What Happens If You Don't Deposit Earnest Money (And How to Make Sure It Never Gets to That Point)

It is no longer news that earnest money deposits (also known as good faith deposits) have become an important part of the real estate buying process.

One way to view this importance is that sellers are requesting it in all types of real estate transactions (residential and commercial), and buyers are competing on who can offer the highest EMD in competitive markets.

However, there is an alternative way to consider this importance: what happens if a buyer does not deposit earnest money?

Understanding the consequences of non-payment or delayed payment is a good way to appreciate the significance of earnest money deposits and be better prepared to handle them.

In this article, we will consider these consequences and help you identify how to avoid them by gaining consistent access to earnest money financing. We’ll cover:

- The growing importance of earnest money deposits

- How does an earnest money deposit work?

- What happens if you don’t pay earnest money? Consequences of non-payment

- What happens if you don’t pay earnest money on time? Consequences of delayed payment

- The major causes of non-payment and delayed payment

- Mastering earnest money: How to avoid non-payment and delayed payment

Do you want to learn more about how Duckfund can solve your EMD challenges? Contact us to learn more about how our EMD financing product can help you build a profitable CRE portfolio.

1. The growing importance of earnest money deposits

Earnest money deposits became normative in the real estate market as a way to protect sellers from unserious buyers.

Instead of wasting their time arranging an inspection or negotiating other finer details with everyone who inquires about the property, sellers can focus their energy on those serious enough to pay earnest money.

In other words, earnest money has come to serve as a signal of financial readiness and commitment. Sellers believe that buyers who can make this upfront payment are likely to be more committed to closing the contract.

On the other hand, as sellers have embraced it as a sign of financial readiness and commitment, buyers have adopted it as a negotiation tool. If other buyers are offering 5% of the purchase price, why not offer 10% to show greater financial readiness and commitment?

But the competition is not only on price. When sellers want to move fast, the buyer who can pay 5% earnest money within 24 hours may be more valuable than the one who can pay 10% in a week.

In other words, buyers have embraced earnest money as a way to compete on both amount and speed. Those who can offer higher amounts promptly can lead the pack and gain a competitive advantage in fast-moving markets.

2. How does an earnest money deposit work?

Let’s start by highlighting how earnest money deposits work in both commercial and residential real estate before focusing on the differences between the two markets.

How earnest money deposits work in CRE and RRE

The earnest money deposit is usually a percentage of the purchase price.

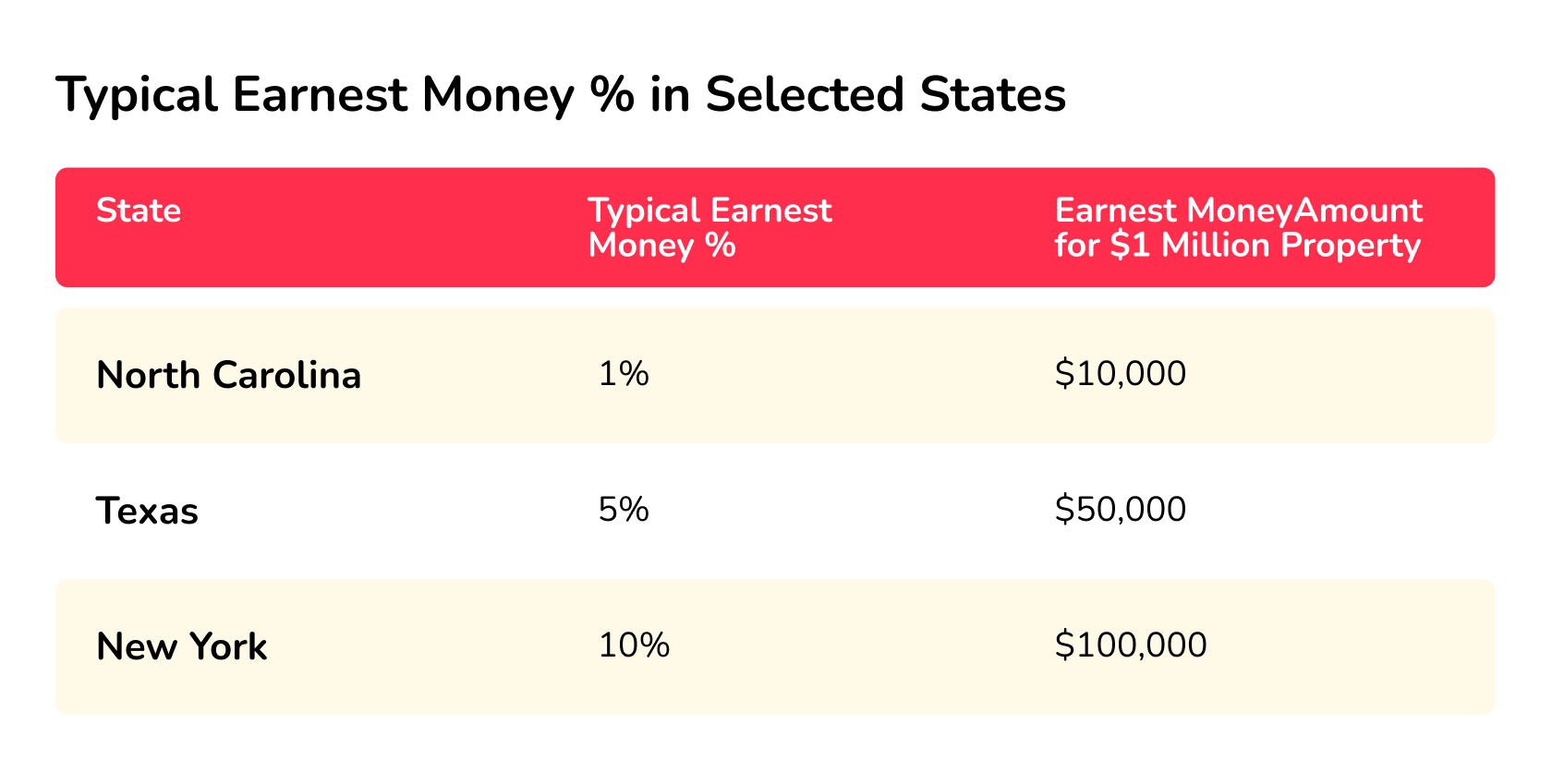

Since there is no legal requirement defining the earnest money amount, what you can expect to pay depends on the state where you operate. It can be as low as 1% in a state like North Carolina, as high as 10% in a state like New York, and it can be a medium rate like 5%, as it is in Texas.

Earnest money deposits are usually paid to an escrow agent (a title company, a real estate agent, a real estate brokerage, or a real estate attorney) that holds the money in safety on behalf of sellers and buyers.

All the important details regarding the earnest money are included in the Purchase and Sale Agreement (PSA), also known as the Purchase Agreement. These details include the amount to be paid, when it is expected to be paid, how the escrow agent is to handle the money, and the conditions for refundability.

Once a buyer pays the earnest money, the seller takes the property off the market and the due diligence period (the length of which is usually specified in the PSA) kicks off. During this period, the buyer can inspect and investigate the property to ensure everything is okay legally and physically.

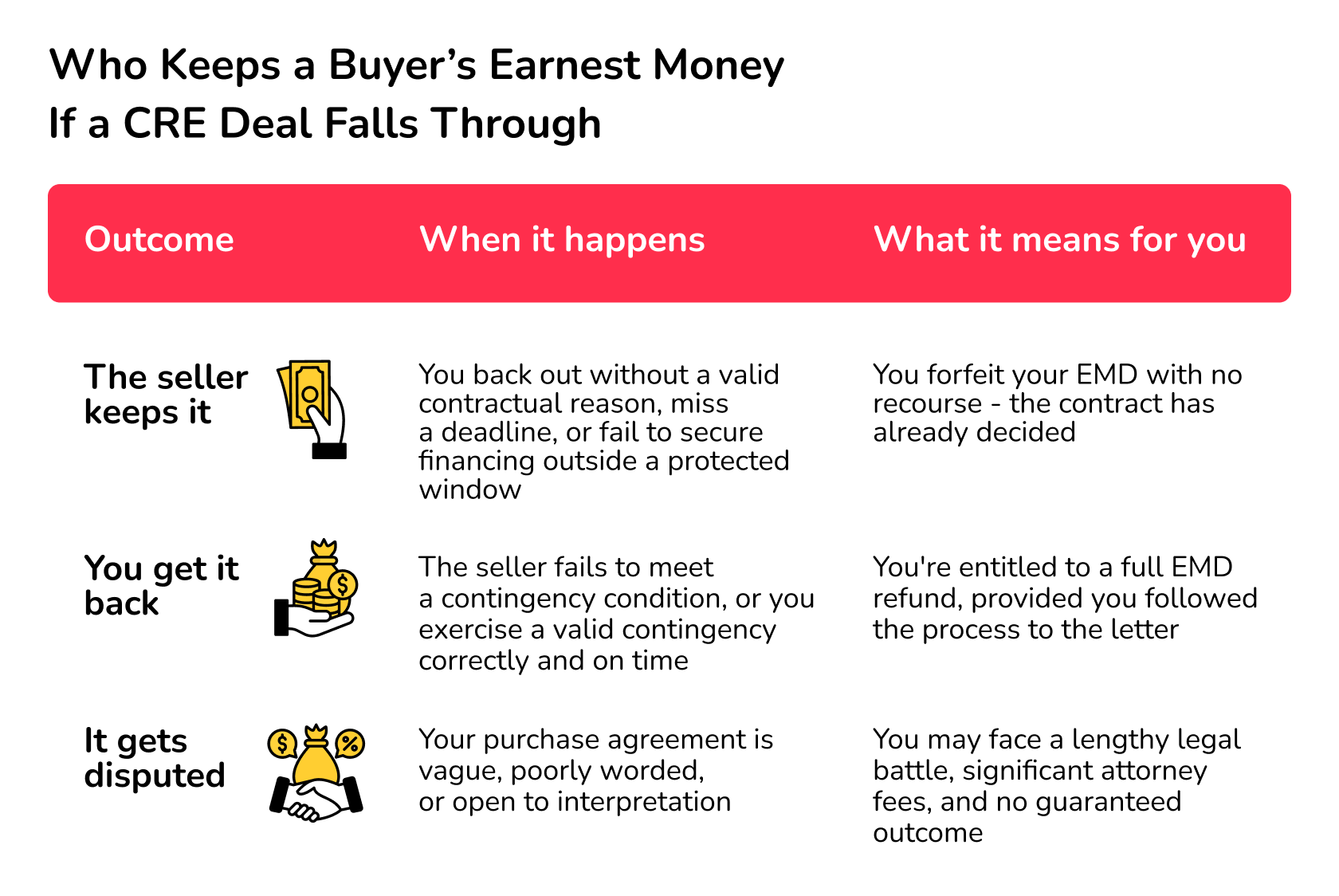

But is earnest money refundable?

This is one of the most common questions real estate buyers ask. As noted above, the refundability conditions are included in the PSA.

Usually, the PSA contains a list of contingencies (inspection contingency, financing contingency, title contingency, appraisal contingency, home sale contingency, and home inspection contingency, etc.) that give the buyer the right to pull out of the deal. If the buyer pulls out for any of these reasons, they can get the earnest money back.

Also, earnest money is refundable if the seller is the one pulling out of the deal. However, earnest money disputes often arise if the buyer backs out of the deal for reasons outside of the contingencies.

In this case, the earnest money is typically non-refundable. However, some such cases do end up in arbitration or litigation. To avoid such legal cases, it is better for the buyer and the buyer’s agent to carefully review the terms of the contract and ensure that all relevant contingencies are included (especially for residential properties).

Below is a summary of what happens with the earnest money:

But what do escrows end up doing with the earnest money if the deal succeeds? It depends on what the purchase contract (or sales contract) says. However, there are two major options: use it to cover the closing costs of the deal or the down payment of the mortgage financing.

How does earnest money differ between CRE and RRE?

Below are some important differences to note:

- Typical amount: Earnest money for commercial property in the US ranges between 5-10%, while it is between 1-3% of the purchase price in RRE.

- Refundability: RRE often has multiple well-defined contingencies that offer much protection to buyers. In CRE, the focus is on a longer due diligence period, within which buyers must raise any relevant issues.

“Commercial deposits are much larger and often move in steps,” according to Matt Vukovich, founder of Matt Buys Indiana Houses, a real estate investment company. “Investors face more risk because this money can become non-refundable once the inspection time ends. This means you must finish your property checks very quickly to protect your cash.”

- Buyer protections: Government agencies always ensure there are enough standardised rules to protect home buyers. For example, there are state-approved forms and escrow neutrality rules.

In CRE, buyers often have to protect themselves by ensuring they hire real estate attorneys who can structure the terms of the contract in their best interest.

- Negotiations: EMD terms tend to be more standardised in RRE, while they depend on extensive negotiations in CRE.

Now that we know how the earnest money deposit works, let’s consider what happens if the buyer does not deposit earnest money.

3. What happens if you don’t pay earnest money? Consequences of non-payment

As said above, the PSA will include information about the amount of earnest money to be paid, when that payment is to be expected, and how the escrow agent should handle the money deposited.

What happens if earnest money is not paid in accordance with the PSA?

Breach of contract

If the buyer misses the deadline stated in the PSA, then a breach of contract can be considered to have occurred, according to real estate law. Consequently, the buyer loses real estate purchase rights.

For this automatic breach to have occurred, the PSA must have specified that the earnest money is a requirement and that it must be paid within a stated period, according to William B. Serangeli, a retired attorney at Dickson and Bradshaw, a law firm.

Below is an example of a PSA wording where nonpayment of the earnest money can automatically result in a breach of contract:

“..the earnest money must be paid within 3 days of the acceptance of this offer. The failure to pay the earnest money within this 3-day time period shall make the Sellers’ acceptance null and void without any further action of the Sellers or notice to the Buyers.”

In a market like Indiana, there is a strict focus on this legal framing as it gives sellers the right to quickly cancel and relist (see below), according to Vukovich.

“In the Indiana market, the legal language regarding time is very strict,” he said. “Sellers often want to see funds within two or three days. If you miss that window, a seller might take a backup offer from a bigger firm. In this state, a solid deposit is what keeps your spot at the closing table secured.”

However, if the PSA does not contain an automatic-void clause like the one above, then the contract cannot be considered to be automatically cancelled even if the buyer did not deposit earnest money. That is, a legally binding contract still exists, and both parties still have obligations.

In this case, the contract must be formally terminated by both seller and buyer before they can be free from its stated obligations. Only after this can the seller or the seller’s agent accept a new offer.

We can consider how this works in specific markets by exploring what happens if the buyer does not deposit earnest money in Florida.

“Unless it’s stipulated in the contract that the money should be paid within a specific timeframe, you won’t suffer any legal consequences, at least not at the beginning of the transaction,” according to Key Title and Escrow, a title and escrow company in Florida. “It all depends on how far you go into the process without meeting the terms of the agreement.”

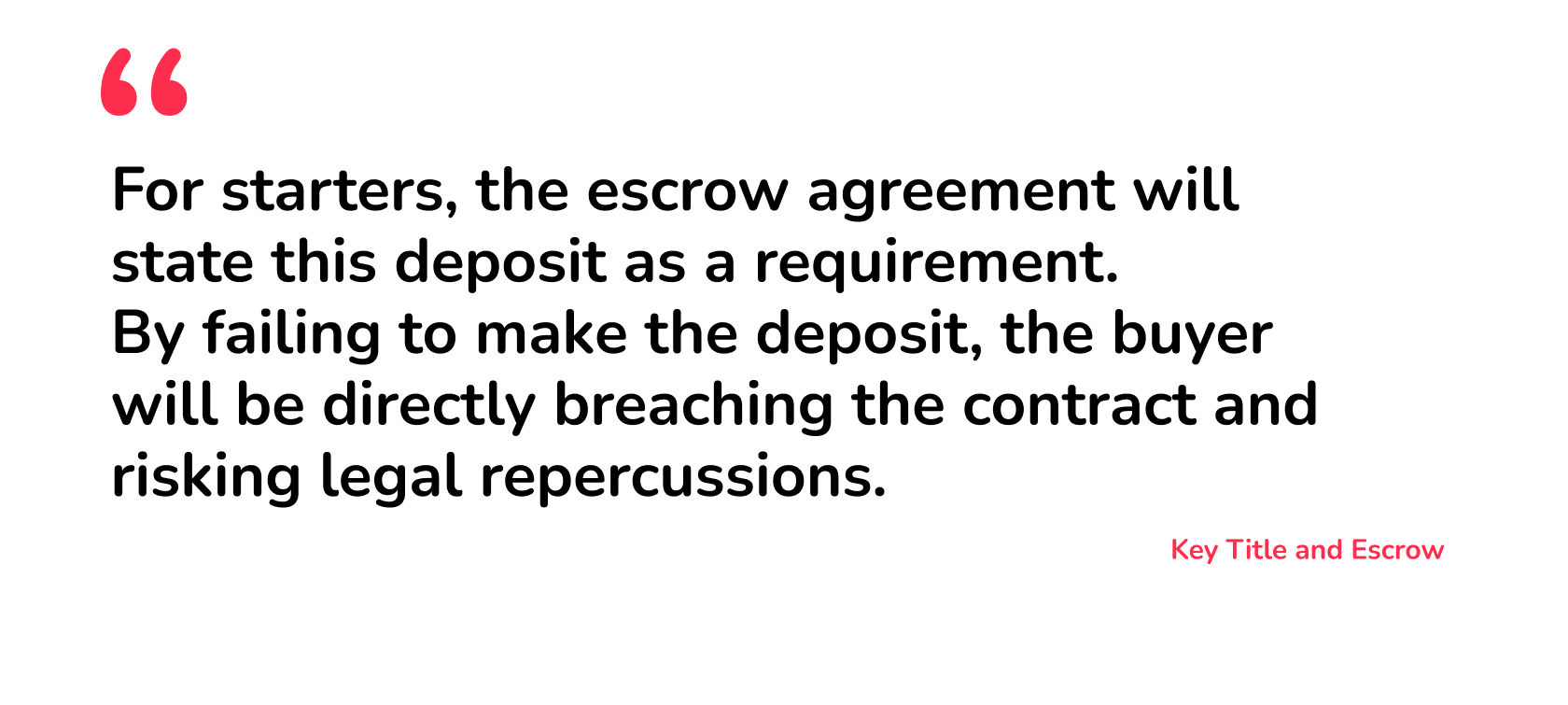

Also, a breach of contract only occurs if the purchase contract states that the deposit is a requirement.

“For starters, the escrow agreement will state this deposit as a requirement,” they noted. “By failing to make the deposit, the buyer will be directly breaching the contract and risking legal repercussions. This would also grant the seller the right to demand compensation, unless they agree to let the buyer pay the earnest money at a later date.”

In other words, an automatic breach occurs only when earnest money is listed as a requirement and there is a specific deadline for its payment.

Legal actions

If a breach of contract has been established to have occurred (there is an automatic-void clause), the seller can pursue legal actions, depending on the legal advice they receive.

For example, they might claim damages for missing out on other (stronger) offers.

However, this does not usually happen in practice. Sellers should seek legal counsel before embarking on such a quest.

Cancel and relist

In the event of a breach, it is more common in practice for sellers to cancel the deal and relist the property. This is also the usual consequence when both parties agree to cancel the contract.

“In the competitive Inland Empire market, a late deposit is often treated as a breach, allowing sellers to swiftly move to backup offers,” according to Matt Morgan, the founder of Inland Pacific Advisors, a CRE brokerage and consulting firm.

Reputation damage

In a competitive CRE industry, reputation matters. Sellers, and lenders for that matter, often agree to do business with investors if they have a history of honoring commitments.

Should you not pay earnest money following the signing of a real estate contract, then be prepared for the blow to your reputation that comes with it.

Word spreads quickly in the marketplace, and future sellers and real estate professionals (especially realtors) may hesitate to do business with you.

In fact, losing the trust of local real estate brokers is the most enduring consequence of nonpayment of EMD, according to Vukovich.

Issuance of a notice to perform

When a breach occurs, some buyers may decide to issue a notice to perform instead of immediately cancelling the deal. This notice to perform is usually a short window within which the buyer can pay the earnest money and get the deal back on track.

However, this is more likely to happen with a residential rather than a commercial property.

“In commercial real estate, if you don’t deposit your earnest money on time, it’s usually a deal-breaker,” according to Martin Boonzaayer, CEO of The Trusted Home Buyer, a real estate investment company. “Sellers can walk away immediately and move on to another buyer. In residential deals, there’s sometimes a bit more flexibility - agents might give you a reminder or short extension - but it can still void the contract. CRE is stricter and less forgiving overall.

4. What happens if you don’t pay earnest money on time? Consequences of delayed payment

We saw above that there are instances where the seller may issue a notice to perform instead of immediately cancelling the deal. This gives you a period of grace where you can still pay the earnest money and get the deal back on track.

However, the delay that has occurred here often has consequences:

Reputation damage

In competitive markets where timing is crucial, a buyer known for paying earnest money only after receiving a notice of payment will hardly get a look-in from sellers.

Shorter due diligence period

Even if the seller chooses to continue with the deal, the due diligence period cannot be renegotiated. This means you have to start the due diligence process later than usual.

Stricter terms

Delayed earnest money deposit payment may lead to stricter terms down the line, as the seller may be less inclined to trust you. This might mean refusing any extensions or concessions or doing so only for a fee.

5. The major causes of non-payment and delayed payment

Interestingly, non-payment and delayed payment of earnest money hardly result from a lack of interest in the property.

In fact, since the payment of earnest money is the beginning of the due dilligence period, it is almost impossible for issues with the property (which will be discovered in the due dilligence period) to be the reason for non-payment or delayed payment.

What then are the major reasons why buyers do not deposit earnest money?

Below are the most important ones:

- Liquidity issues: Real estate investors pursuing multiple deals may become cash-strapped, making it difficult to pay earnest money on a new property.

- Cash management concerns: In some cases, investors may have the cash but are unwilling to lock it up with an escrow. This might be because the cash is serving as an emergency fund for an ongoing project.

- Delay with financing sources: A real estate investor relying on a traditional bank loan may experience delays due to administrative issues.

Also, those who depend on private loans from other private investors or equity contributions from limited partners in a joint venture or syndication may experience delays when these sources experience sudden financing challenges.

These delays can be fatal, especially in fast-moving markets. “In fast-moving markets like New York City, Los Angeles, or Dallas, deadlines are taken very seriously,” according to Boonzaayer. “Even being a day late on your deposit can cost you the deal. In slower markets, you might get some leeway - but it’s never something you should count on.”

- Human error: In some cases, buyers may miss deadlines because they forgot or got the date muddled up.

- Technical errors: These can include wire transfer failures, incorrect routing numbers, or time-zone mismatches. Any of them can result in delayed transfers, which can have consequences, as we have seen above.

- Mastering earnest money: How to avoid non-payment and delayed payment

To avoid non-payment and delayed payment (and their consequences), you must find solutions to these five challenges that real estate buyers usually face.

The fourth problem – human error – is administrative, so the solution is operational. You should develop a system that ensures you don’t miss out on relevant deadlines. This can be something as simple as setting reminders before the payment deadline.

For the other challenges, the solution is simple: choose the right EMD financing solution and platform.

Choosing the right solution

When real estate investors have liquidity challenges or cash flow management concerns, they often resort to solutions like hard money loans, private money loans, partner funding, and a line of credit to fund earnest money.

However, there are challenges with these methods that can lead to non-payment and delayed payment.

- Hard money loans: Though they have a high approval rate and tend to release funds on time, they charge high interest rates and usually require collateral.

- Private money loans: Since these loans are based on personal relationships, they cannot be scaled for multiple deals. Also, private investors can run into troubles that make them unreliable.

- Partner funding: Since this is a form of equity financing, no repayment is needed. It is ideal for CRE projects that require large deposits. However, they dilute ownership and can take time to negotiate and structure.

- Line of credit: Since they are reusable, they can be scaled, and access to finance is quick. However, it requires a prior relationship with a financial institution and may include restrictions and covenants.

For these reasons, many investors, especially in the CRE market, are turning to specialized EMD financing providers. These are fintech platforms that are specially designed to finance EMDs across different CRE types.

Since they focus on EMDs, they can offer flexible deals that match the needs of investors. They also offer quick approvals, fast funding, streamlined processes, and high accessibility (no credit score or collateral required).

With such platforms, you can consistently access EMD financing when you are facing liquidity issues or cash flow management concerns. Even when you have the cash, you can use it for other purposes instead of tying it down in an escrow account.

“If you are cash-strapped, leverage specialized financing to keep your liquid capital available for the earnest money deposit,” advised Ryan Majewski, a managing partner at MLM Properties, a real estate investment company.

Choosing the right platform

Duckfund is a specialized EMD financing platform that supports CRE investors and developers in the US.

With them, you can complete an application in two minutes and get funds to an escrow within 48 hours. They have a streamlined process that minimizes the likelihood of technical errors, protecting you from the consequences of non-payment and delayed payment.

Furthermore, Duckfund helps you compete in competitive markets by allowing you to propose higher EMD amounts than competitors.

Also, with Duckfund, you can get EMDs for multiple simultaneous deals. This helps you build your CRE portfolio without worrying about liquidity.

What is more? You can access all of these without submitting a credit report. Duckfund uses a comprehensive system to analyze your business instead of obsessing over your credit score.

Do you want to avoid the consequences of non-payment and delayed payment of EMDs? Sign up now with Duckfund for a dedicated EMD financing partner committed to your investing success.

Takeaways

- Earnest money is a competitive tool, not just a formality. Buyers now compete on both deposit size and speed to win deals in hot markets.

- Missing an EMD deadline can trigger a breach of contract, allowing sellers to cancel and relist.

- Even if a deal survives, late payment can lead to stricter terms, shorter due diligence, and reputational damage.

- Most EMD failures stem from cash flow challenges, financing delays, or operational errors, not lack of intent. Selecting the right financing solution and platform is essential.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence