works like this: sponsors apply in under two minutes, receive approval within one business day, and have funds in escrow within 48 hours. The minimum deposit starts at $25,000, no collateral is required, and the EMD stays fully refundable throughout the contractual due diligence period. The service covers all major CRE asset classes and is available across most US states.

The whole Duckfund model is built to help active sponsors tackle the question: can you get the deposit into escrow before the next buyer does?

Is Duckfund a crowdfunding platform?

The answer is no – and the structure of each tool explains why.

Duckfund is a direct EMD lender. The two categories might turn up in the same searches. But when we compare Duckfund to traditional commercial real estate crowdfunding platforms, they have very little in common.

Crowdfunding platforms aggregate capital from passive investors into property investments and real estate funds managed by a third-party sponsor. There's no single lender, no direct borrower relationship, and no urgency built into the model. The structure runs on weeks of investor screening, SEC compliance, and capital aggregation before a dollar moves.

Duckfund works differently. A single sponsor applies, gets approved within one business day, and receives deposit capital in 48 hours. No pool of investors. No equity stake given up. No hold period.

When you compare Duckfund to traditional commercial real estate crowdfunding platforms on structure alone, you're looking at two different financial instruments: one is an investment vehicle for passive investors seeking fractional real estate exposure; the other is a direct lending product for sponsors actively buying property right now.

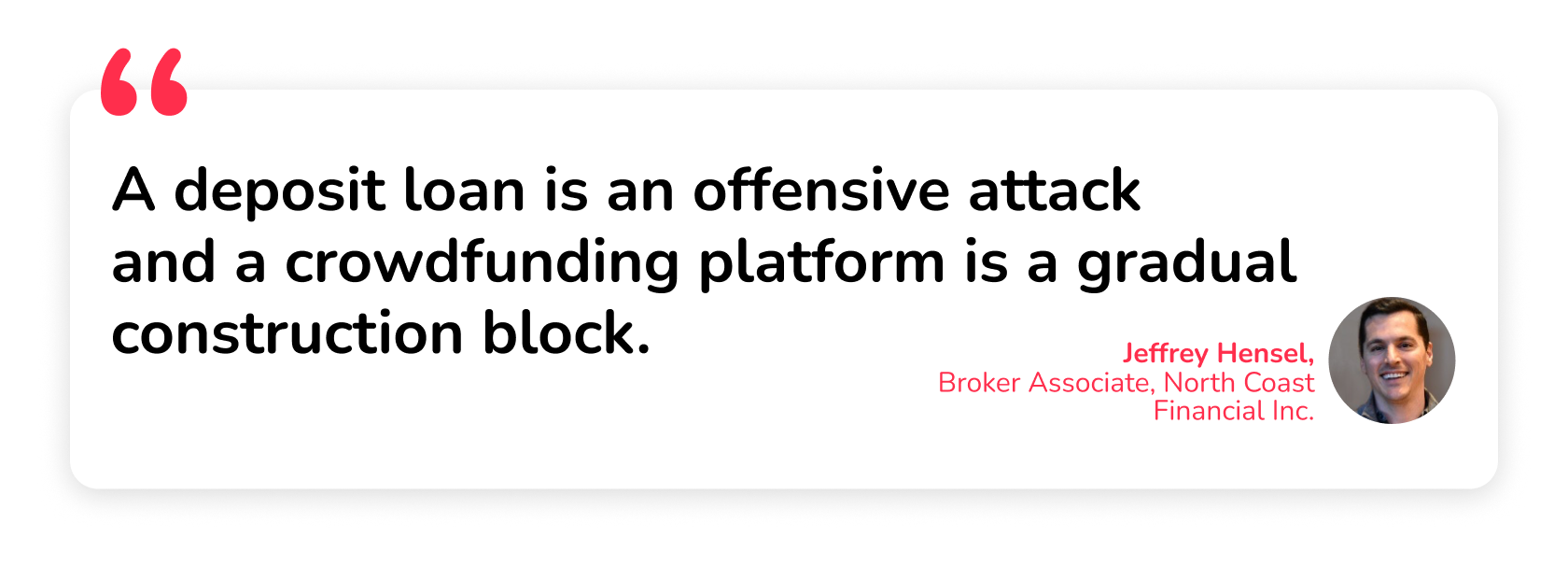

Jeffrey Hensel, a broker associate at North Coast Financial who has spent a decade in hard money lending, has watched this confusion delay and derail deals more than once: “The biggest bottleneck is not the amount of money conducted but the time when that money is conducted.”

Understanding this difference and using each tool effectively is what makes a great CRE professional. On the practical difference between the two, Hensel is direct: “The main best uses of crowdfunding platforms are the long-term passive equity deals in the already controlled deals. A deposit loan is an offensive attack and a retail crowdfunding platform is a gradual construction block.”

That timing gap is the core distinction. Crowdfunding platforms take weeks to deploy capital, while Duckfund takes days. And where crowdfunding chases passive returns, Duckfund places active investors at the deal table before anyone else.

Duckfund sits within a small category of specialist earnest money deposit financing providers built to operate specifically in that gap — and it's the only one structured as a fully digital, collateral-free product available across most US states.

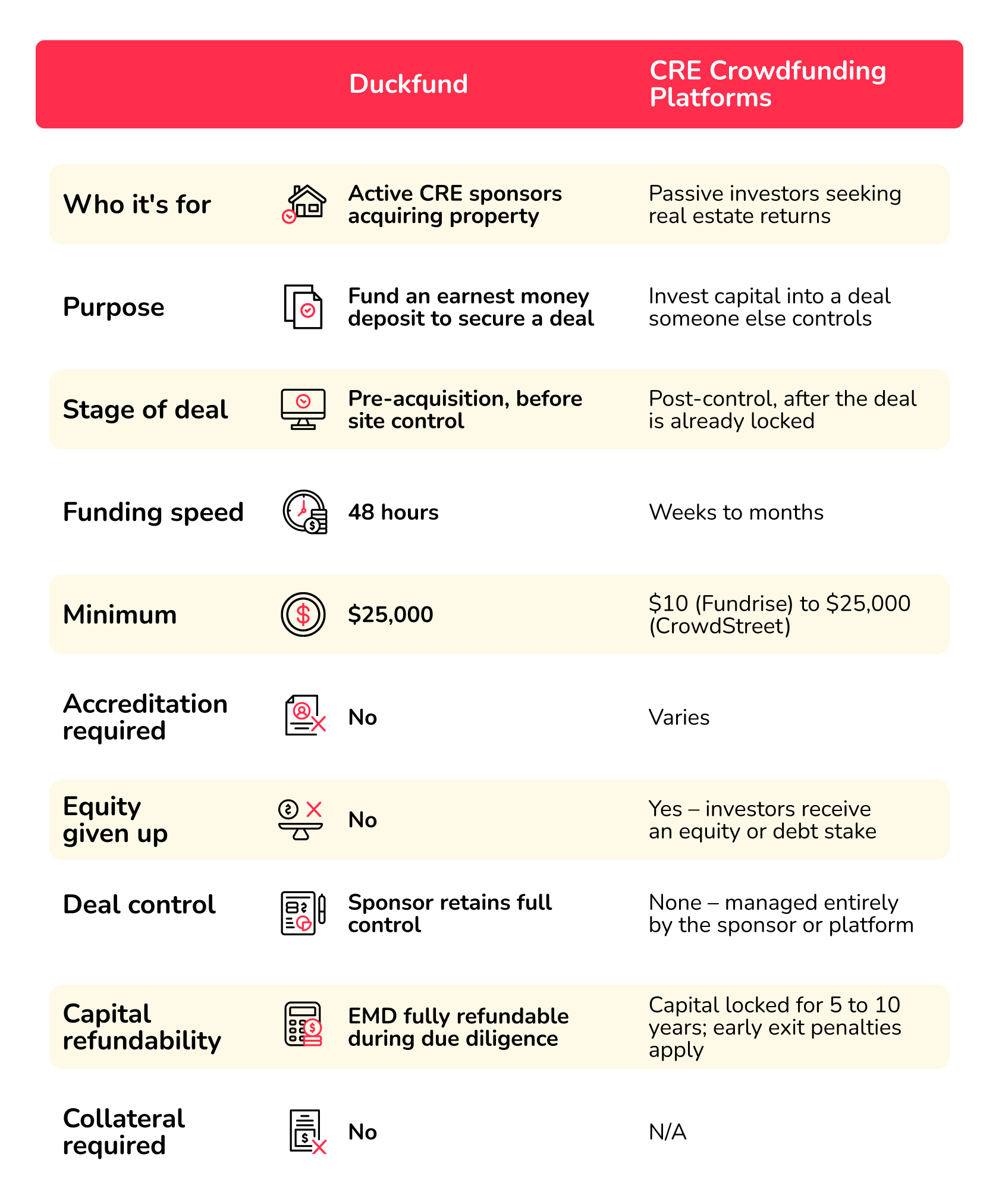

Duckfund vs. CRE crowdfunding platforms: A direct comparison

Putting the two side by side makes the difference hard to miss. Tenant rep broker Brett Sherman comments that "Conflating the two is like using construction financing to win a bidding war."

The wrong tool, at the wrong stage of the deal.

Here's what the comparison looks like when you compare Duckfund to traditional commercial real estate crowdfunding platforms across the dimensions that matter to an active sponsor:

Duckfund vs CRE Crowdfunding Platforms

What the table makes clear is that Duckfund doesn't replace crowdfunding, or the other way around. The tools don't compete.

For a hands-on sponsor who needs to lock up a property this week, crowdfunding platforms are simply not a solution. The timelines are structurally incompatible. Similarly, Duckfund’s product doesn’t serve a passive investor looking to deploy capital into a managed CRE deal over a five-year horizon.

EMD lending and crowdfunding serve different roles. In some deals, they can even serve the same sponsor at different stages — which is what the next section covers.

Where each tool sits in your capital stack

Every individual property acquisition follows a sequence. The capital tools you use should match where you are in it.

Before site control, the job is to win the deal — get the deposit in escrow, lock up the asset, and keep competing buyers out. Duckfund's EMD lending belongs in the first stage. The moment a seller accepts your LOI and asks for a deposit, speed and liquidity are the only variables that matter. Duckfund handles both.

Crowdfunding platforms with their slow capital aggregation and compliance process have no part to play at this stage.

Once site control is established, the job of capital shifts. Now you're capitalizing a deal you already have: assembling equity, bringing in investors, executing the business plan. That’s where crowdfunding could come in.

Brett Sherman, the Miami-based broker whose deal experience shaped several points in this article, explains the sequential relationship: “EMD financing is about not losing the deal. Crowdfunding is about capitalizing the deal you already have.”

An active sponsor who understands the capital stack can use both tools efficiently. In deals where the equity structure calls for it, EMD financing secures the asset first, and a crowdfunding platform brings the investors in second.

Neither tool is objectively better. Instead, they belong at different points on the same timeline.

Frequently Asked Questions (FAQs)

Can you use Duckfund and a crowdfunding platform on the same deal?

Yes, at different stages. Duckfund secures the asset pre-acquisition by funding the earnest money deposit. Once site control is established, a crowdfunding platform can be used to raise equity from investors. The two tools work sequentially, not in competition.

Does Duckfund offer returns or distributions like a crowdfunding platform?

No. Duckfund is a short-term lender, not an investment vehicle. Sponsors repay the deposit financing once the deal closes or the due diligence period ends. There are no investor distributions, equity stakes, or passive income structures involved.

Is CRE crowdfunding different from real estate syndications?

Syndications are structured for institutional investors or high-net-worth individuals and are built around a sponsor's track record. Crowdfunding platforms are regulated differently, reach a broader investor base, and commonly offer both equity positions and fixed-income debt investments.

Can I invest in real estate crowdfunding through a self-directed IRA?

Some platforms allow it. Eligibility depends on the platform and deal structure. Interest rates on debt products vary by offering, and specific net worth or income thresholds apply to certain deal types.

Is there a secondary market for crowdfunding investments?

Limited secondary market options exist on select platforms, but liquidity is far more restricted than publicly traded REITs. Most capital stays committed for the full hold period.

Find the right CRE financing tool for the right stage

The objective behind this article was a practical one: to compare Duckfund to traditional commercial real estate crowdfunding platforms, and to find out which one actually fits your case.

Which tool to use depends on where you are in the deal.

Passive investors seeking fractional exposure to managed commercial real estate have four solid platform options and a growing crowdfunding market behind them. Active sponsors trying to win a competitive acquisition before the next bid surfaces face a different problem altogether. Crowdfunding platforms aren't built to solve it.

When you compare Duckfund to traditional commercial real estate crowdfunding platforms on timing, structure, and purpose, they're solving different problems for completely different buyers.

Duckfund belongs before site control. Crowdfunding comes in after.

If your next deal is already in motion, apply for EMD financing with Duckfund and get your deposit with 48-hour approval, zero upfront capital, and discounted rates starting month four.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence