How to Secure a Commercial Property Equity Line of Credit in Today’s CRE Market

Chess players think three moves ahead. The most successful commercial real estate investors tend to think three funding steps ahead, which is exactly why the smartest ones keep a commercial property equity line of credit (CELOC) in their arsenal.

If you’ve invested in the CRE before, you may have come across common funding frustrations, including:

- Financing timelines that drag along and cost you deals

- Tough lending requirements that keep approval out of reach for too long

- Equity tied up in other purchases that you can’t make use of

Flexible and reusable, a CELOC can act as a kind of liquidity bridge that moves you past these hurdles, but you may not have used one before.

If so, this article walks you through how to apply and qualify for a CELOC, going into detail about what lenders look for, and how top-end investors use these credit lines to build smarter – without running out of capital.

Contents list:

- What is a commercial property equity line of credit?

- How does equity work in commercial real estate?

- How to get a commercial property equity line of credit

- Can you pull equity out of a commercial property?

- How to use a CELOC as an investment strategy

- Secure your next CRE deal without tapping existing equity

Want to unlock a stream of CRE funding? Contact Duckfund to discover how our flexible financing can secure your next deal in just 48 hours.

What is a commercial property equity line of credit?

A CELOC is a revolving credit line secured against the equity you've already built in a commercial property, which you can tap into whenever financing needs come along. These might be for renovation, or they might be for your next property deposit.

Unlike a commercial real estate equity loan, which hands you a lump sum upfront and starts charging interest immediately, a commercial equity line of credit lets you access funds as you need them, up to an agreed limit. You only pay interest on what you actually borrow.

You might have already heard of a home equity line of credit (HELOC). A commercial line works in a similar way, but is designed for commercial properties, including office buildings, retail spaces, multifamily units, and facilities in the industrial real estate market.

A CELOC is fast becoming one of the most useful mechanisms for investors who wish to pull off multiple deals at once because it’s fast, flexible, and uncomplicated. Those who can use it well may find they have a big competitive edge in a market that punishes those who hesitate.

How does equity work in commercial real estate?

As someone interested in real estate, you’ll already know how important equity is – and commercial property can help you build it quickly.

Let’s say you buy an office building for $2 million with a 60% LTV (loan-to-value) mortgage. You immediately contribute $800,000 equity upfront. As you reduce the loan amount and the property’s value rises, this equity starts to compound quietly in the background.

In a strong market, a well-chosen commercial property can increase in market value surprisingly quickly and become a powerful borrowing asset. However, that equity may grow at different speeds according to where the property sits in an unevenly distributed market.

Recent MSCI data from CRE shows how much this price performance can vary by sector, thus affecting how much usable equity you’re likely to see from your investment.

RCA Commercial Property Price Index (CPPI) by sector, 2001–2025

Source: MSCI

The chart tells a clear story: multifamily and industrial assets have held their value far better than CBD office properties, which have taken a notable hit in recent years. As it stands, you’re likely to get more CELOC borrowing capacity from the first two types thanks to this extra equity potential.

Yet, regardless of the asset type, most owners let this equity sit there idly when they could be using it as deployable capital to support further real estate investments. A CELOC is one of the most efficient ways to change that.

Does a commercial real estate loan build equity?

A common mistake that investors make is that a CRE loan builds equity by itself. This is not the case. A loan helps you purchase a property, but equity rises only come from your loan repayments and the property's rising value.

The equity is what you accumulate along the way, and eventually, what a CELOC lets you put back to work.

Can you pull equity out of a commercial property?

Bricks and mortar have a great capacity beyond just staying upright: they accumulate equity.

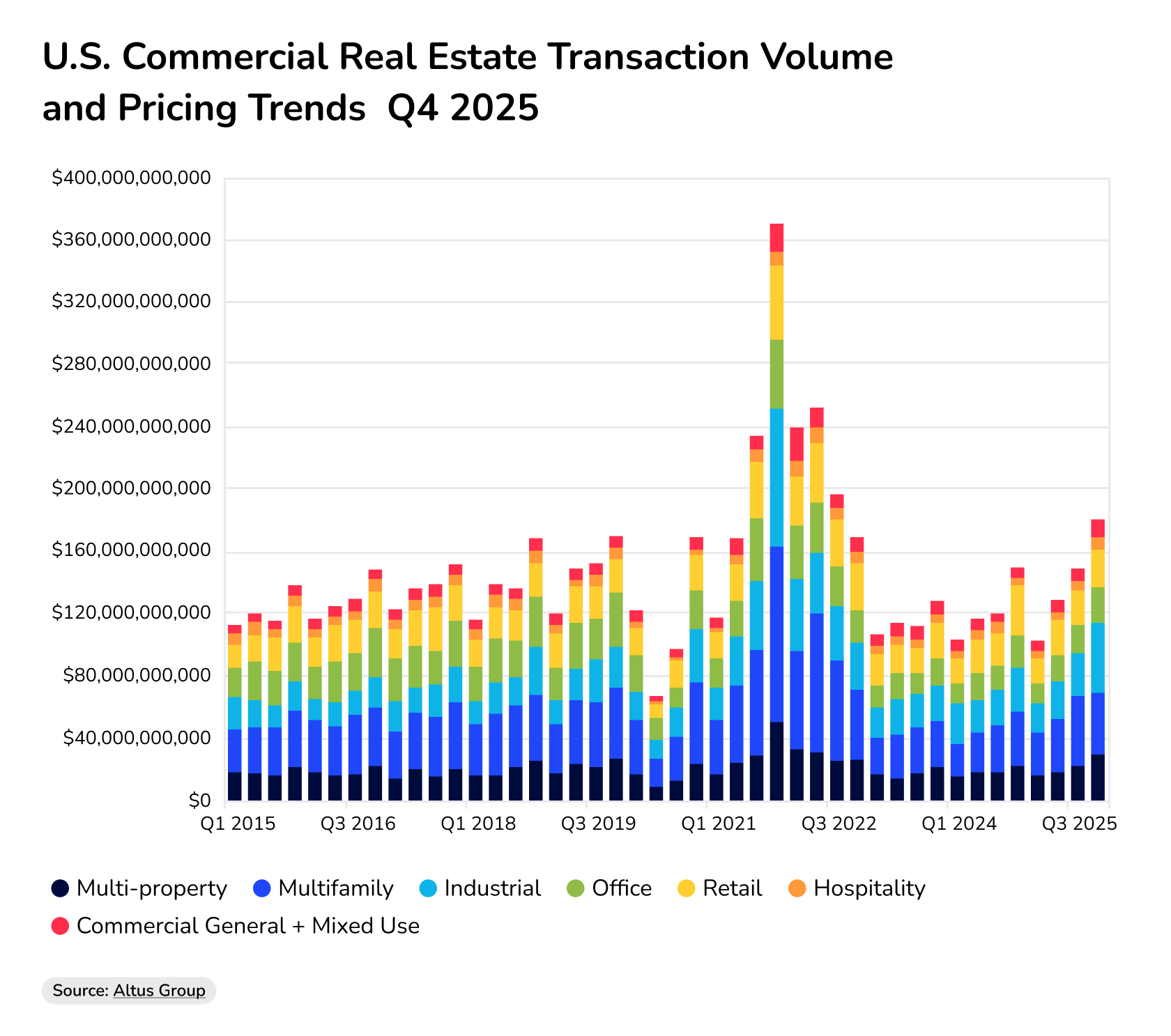

Even after a turbulent period since the pandemic, this has held. Late 2025 data from CRE experts Altus Group show stabilizing prices across the board, with a quiet but important recovery in the multifamily and industrial sectors.

Deal volume and median sale prices have firmed up, which usually means that appraised values follow in their footsteps. This is relevant for CELOC borrowers, as stronger valuations typically mean more accessible equity.

Source: Altus Group

Savvy investors know exactly how to put that to work, and there are several ways to do this. The most common traditional routes are refinancing your commercial mortgage or taking out a CRE property loan. Both of these will give you a fixed lump sum upfront, which makes them a good fit for a single, well-planned project where you know exactly what the costs will be. They tend to come with rigid loan terms, however, and higher monthly payments – not to mention the avalanche of paperwork.

A business line of credit is an option that offers revolving flexibility, but it's typically unsecured and better suited to covering operational costs or short-term small business expenses — not the large-scale commercial real estate equity financing we’re looking at here.

A CELOC tends to be more surgical. Lenders are more likely to approve a revolving line of credit that you can draw from, depending on your business needs, instead of a large lump sum. They typically come with interest-only periods, which keep early repayment costs lean, and you're not committed to a fixed-rate loan amount from day one.

You’ll still need a decent credit score (and manageable existing debt levels), but for borrowers with strong equity and clean financials, a commercial equity line of credit is one of the most capital-efficient loan options available.

How to get a commercial property equity line of credit

Knowing how to finance a commercial property purchase is one thing; having the right structure in place before you need it is another entirely.

Applying for a CELOC loan probably won’t test your patience as much as a traditional CRE loan, but it will test your financial housekeeping skills.

Here are the key steps you’ll need to follow:

- Get your house (or CRE property) in order

Commercial property equity line of credit lenders will take a magnifying glass to your property’s appraised value, its current LTV ratio, and the amount of equity you have tied up in it. Most of them want to see an LTV of 75% or lower, to use a general rule of thumb. The more equity present, the more likely you are to get reasonable terms and a higher credit limit.

- Back it up with solid paperwork

You’ll need to have your paperwork in order, too, including:

- Tax returns

- Financial statements

- Details of any existing liens or debt obligations

- Documents with security deposits and lease terms

- A reconciled rent roll

- Evidence of steady cash flow

- Your latest credit score

Preparation matters more than most investors expect. “The #1 investor mistake I see is walking in with a story instead of a clean package: messy rent roll, deposits not matching leases, trailing expenses not normalized, and no clear use-of-funds tied to value creation,” says Preston Guyton, founder of EZ Homesearch, a real estate search platform.

Lenders will want to see how the property will perform, depending on whether it’s a multifamily, owner-occupied, or pure investment property.

Their underwriting will revolve around one key question: Can this person reliably repay? They’ll want to see how a new revolving credit line fits into the bigger picture.

- Have a smart backup funding option

One last thing: approval can take a while as they take all of this into account. It’s a good idea to plan your liquidity well in advance, or keep faster-moving CRE financing options in your back pocket for when an important and urgent deal comes along.

What CELOC lenders are looking for in 2026

Lenders are applying sharper scrutiny across the board in 2026 as they go beyond LTVs and look at debt service coverage ratios (DSCR), tenant stability, and the predictability of your cash flow.

Looking at a multifamily development running at consistent occupancy? Good – this will fare much better than a property mid-reposition or facing lease rollover risk. Carrying multiple business loans? Not so good – you may find your credit limits trimmed as lenders take a wider view of total financial exposure.

“Right now, lenders are stress-testing cash flow scenarios that would have seemed paranoid 18 months ago, “says Arthur Putzel, managing partner for Trout Daniel & Associates, a full-service CRE firm. “When we worked through financing discussions on retail assets recently, lenders wanted to see not just current NOI but a demonstrated ‘what if’ scenario – what happens if your top tenant vacates?”

Underwriters are also increasingly sensitive to variable interest rates, so expect them to stress-test your cash flow against higher-rate scenarios before signing off.

Equity’s only the first step: you’ll likely need a stable income and clean financial management to get you the CELOC financing you’re looking for.

How to use a CELOC as an investment strategy

A commercial equity line can be two things. For cautious investors, it’s a useful financing tool; for confident investors, it can be a portfolio accelerator.

Here are the ways you can use it as part of a CRE investment strategy.

- Renovation projects

Renovation projects tend to need funds intermittently, which is perfect for a CELOC. Instead of taking out a lump-sum business loan and paying interest on capital just sitting around, you can draw out just what you need to cover the tasks at hand. This will help your property's value rise, your equity grow, and it means your CELOC effectively pays for itself over the course of the project.

- Fast-moving acquisitions

Commercial real estate equity loans and SBA product approvals tend to drag along, waiting for approval. A revolving line of credit lets you pounce on opportunities by providing a deposit amount of bridging funding gaps in less time than it takes for longer-term business financing to fall into place.

- Portfolio expansion

A commercial property line of credit lets you fund deposits across multiple properties simultaneously, which saves you from scrambling around for working capital or draining credit cards.

- Operational breathing room

Vacancy periods or lease-up phases can be costly, but a CELOC gives you variable interest rates and interest-only repayment periods to give you a flexible buffer – a much cheaper alternative to other financing options.

How to control risk when using a CELOC

A CELOC can help you grow your portfolio, but there’s a fine line between using it smartly and using it too eagerly.

Drawing out the full credit limit simply because it’s sitting there is a common mistake among investors. A CELOC is best used as a liquidity buffer for when vacancy periods and market wobbles come along unannounced.

It’s also a smart idea to keep a close eye on variable interest rates. A change may look manageable on paper, but it can quickly feel a lot different when it hits your cash flow.

Most importantly, make sure you map out each drawdown deliberately. Whether for a value-add renovation, acquisition deposits, or bridging structured financing, make sure you have a clear purpose.

A commercial property equity line of credit used with the intention strengthens your capital stack, but can become a problem if you use it carelessly.

When a CELOC isn't the right tool

For all its flexibility, business equity lines of credit like this do have a ceiling. Depending on your situation, you might hit it sooner than you'd like.

Here’s where it shows its limits.

- No existing property, no party

Most CELOC providers will want to see that you already have a profitable commercial property under your belt, which rules out new investors or those who haven’t managed to accumulate enough CRE equity.

- Timing risk

CELOCs may be quicker than most other financing methods, but they still need to go through lender appraisals and underwriting. This can be enough for a promising deal to disappear while your application is being processed.

- Unpredictable costs

There is a downside to variable interest rates – forecasting gets tricky. Unlike a flat-fee financing model, you might get a surprise or two if you don’t keep track, including high commercial real estate equity loan rates.

For investors who need to move fast, scale quickly, and keep costs predictable, these limitations matter, and they point toward a different kind of solution entirely.

Move faster than a CELOC: CRE financing for investors who can't afford to wait

A CELOC is one of the most powerful CRE funding mechanisms out there – a brilliant way to put your idle equity to work – but it can only move as fast as the underwriting and approval process allows.

In a market where the best deals close in days, this lag can be the difference between securing a property and watching someone else sign the contract.

Duckfund was built precisely for the moments a CELOC can't handle. With us, you can lock in your earnest money deposit within 48 hours without using your own capital.

No lengthy approval processes. No early repayment processes. No hidden fees. Just a transparent flat rate and unlimited reborrowing across as many properties as your strategy demands.

Ready to grow your CRE portfolio? Sign up for Duckfund and unlock fast, flexible EMD funding in minutes.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence