Is Earnest Money Refundable? The Refund Is in the Contract, Not the Law

Is earnest money refundable? Most investors are looking for the answer in the wrong place.

If you’re one of them, you may feel that your earnest money deposit (EMD) is vulnerable thanks to:

- A drawn-out underwriting process from your lender that’s taking longer than expected

- Due diligence lapsing past the deadline by a few days

- A contract going hard quicker than you expected, locking in your EMD with no clear exit.

These scenarios are enough to make you question whether you’ll see your earnest money deposit again, yet whether you do comes down to how you word your purchase agreement (PSA), rather than any state law or market norm.

In this guide, we explore how CRE earnest money really works in line with your PSA and how you can structure your deals so that you’re not risking this capital unnecessarily.

We’ll cover:

- Is earnest money refundable in commercial real estate? What it is, and how to get it back

- How to understand your purchase agreement (and protect your EMD)

- Do you lose earnest money if you back out? (4 common scenarios)

- When do you get earnest money back?

- How to protect your earnest money in CRE deals

- How to close a deal without risking your own capital

Is earnest money refundable? With Duckfund, it doesn’t matter. Contact us to find out how we fund your EMD, protect your capital, and keep you free to walk away – or scale up.

Is earnest money refundable in commercial real estate? What it is, and how to get it back

An earnest money deposit (EMD) is a down payment that a buyer makes to show a seller that they are committed to buying a property.

Here’s how it works in a commercial real estate deal:

- You put down your earnest money deposit up front as a signal of serious intent

- It goes into an escrow account, typically held by a title company or real estate attorney

- If the deal is a success, the EMD is taken from your closing costs

- If the deal falls through, the purchase agreement decides who keeps the deposit.

Earnest money deposits are calculated based on the purchase price. In a normal CRE market, you can expect to pay between one and five percent of the purchase price; however, sellers in competitive markets might ask for up to 10%

How commercial earnest money deposits differ from residential real estate

Higher property values mean that earnest money in the commercial real estate market typically far surpasses residential deposits, and even reaches six figures. Investors often take out gap funding at this stage as a way to bridge the difference.

On top of finding this money, you must also prepare for longer due diligence and underwriting timelines as a commercial investor, not to mention less protection from state laws.

Many CRE investors, especially those who leap from residential real estate, are not prepared for how exposed their EMD can become. The purchase agreement is often drafted with the seller’s interests in mind, which means that the guardrails that residential buyers enjoy simply don’t exist.

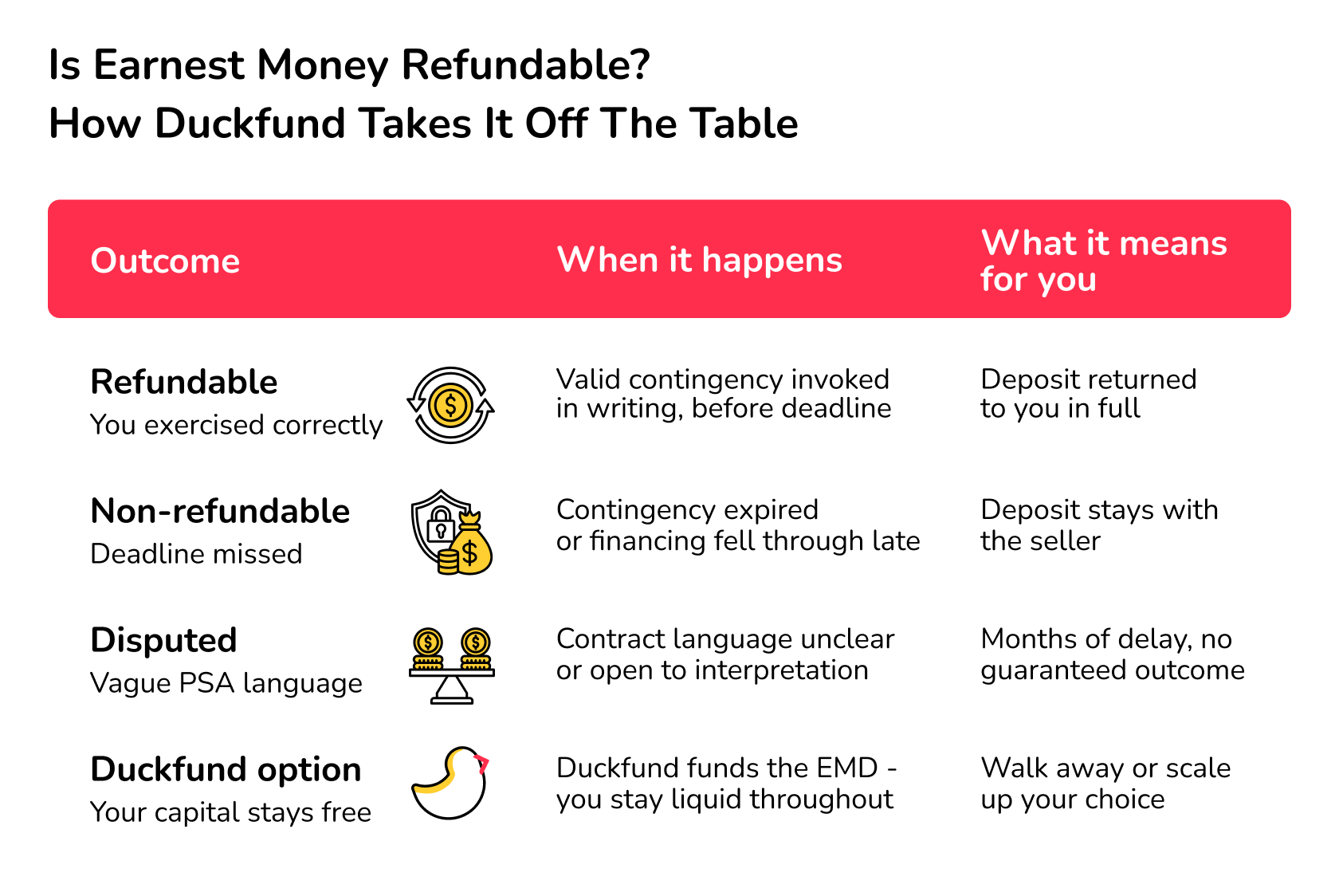

Is earnest money refundable in CRE?

Many investors walk into the trap of thinking their EMD is automatically refundable, when it isn’t.

When you place your earnest deposit, it’s typically “soft”, meaning it comes with a safety net of contingencies. These protect your money should things go wrong – but only for so long.

Each contingency has a deadline, and each one you miss snaps a thread of that safety net.

You might see an inspection fail, or a due diligence finding that changes the picture entirely, and this,

Miss enough of them, or miss the wrong one, and the net is gone entirely. Your EMD becomes non-refundable, or “goes hard”, and is very likely due to the seller.

Key takeaway: An earnest money deposit refund is a condition, not a guarantee. This condition is dependent on what’s in the purchase agreement.

How to understand your purchase agreement (and protect your EMD)

The best way to get a straight answer to “Is earnest money refundable?” is to look at your purchase agreement. This will give you more clues than the market will.

Here are the key things to look out for.

1. Contingencies (your primary protection)

The best safety net you can make for yourself is to structure your contingencies carefully – these are the only things protecting you from a non-refundable deposit.

A financing contingency is the safeguard against your mortgage loan falling through, but only within a specific window. In CRE, it’s very common for lender timelines to outlast contingency deadlines.

An inspection contingency, meanwhile, protects you if the property’s physical condition turns out to be a deal-breaker. You will almost certainly need to formally terminate in writing before the deadline if things go wrong, or getting earnest money back will be complicated. You not only have to discover the problem, but also act on it correctly before time’s up.

If the property doesn't appraise at the sale price, then an appraisal contingency is your get-out. You’ll probably know that appraisals are slower and more complex in CRE, so this clause is particularly important during negotiations.

Finally, the due diligence contingency is probably the broadest protection in commercial deals because it covers various areas, including zoning, title, and rent rolls. Its importance means it usually has a hard end date, so once it closes, that’s it: you’re committed.

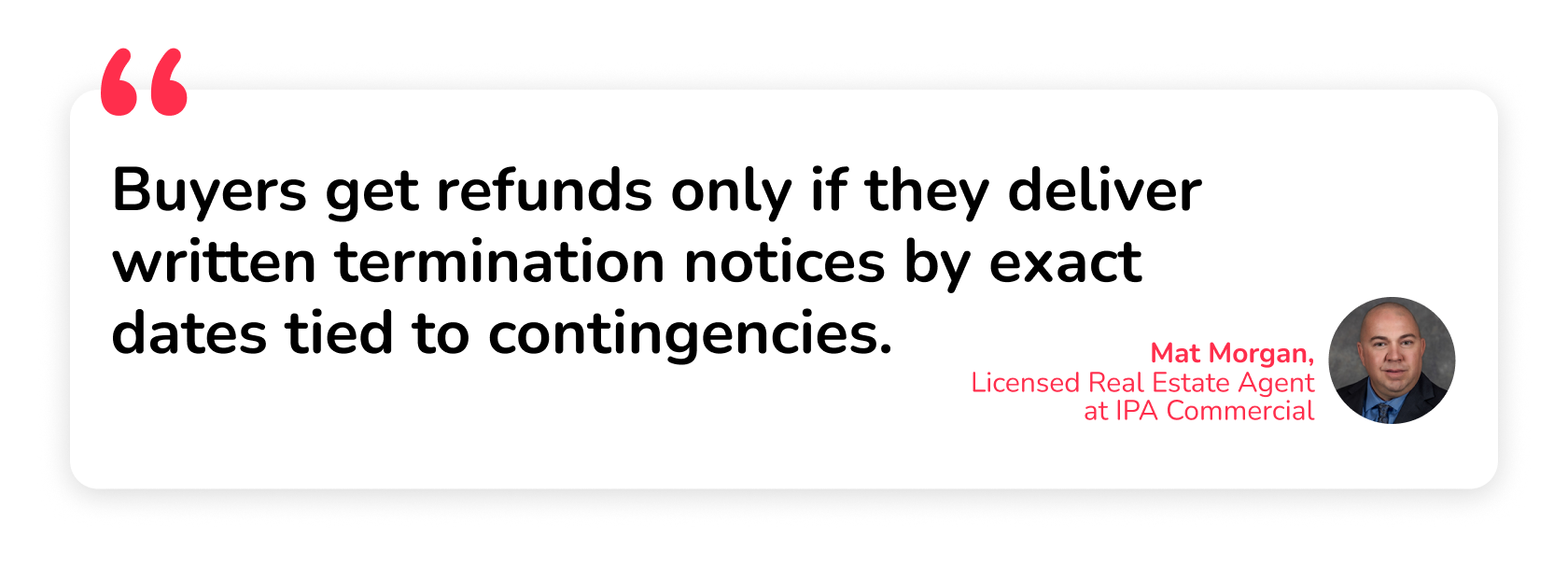

2. Timeframes

CRE deals are complicated, so earnest money deposits don’t go hard straight away. Instead, they’re structured so that they harden once the deal goes past certain contingency windows.

These windows are set according to timelines. Miss one of them and the chances of getting your EMD back decrease, so you must make sure they’re realistic, instead of optimistic. You’ll also need to have these termination notices in print.

“Earnest money refundability pivots on timeframes,” says Mat Morgan, a licensed real estate agent at IPA Commercial. “Buyers get refunds only if they deliver written termination notices by exact dates tied to contingencies.”

These notices will help you remember when the contingencies expire. After all, it’s a case of miss the window, miss the refund.

3. Default clauses

Contingencies and timelines tell you when you can exit; default clauses are the other side of the coin – they tell you what it costs when you can’t.

If you back out without a valid contractual reason — or simply miss a deadline — the default clause is what hands the seller your deposit. There's no negotiation at that point because the contract has already been decided.

It’s worth looking out for one trap in particular. Many investors simply assume that any title defect (an ownership or legal issue discovered during the title search) gives them a clean exit. This often isn’t the case: PSAs tend to only allow objections to “material defects”, which is a big grey area. Courts and arbitrators tend to favor commercial sellers in this scenario, so it’s best not to rely on it as an exit route.

Do you lose earnest money if you back out? ( 4 common real-world scenarios)

The simple answer here is: you might, but it depends on what’s in your contract.

Here are four real-world scenarios that you might come across in a CRE deal, and who would be entitled to the EMD in each case.

Scenario 1: Your financing falls through

One question that might rush through your head as you place your EMD is, “Can I get my earnest money back if my loan is denied?”

This comes down to whether you have an active financing contingency and if you act within its window.

It’s much easier to break this deadline in CRE thanks to longer lender timelines. If this happens after the contingency’s expiry, then the seller has a legal right to your deposit. The contingency protects you, but only for so long.

This is where understanding your commercial property loan deposit obligations before you sign can save you from a costly surprise later.

Scenario 2: You discover major issues during an inspection

Do you get earnest money back if an inspection fails? The simple answer is “yes, you should, but it’s not automatic.”

In this case, you’ll need to formally terminate in writing before the inspection contingency deadline. Miss this window by even a few hours,s and your refund disappears, no matter what you’ve discovered at the property.

Scenario 3: You simply change your mind

If you simply decide that you don’t want to proceed for a reason that isn’t in the contract, then you’ll almost certainly lose your deposit.

Putting down earnest money is to show that you have serious intent to buy the property, so walking away without a valid reason is exactly what it's designed to prevent.e.

Scenario 4: The deal drags past its deadlines

CRE deals need time. Lenders tend to run slow, reports are more complicated, and title issues often appear late.

Yet, the contract's contingency deadlines don't move unless both parties agree in writing to extend them. If your financing contingency expires while your lender is still underwriting, your deposit goes hard. Always build buffer time into your deadlines, and get any extensions formalized before the closing date.

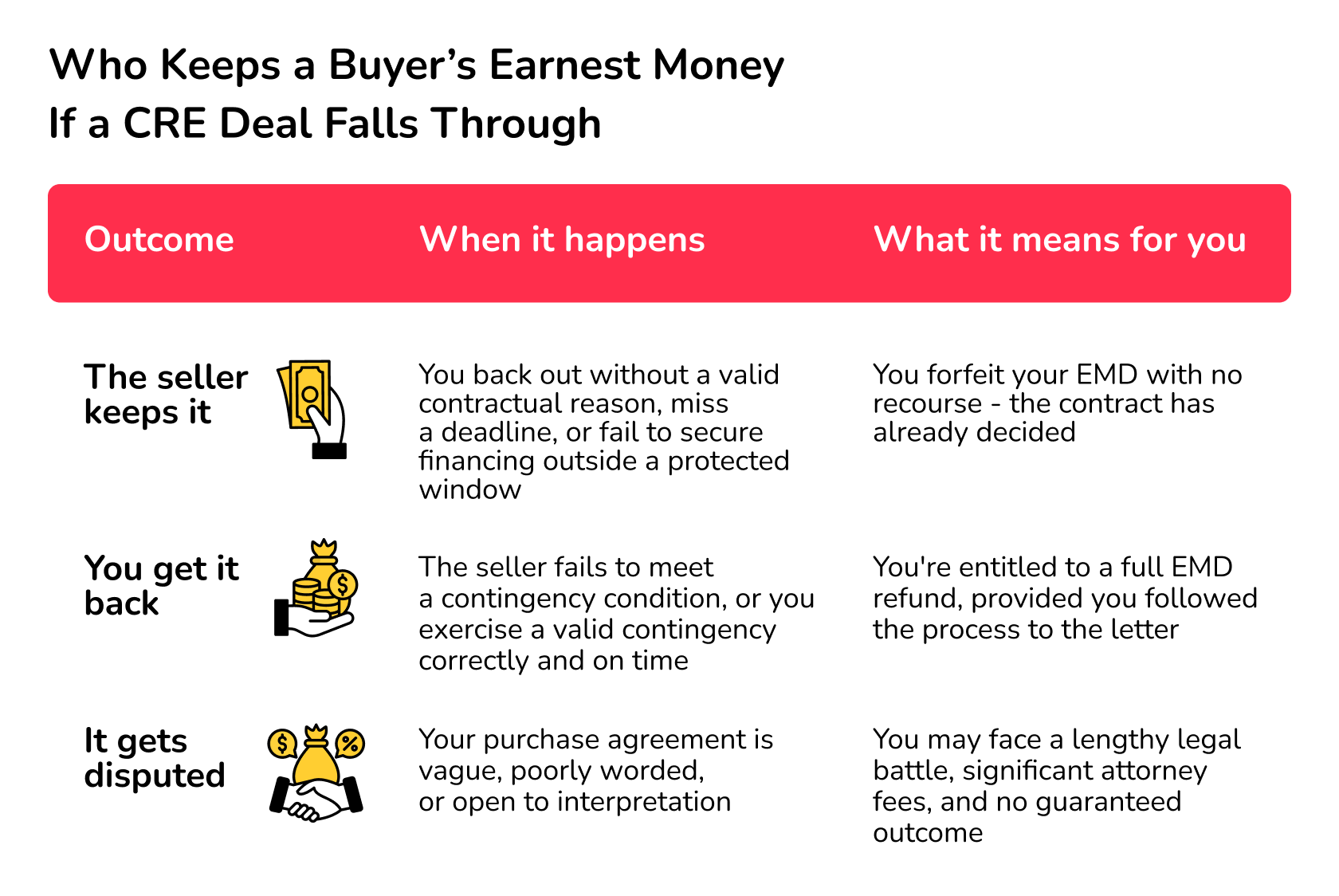

Who keeps earnest money if a deal falls through?

As mentioned, the contract decides who gets the earnest money amount should things go wrong, and we can summarize it as follows.

When can a seller keep earnest money?

If you back out without a valid reason that’s stated in the contract, you miss a deadline, or fail to secure financing within a certain amount of time, you lose your EMD rights.

When can you get it back?

If the seller fails to meet a condition that’s listed within a contingency within the stated timeframe, or if you exercise a valid contingency correctly and on time, then you have the right to an EMD refund.

When does it get disputed?

If your purchase agreement is vague or poorly worded, then you may face a lengthy legal battle to get your earnest money back. In commercial real estate, this can mean months of waiting and a ton of legal fees with no guaranteed outcome.

This is exactly why your real estate attorney should review the PSA before you sign anything.

There’s also the option to simply not risk your own capital for EMD and source it from elsewhere. The best EMD providers in the USA can fund your deposit quickly and cleanly, so your own liquidity stays intact regardless of how the deal plays out.

How to protect your earnest money in CRE deals

The best way to protect your earnest money is to take all precautions before you sign the contract, not after something goes wrong – yet, in CRE, this looks very difficult in the homebuying process you might be familiar with.

In a standard home purchase, common contingencies like the home inspection contingency and appraisal contingency are fairly clear and straightforward. These same protections exist in CRE, but the stakes are far higher, you have less time, and the wording of your real estate contract carries much more weight.

The best place to start is to argue for a longer due diligence period. Regular real estate windows are just too tight for commercial deals, and this extra time is golden.

You should also make sure your EMD hardens incrementally, with exit points built in for you as the deal progresses. Make sure your lender gets the time they need too with a more flexible financing contingency,

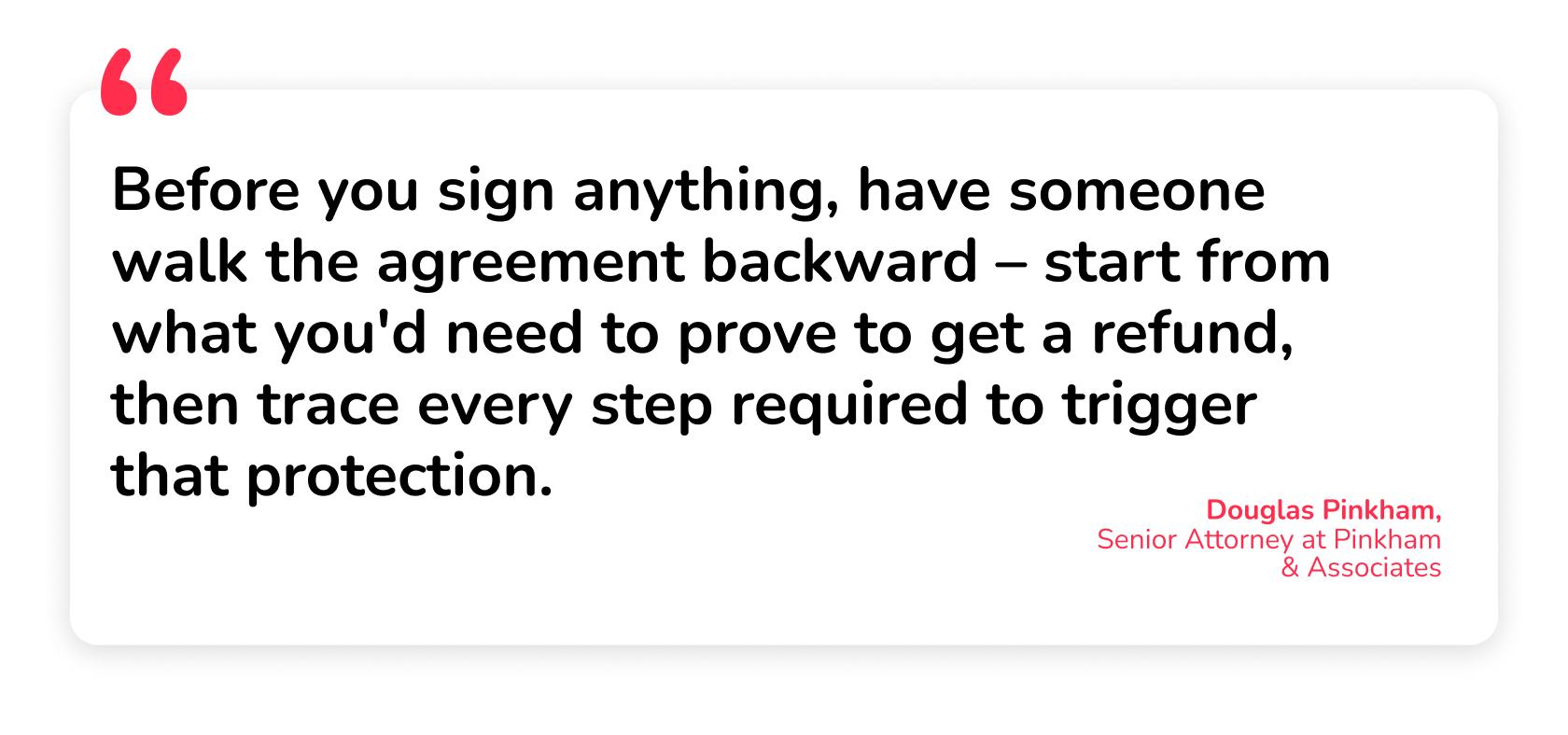

You’ll also need a reliable real estate attorney or realtor to review every clause, every deadline, and every default provision before you sign. They will help you make sure that you use clear and precise language, particularly around anything to do with inspections and title search results.

“Before you sign anything, have someone walk the agreement backward – start from what you'd need to prove to get a refund, then trace every step required to trigger that protection," says Douglas Pinkham, Senior Attorney at Pinkham & Associates, an Orange County law firm.

The clearer you are about your rights and timelines, the more likely you are to get your good faith deposit back should the deal hit a brick wall.

How Duckfund helps you secure your CRE deal without risking your own capital

Even if you manage every contingency perfectly, there's one problem no PSA can solve: you’ll still have a huge chunk of your own capital sitting in escrow for weeks waiting for a deal to close.

This is exactly the problem that Duckfund was built to solve. Apply in under five minutes, get approved within 24 hours, and have your EMD funding within 48 hours, with no collateral required.

And if the deal falls through? “Just let Duckfund know two days before the close of due diligence, and you’re free to leave without any additional action or fees,” says Anna Kogan, Duckfund’s CEO.

No obligations, no drama. Better still, with your capital free and Duckfund handling the EMD, nothing is stopping you from running multiple deals simultaneously — the way serious CRE investors actually scale.

Because in commercial real estate, the investors who win aren't always the ones with the most capital. They're the ones who know how to use it wisely.

Ready to stop putting your own capital at risk for earnest money? Sign up for Duckfund and find out how we can fund your next deal with no collateral, no delays, and no strings attached.

FAQs

Is earnest money refundable?

Yes, but only under specific conditions outlined in your purchase agreement. If you exercise a valid contingency correctly and on time, your good faith deposit is refundable. Miss a deadline or back out without a contractual reason, and the seller is generally entitled to keep it.

How does CRE earnest money differ from residential real estate?

In a standard home purchase, the homebuying process offers more predictable protections and modest deposit amounts. In CRE, deposits routinely reach six figures, due diligence timelines are longer, and the real estate contract carries far more weight. State law offers buyers significantly less protection in commercial real estate transactions.

Can you get earnest money back after inspection?

Yes, but the inspection report alone won't save you. You need to formally terminate in writing before the inspection contingency deadline. Think of it this way: discovering the problem is only half the job. Acting on it correctly and on time is the other half. Miss the window, and the report becomes very expensive kindling.

Can a buyer back out of a contract before closing?

Yes, but the consequences depend entirely on your real estate contract. Back out within a valid contingency window, and your deposit is protected. Back out without contractual grounds — even the day before the closing date — and you'll almost certainly forfeit your earnest money deposit.

Is earnest money refundable in Texas?

Texas follows the same fundamental principle as every other state: the purchase agreement, not state law, is the final word on refundability. Texan real estate professionals must follow established contract standards, so your earnest money refund ultimately comes down to your contingencies, your deadlines, and how closely you follow them.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence